Week 193: On getting from here to there

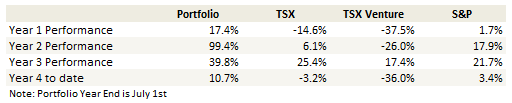

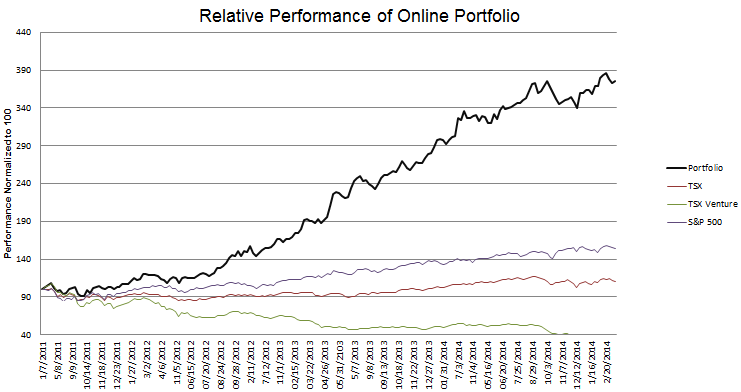

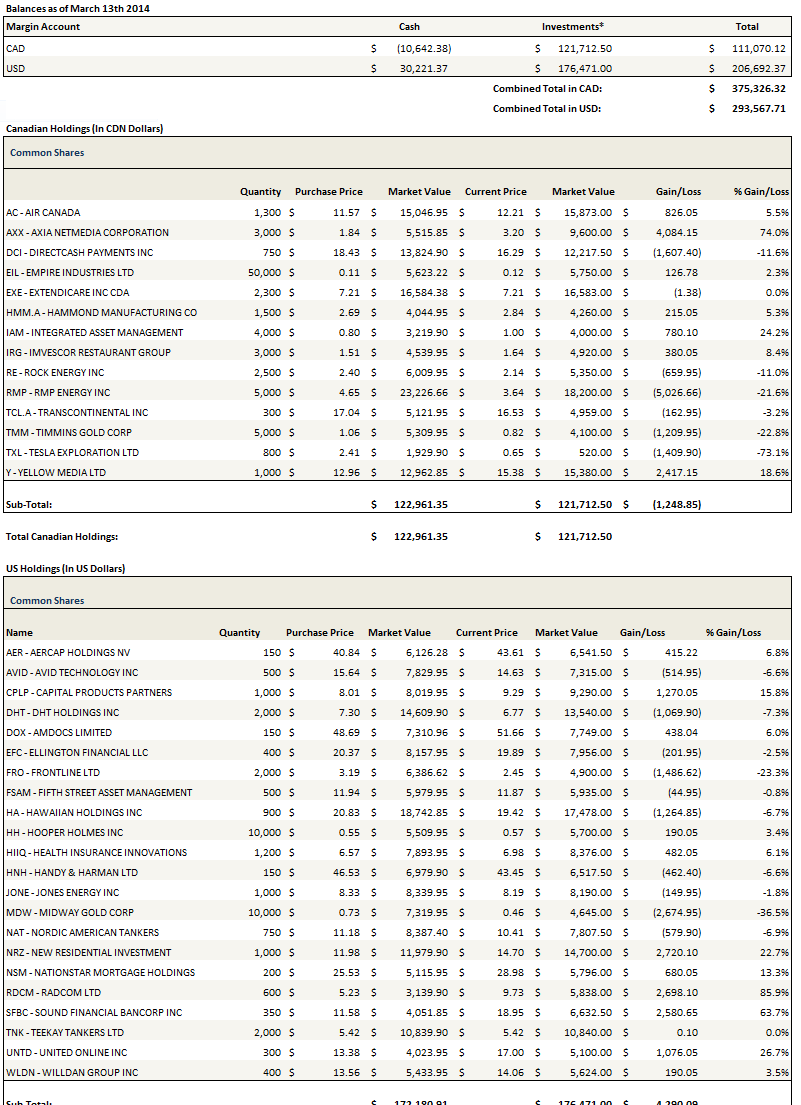

Portfolio Performance

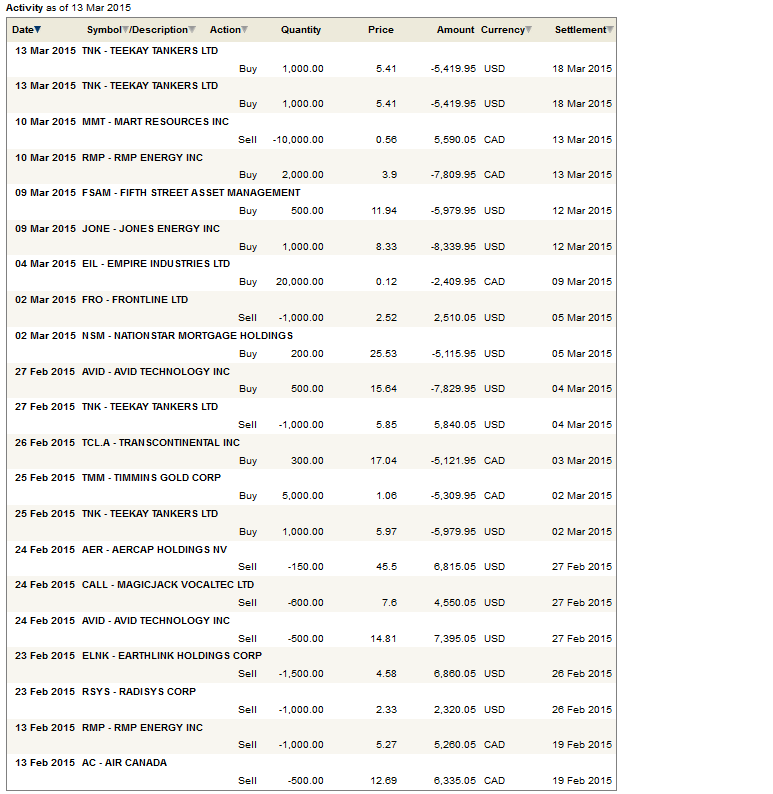

See the end of the post for the current make up of my portfolio and the last four weeks of trades

Updates

This is a difficult investing environment. Valuations are high and the market is choppy. Even as I do my best to limit my exposure to the gyrations by keeping 25% of my portfolio in cash, reducing the size of all but my favorite ideas, and parking cash in dividend paying investments, I still find my stomach churning on days like some of those this week, as I found myself down 2% after Tuesday’s close.

Many stocks that might appear attractive in their own right are difficult to own in this environment. It is a situation I find unpleasant. While I am still a relatively young man, in markets like these I find myself too old for this.

Like most Canadians I have two accounts. I have an investment account, and an RRSP account. Through most of the last 10 years, which constitutes the extent of my productive investing career, these accounts have seen similar allocations. What I did in my investment account, I did in my RRSP. However 4 months ago I changed this strategy. I cleaned my RRSP out of anything speculative, anything small cap, and what I own now are primarily dividend paying companies and REITs. And a lot of cash.

I just can’t justify the chase given the circumstance and intent of the account and where the market is right now.

