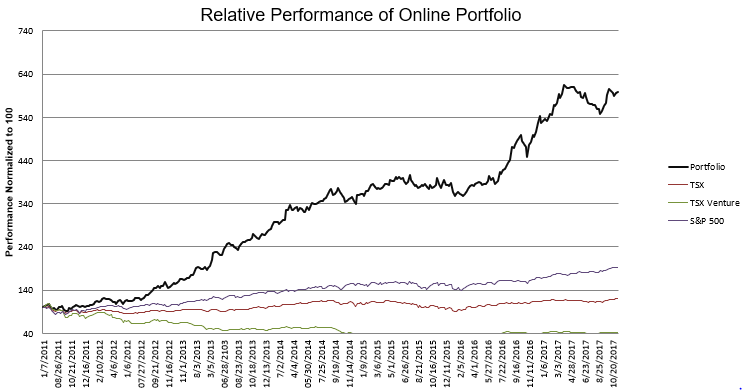

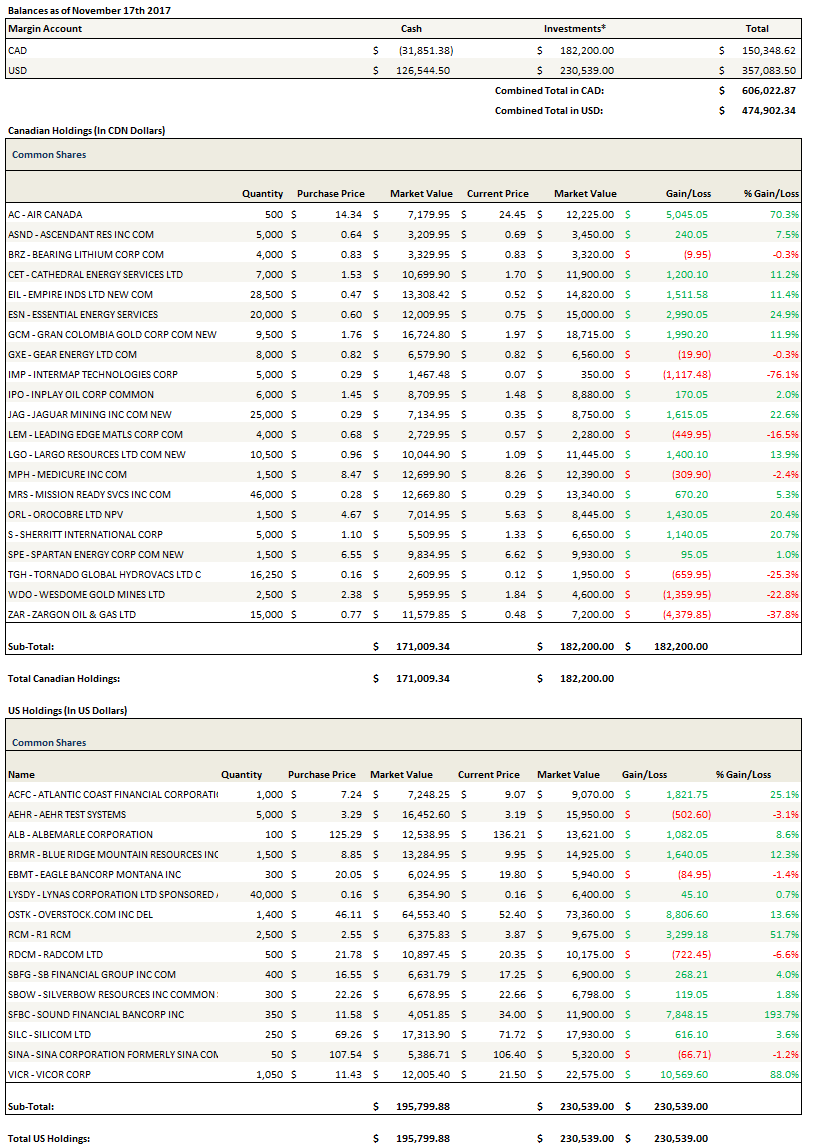

My biggest position right now is Overstock. I’ve already written two posts about the stock (here and here). I actually added to the position some more today as it dipped back into the $40s. I’ve been spending most of my time on the name. Here are a few new thoughts on it.

What is the lending platform worth?

I am constantly re-evaluating the lending platform. The industry is really opaque and its been a lot of work getting numbers that I have some comfort in.

I have found two sources that seem credible. The first is this paper from Beneish, Lee and Nichols. The second is this lawsuit from the pension funds against the prime brokers.

In what follows I am considering the US stock market only. I believe that once this market is proved out, tZero should be able to expand the platform to other market. But we’ll leave that for the future. Right now the big question is whether tZero can make this work in the US. The news on the call that there is indeed $100 billion of inventory and that they had been offered another $6 billion of hard to borrow that very day (as I’ll describe, the vast majority of revenue from stock lending comes from a few hard to borrow securities), is reassuring.

The US lending market generates $4-$4.5 billion of revenue to prime brokers. According to the lawsuit documentation, and also described by Bryne a number of times, the prime broker cut is supposed to be around 60%. But most assume the actual cut is higher because of inter-broker transactions that reduce the cut for the lender. So let’s say its actually 75%. That pegs industry revenue from US equities, including what is going to the lender, at $6 billion.

You can get to a very similar number by using the data from the Beneish paper and this article from the securities lending times, which was referenced in the lawsuit document. The Beneish paper uses IHS Markit data on stock lending rates and volumes. Global equities on loan are $851 billion and the US makes up 55% of the lending market. Therefore total US equities on loan are $472 billion. The average borrowing rate for US equities on loan is about 1.5% (its actually a bit higher but roughly). So that gives a market size of $7 billion. So its in the ballpark of the first number.

You often hear a much smaller average borrowing rate quoted, something around 45-50 basis points. I believe this is because the number quoted