In fact, I would expect that at some time in the next couple of years this blog is going to undergo a facelift. Its going to become the ‘how to make money on dividends and not lose your principle’ blog. That happens about 30% from now, so you can put a timeframe to that depending on the returns you think I can manage.

People write blogs like this for different reasons. Some are looking to make a name for themselves by finding the next big zero or riding a name on the discard heap to the sun. Others are hoping to parlay their knowledge into a career or at least a few mentions on network cable. I’m in this for two reason. First, I actually enjoy writing. Second, I want to get to my goal and be done with it, and writing this blog speeds up that process. How can I get from here to there in the shortest time possible? That is my trajectory. While the arrival time is getting close, I’m not quite there yet.

It is this purpose that allows me to exercise as little conviction to my ideas as I see fit. I’m not interested in appearing consistent. If an idea is not working I sell it. If I read or learn something that changes my mind, I change it. That may be even after I have said only a week before that I loved the idea like a son. I learned soon after starting this blog that I would have to decide whether I wanted to be right and look good or make money. If I chose the former then I would have to either A. be perfect, or B. show a herculean ability stand by my convictions in the face of adversity and a willingness to stick things out for the long haul through inevitably lags in performance. Well I’m certainly not A, and B is a little too risky given that A is not likely to be achieved.

Onto my chariots.

Oil Stocks

I took a position in Jones Energy, and I now have exposure to 3 North American E&Ps (with RMP Energy and Rock Energy being the other two). I am likely too early; WTI continues to fall and the storage builds continue to mount. But I have a good memory, and I know that trying to predict the stock price turn is not the same as predicting the turn in the underlying conditions. Remember that things were not necessarily all that rosy in April of 2009 when the stock market decided enough was enough. Besides, as I will point, this is only one side of a 3-way hedge.

Sometimes you have to lose a little money to make money, and that is the perspective I am taking with Jones Energy. I will talk more specifically about why I chose Jones below, and give a little update into some of the work I have seen on RMP Energy, a second position of mine. But first a little perspective on oil and how I think about my positions.

At worst what I have here is a hedged bet. I have my oil stocks one the one side and my airlines and tankers on the other. At some point, one, or maybe two of these guys is going to be a winner.

The best case outcome is that I have 3 winning bets with staggered payoffs. Here is how I think this plays out.

First, oil continues to be under pressure in the short-term. This is already happening. Storage continues to rise, production grows, albeit at a slower pace. The contango widens and once again the tanker stocks come into favor. I do not believe that the tanker story is merely a storage story but the market does, so a short term move in these stocks depends on some negative developments on the oil price side and a positive move in the contango. Tanker rates are already at elevated levels. If rates move up during what should be the weaker spring season there will undoubtedly be calls that after a 6 year hiatus, the tide has finally come back in for the tankers. As these stocks move back up, hopefully to their highs or beyond, winning bet #1 pays off.

Next, oil settles as it becomes clear that production has peaked and nobody is drilling any more. The current narrative of collapse and fear is replaced by a narrative of the “new normal”. The new normal narrative will be that low prices are here to stay. This is what is going to set off the airlines. They have been in a holding pattern since the beginning of the year, digesting some really large gains and wrestling with whether the boon in fuel costs is actually something that can be priced in for the long run. Once the market decides it can be, they move up another leg and I get winner #2.

Finally for the last winning bet; the E&Ps. Getting to here might be a shit-show or it might not. The market is already starting to show signs that it discerns the survivors from the wreckage. Of the three E&Ps I own, Rock Energy has no debt, RMP Energy has $115 million on a market capitalization of over $500 million (so very low debt), and Jones Energy, which does have a healthy amount of debt, has done such a good job hedging their production until the end of 2016 that by the time they realize spot prices most of their lessor hedged brethren will have already succumbed. Rock and Jones have done secondaries. These companies are in good shape.

I don’t think oil prices have to go back to $100 for stocks like these to rise. At some point a legitimate new normal will assert itself and prices will go back to a $65 or $70 level where supply and demand are balanced. Now I know there is a lot of talk that E&P’s are already pricing in $70 oil or $80 oil. While I think this argument is being reserved for the larger entities, the EOG’s of the world, and not these smaller players who have actually taken a very hard fall, I also think this argument is flawed. I simply ask you this: If some of these companies are pricing in $70 oil, are they also pricing in $70 oil service costs?

As I will explain below using Jones as the example, service costs are collapsing. And that means $70 oil is no longer actually $70 oil. $70 oil is maybe $85 oil when you look at in terms of margins, which is what matters. And not operating margins, not the somewhat irrelevant costs that are used to put together all the break-even forecasts you hear about. I’m talking about the half-cycle margins that include the primary cost associated with producing oil: drilling the well. Those costs are coming down big.

The beauty of it is that $70 oil is still going to be $70 oil for the debt laden and high operating cost producers and so the cash flows of many will continue to be constrained. But for the operators with the financial flexibility to drill and the land positions to achieve attractive returns, they will inherit this new earth. And that is when my third bet pays off.

Why Jones?

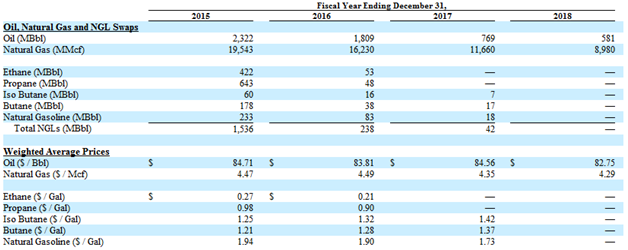

So I bought Jones and I think they have a very good chance to be a big winner when we eventually come through this morass. Reason #1 for my optimism is that Jones has a very good hedge book for 2015 and 2016:

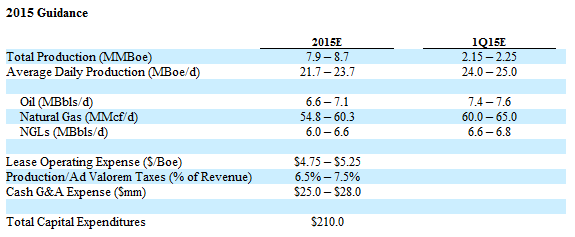

Compare the above hedge positions to the company guidance below:

So to put everything in like terms, guidance is suggesting oil production of about 2,518MMbbl, natural gas production of about 21,000MMscf and NGL production of about 2,300MMbbl. That means they have about 92% of oil production, 93% of natural gas production and 66% of NGL production hedged at decent prices for 2015. The volumes hedged for 2016 are not far off that.

On their fourth quarter conference call Jones said that their drilling and completion costs are coming down substantially. Wells that used to cost them $3.8mm are down to $2.9mm. They think that will come down to $2.6 million in short order. That is a huge change that has moved the profitability curve down substantially.

While all operators are seeing costs come down, Jones is in enviable position being the major operator in the area – I think they have more leverage over their suppliers than some.

Unlike my other two E&P picks, Jones has debt. They have also taken on more debt recently. At the beginning of February they sold $250mm of 9.5% senior unsecured notes due 2023 to the market.

Jones has also issued shares, but worth noting, the offerings were at substantially higher prices than what the stock is trading at today:

A. 4,761,905 shares at $10.50 to Magnetar Capital LLC and GSO Capital Partners LP

B. 7,500,000 shares at $10.25 via an underwriting with underwriter option for additional 1,125,000 shares

In total Jones has offered 13.4 million shares if underwriter option is exercised. It will raise a little over $130mm in proceeds from the offering.

As far as the operations go, things look solid. The company is going ahead with three drilling rigs all focused on the Cleveland. They’ve settled on a frac design and will be going back to an openhole completion with 33 stages. This is expected to give them the oil uplift that had been the intent of all the experimentation that they did in 2014, but without a lot of added cost. Production is going to fall as they cut back on drilling, but I think we are all past the point of worrying about what happens to production in the short term. They didn’t have a lot to say about their Tanaka wells on the last conference call, but given the opportunity for additional lands that is likely to open up in the Cleveland, I’m not sure if the viability of the Tanaka is relevant any more.

Basically, I think Jones will weather the storm here. They have ample liquidity to increase their position in the Anadarko basin with cheap assets. You can pick up the shares at a 20% discount to the underwriting less than a month ago. The near term commodity price risk is greatly mitigated given the hedge book. The move down to $8, which unlike many of their peers is a significant new low, seems to me to be unjustified given all of these factors.

Reviewing RMP Energy

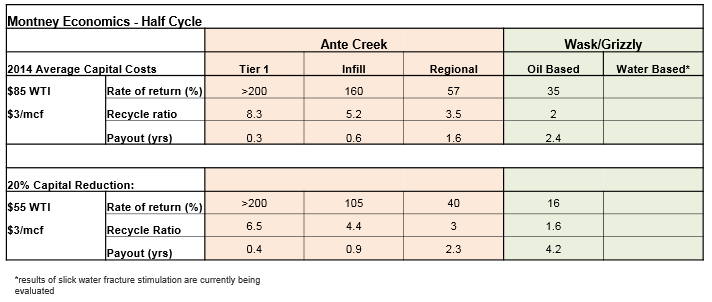

Since I the discussion revolves around E&P’s in this post, I wanted to give a few thoughts on RMP Energy. In the last couple of weeks I spent some time reading through and analyzing a recent report put out by Peters. In the report Peters raised some concerns about the extent of Ante Creek play and the recent decline in Ante Creek production. Production at Ante Creek is down to 8,300boe/d from around 10,200boe/d in the summer. Peters lowered their target price on the stock.

To some extent their concerns are valid. The Ante Creek wells drilled in the south aren’t as productive as those in the core 8 sections. In the recent March presentation the company the company said as much, delineating between the core, the infill of that core, and regional development.

With that said, I don’t know if I would worry too much about the production declines. I think that it has more to do with facility capacity constraints than anything else. The problem is that as the reservoir pressure declines the wells are producing a higher gas content. Pretty typical behavior.

If you look at the numbers, at 10,200boe/d the volumes were 63% liquids, so gas production was about 22.6MMscfd. At 8,300boe/d gas production is now up to 48%, or about 23.9MMscfd, so even as the overall production has declined, gas production has ticked higher. And its started to hit the ceiling. According to the March presentation the facilities at Ante Creek can only handle 24MMscfd at current gas plant capacity:

Fortunately more capacity should be online shortly, at which time we will see what production can really do.

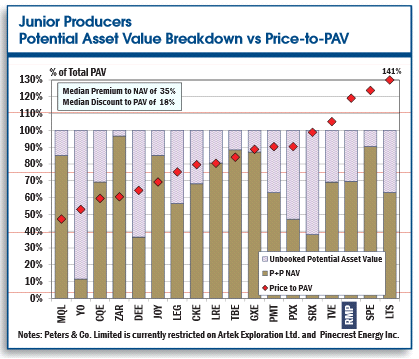

Peters NAV in the report was $4.25. Its pretty easy to come up with a higher NAV than that and in fact some of the other analysts do, but lets go with this number for sake of comparison. At the time of the report, at a $5 price, RMP was at a 20% premium to NAV. This was at the upper end of the peer comparison below:

At the current price, a little under $4, RMP trades at less than 90% of NAV which is pretty closely inline with their peers. But should RMP really trade at the same level as LEG or DEE? Probably not. So I think the stock has probably come down too far. I traded some RMP when it got into the $5’s, waited patiently for it to correct like this, and now I’ve jumped on it here sub-$4.

The other leg to the story is that RMP has had excellent initial results for the two Waskihagan wells drilled with their new slick water frac design. You’ll note in the table above that the Waskihagan wells don’t have a great return with the oil based fracs. RMP is testing out slick water based fracs and the first two have performed admirably so far. Another poster on InvestorVillage posted a list of the top performing wells in the WCSB in December-January and the two water based frac wells from RMP made the list.

Fifth Street Asset Management

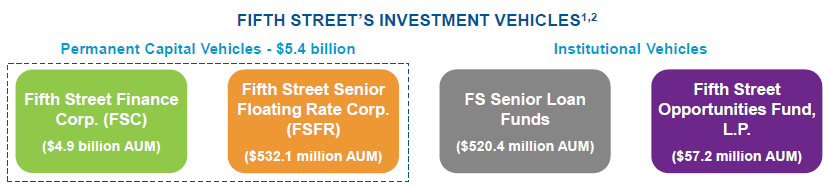

I tweeted this one out on Thursday. Fifth Street Asset Management is a fairly small, recently IPO’d asset management company. They manage a little over $6 billion in assets, with about 90% of those residing in two business development corporations (BDCs).

The stock did an IPO in November at $17 per share. Since that time it as sunk in price, for what I believe are two main reasons. First, both of their BDC vehicles trade below book value, and the company has come out and said that they will not raise capital at their BDC’s below book. This invites the assumption that growing assets under management (AUM) is off the table. Second, the larger of the two BDC’s, Fifth Street Finance, put out some fairly crummy results in February, including a reduction of the dividend and news that the existing CEO, Leonard Tannenbaum, would be resigning to focus on Fifth Street Asset Management and their new hedge fund.

The stock did an IPO in November at $17 per share. Since that time it as sunk in price, for what I believe are two main reasons. First, both of their BDC vehicles trade below book value, and the company has come out and said that they will not raise capital at their BDC’s below book. This invites the assumption that growing assets under management (AUM) is off the table. Second, the larger of the two BDC’s, Fifth Street Finance, put out some fairly crummy results in February, including a reduction of the dividend and news that the existing CEO, Leonard Tannenbaum, would be resigning to focus on Fifth Street Asset Management and their new hedge fund.

This feels to me like one of those stories where yeah, the news is bad, but chances are it is transitory and as it is digested and conditions improve the stock could quickly go from dog to darling. While they are unable to expand their AUM via the BDC’s Fifth Street does have other options for growth. The company recently closed on a $309 million CLO. They are starting a hedge fund (which as I mentioned will also be run by Tannenbaum), are expanding into aircraft leasing, and starting a Japan focused fund. So there are other ways to grow. And while the BDC’s are below book right now things change.

I think they can do $1+ earnings per share this year. The company distributed 30c quarterly dividend in January. On the conference call where they announced the dividend they warned that it would exceed 100% of income in the fourth quarter and possibly exceed 90% of net income for 2015. As was picked up on by one of the analysts on the call this implied managements expectations of earnings, that they think $1.20 per share is reachable.

I think there is a reasonable chance that the concerns about the FSC subside, the company shows further evidence that they can raise capital outside of the BDCs, and the market begins to focus on the growth potential rather than the lack thereof. And the stock comes back to its IPO price.

Patriot National

This is another recent IPO that I think has some upside if they can execute and the market gets comfortable with them. The IPO price was $14 and I have bought the stock at a significant discount to that in the low $11’s. The IPO prospectus can be viewed here.

Patriot handles the procurement and management (including claims management) of workers compensation insurance. They basically sign a contract with a client for a set book of workers compensation business, then procure that business through affiliated insurance agents and manage it. The contract will define the risk parameters, geography, premium size, etc that they want in their book. Patriot’s system distributes the data to its agents who then look for opportunities to sell into it. Patriot doesn’t take on any of the claims risk.

Patriot currently provides services to Guarantee Insurance, Zurich Insurance Group Ltd. and Scottsdale Insurance Company. Scottsdale is a relatively new relationship that should continue to add reference premium growth during 2015. They recently began a relationship with AIG, of who they will begin to provide services to in 2015 and expect to become one of their “primary insurance carrier clients over time”.

They are a small company compared to many of their peers. with 26.4 million shares outstanding, the market capitalization sits at $290 million. The company will likely do around $23-$25 million of EBITDA in 2014, which doesn’t make them seem particularly cheap. So the story here is growth and I think there is a good chance they can achieve that.

One of the interesting elements of the business model is that Patriot has quite good visibility into its future revenues, because the contracts are signed up front and then Patriot goes out and fills them. I managed to get a hold of the BMO report on Patriot. Being the underwriter of the IPO, presumably BMO has a close line with management. In the report, they expect reference premiums to grow from $375 million in 2014 to over $500 million in 2015 as the relationships with AIG and Scottsdale mature. That would be 30% growth.

In the company can put together that kind of growth the 14x EBITDA multiple would be justified. If you apply the multiple on the higher level of business, its easy to come up with a lot of upside from here. Also worth noting, this is a low cash use business. Maintenance capital is in the low single digits, and the company only has about $40 million of debt, so the vast majority of EBITDA falls down into free cash generation.

Anyways much like Fifth Street I think that Patriot is suffering from the post-IPO uncertainty. No financials, no track record, no conference call, and the only information it buried deep in a prospectus that most people don’t want to bother with. I think there is a decent chance they continue to execute on the business and grow reference premiums, and that the stock runs up into the high teens.

TC Transcontinental

TC Transcontinental is a pretty simple story. They are the largest printer in Canada. Their printing operation is diverse and includes flyers, packaging materials, newspapers, magazines and books. Of those lines of business, the main driver of revenue is from retail flyers for customers such as Superstore and Canadian Tire. Flyers and related services make up a little over 50% of their total revenue. In addition Transcontinental owns an array of local newspaper and magazine publications in Quebec. They recently expanded into flexible packaging with the purchase of Capri. The table below illustrates the primary customers in each of their segments.

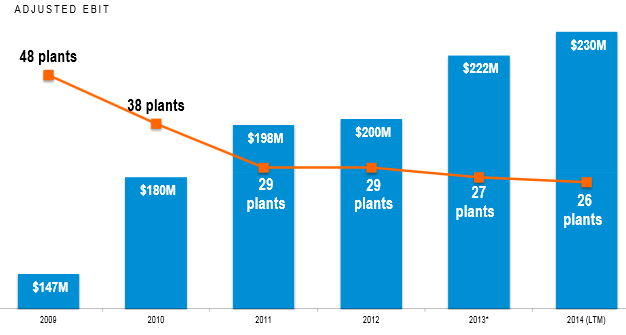

While the print operations are by no means a growth industry, the company has done well to stabilize revenues while improving EBIT from the business. EBIT has shown continuous improvement for the last 5 years.

Over the long-term, print remains a challenged business. Maybe flat to a down couple percent a year. Transcontinental is offsetting the declines by pushing growth from within their media segment (via a growing online presence) and through the expansion into flexible packaging.

Over the long-term, print remains a challenged business. Maybe flat to a down couple percent a year. Transcontinental is offsetting the declines by pushing growth from within their media segment (via a growing online presence) and through the expansion into flexible packaging.

The company has made a couple of acquisitions over the last year and a half to facilitate some growth. First, in December 2013 they bought a number of Quebec local newspaper and magazine assets of Sun Media. They paid $74 million for these assets, which generate annual EBITDA of about $20 million. In April they entered into flexible packaging with the purchase of Capri for $133 million. Capri generates EBITDA of about $17 million, and 75% of revenue comes from a 10 year contract with Schreiber Foods.

While neither of these acquisitions are revolutionary, I believe they are paying a reasonable price to grow and expand in new directions. And they aren’t growing via debt. Like United Online, the print business may not be a great growth business but it does generate a lot of cash. And that is really what made me look twice at the company. Transcontinental is really cheap on a free cash basis. Based on the 2014 year (ended November), the stock trades at 5x the free cash generated. In 2015 they have to start paying cash taxes again so multiple will jump to around 7x. There are not a lot of companies left these days that trade at single digit free cash multiples.

So TC Transcontinental is inexpensive and has plenty of cash available for acquisitions to offset declines or to further facilitate moves into other growth areas. There are the pieces there for something to go right.

An update on United Online

United Online has been a reasonable winner for me so far, going from $12 and change to $17 since I bought it back in November. I did some more work on United Online a couple of weeks ago and I thought I’d put it out there for anyone interested.

United Online is not my largest position. I am not convinced of its prospects and to be honest I don’t even really understand the demand for its StayFriends and Classmates products. Yet I think the stock has a reasonable chance of going higher.

United Online operates a number of legacy businesses that, while in decline, are producing an increasing amount of free cash flow as United attempts to milk them for the cash. These businesses are:

- Social Networking Services – they operate the classmates.com, StayFriends.com and Trombi.com (France) brands

- Loyalty Marketing – operate a loyalty marketing service called MyPoints. MyPoints is an online shopping membership that provides discounts and rewards to users

- Internet Access – operate the brands NetZero and Juno, providing dial-up and mobile broadband services

While these businesses are all declining, and they hardly exemplify the large moat stability that a value investor typically craves, they are generating more and more cash as United squeezes down the cost side. In the fourth quarter free cash generation was $8 million. In the last 9 months its been a little under $15 million.

I’ve listened the last few United Online conference calls and its clear that management understands the predicament they are in. They know that the existing business lines are essentially in either a stasis or prolonged run-off and that they need to do something to generate growth. To that end, United Online is in the process of rolling out three new products: a low cost cell phone, a cloud based shopping list app called List+, and a gift card management app called Swappable. While I don’t really get the cell phone angle, both List+ and Swappable fit well with the existing MyPoints customer base. There is a decent SeekingAlpha article that describes the new products, but its only available for a couple more days.

The Swappable app is a bit of a hot money area right now. United is competing with another gift card app start-up so there is a gift card app star-up called Raise. Raise raised $56mm from investors in January, which values them at a little under $1B. They have “reported hundreds of thousands of customers had either bought or sold cards from around 3,000 brands via the site to date”. While Raise hasn’t said how many users they have. They did say:

In addition, in 2014, the company sold over a million gift cards, and between November and the end of the year, Raise grew over 50% in revenue and other metrics. And user growth quadrupled.

Again according to media reports Raise “passed $10 million in monthly gross card sales several months ago and has been growing more than 10 percent a month since then”. The company takes a 15 percent cut when someone sells a gift card or store credit on their site.

From what I can tell, the Swappable app does pretty much the same thing that the Raise app does. Moreover, United Online can leverage off of MyPoints. From the recent conference call:

MyPoints already does millions of dollars of gift card revenue. It has primarily been desktop. It has been user, going to buy a gift card on MyPoints

So putting it all together, United Online has:

- A comparable product to Raise

- “An ecosystem in place with MyPoints and the other databases around the company”

- “9-plus million MyPoints members we can write and invite to this product”

With cash on the balance sheet exceeding $5.50 per share, United Online has an enterprise value of $160 million at $17. So a lot less than Raise, even though they have a number of other irons in the fire, and an established means of generating capital to plow into the business.

So we will see. But its enough of a story to keep me interested in the stock even as it has risen.

Gold Stocks

In continue to own small positions in Endeavour Mining, Argonaut Gold, Timmins Gold and Primero Mining. These positions are just a trade, premised on the supposition that we have once again gone too far to the downside, just as we went too quickly to the upside in January and before that went too far to the downside in December. But even as I kept all of these positions small, they still led to gyrations in my portfolio, as they saw daily movements in the high single digit and low double digit percentage points. More and more often it is occurring to me that owning gold stocks is not worth the trouble.

What I sold

Mart Resources

I bought Mart Resources at the trough of the last oil stock rout because of what I saw a lot of potentially positive news on the horizon. The company was likely to release news about the purchase of the OML-18 block and show production gains after the commissioning of their new pipeline reduced the existing production bottleneck.

Unfortunately none of this is likely to materialize as the company has sold itself to its partner Midwestern for a paltry 80c per share. This is a case study in why not to invest in a country like Nigeria. Based on the publicly available information it is difficult to make a case for selling the company at this price. This likely means that there is other non-public information that makes a sale of the company compelling, if not unavoidable.

One only has to look at the recent share price, which ticked down to 50c at one point, to illustrate the skepticism of the investor base about the legitimacy of the proceedings. Quite honestly, at this point who really knows what is going on. I sold my shares at a slight profit from my purchase but in relation to what I had expected, which was the opportunity to sell these shares at $1+ within the year, it is a substantial disappointment.

magicJack and Radsys

I group both of these companies together because my motivation for selling was similar; a lack of conviction about their prospects.

In the case of magicJack, I keep coming back to the name as I compelled by its large cash position ($5 per share) and the potential for the company to behave in a manner similar to United Online, milking the legacy business for cash while developing new and perhaps complimentary businesses to facilitate growth. Nevertheless management has disappointed once too often for me to hold my shares through earnings, particularly given that their largest retail vendor (Radioshack) went into bankruptcy during the quarter. I will be listening closely to the conference call though, and could come back to the stock depending on what I hear.

I could be back into Radsys as well. Honestly the problem with Radsys is really my problem. I don’t understand the business that well. The thesis is based on the 4G LTE products that Radsys offers and I just haven’t developed enough background on the offerings to feel confident holding the stock. I’ll try to make time to learn a bit more and come back to the stock once I do.

Earthlink

I exited my position in Earthlink after the company announced fourth quarter results. Its not that the results were particularly bad, its just that they also weren’t notably good, and its difficult for me to envision the catalyst that takes the stock materially higher in the near term.

The company announced flat revenue quarter over for the managed services business, and they really need this business to grow at a reasonable pace given that it is their only true growth driver. And while they announced that they would be reviewing strategic alternatives for their fibre assets, they were vague about what might sold and for how much. If the stock drops back to below $4 I will look at it again.

Transat

It was pointed out in the comment section of my last post that while Transat no longer appeared in my portfolio, I had not actually written about my sale. This was an oversight on my part. These updates get long and at times I miss transactions that I should mention.

To paraphrase my response to the comment, I sold the stock because I thought that the weak Canadian dollar was going to make the winter season (Q1 and Q2) difficult. When you run a business that has mid digit margins and the currency moves 10% in a few months, its difficult to respond fast enough. Transat also unfortunately hedges much of its fuel so in the short term they are not going to benefit from the reduced jet fuel prices. The winter routes also have a lot of added capacity from Air Canada this winter.

All of this came to pass when the company announced weak first quarter results. Now I still really like Transat and I am looking to add my position back, but I’m not sure we are there yet. The second quarter is likely to be just as weak as the first, and the Canadian dollar just keeps on falling. The summer though will be stronger, they will benefit from the weaker Euro and the fuel hedges will begin to run-off. At some point there is a buy here, but I haven’t jumped in yet.

Final Thoughts

Bad things tend to happen when the US dollar is this strong.

Portfolio Composition

Click here for the last four weeks of trades.

{kind=link}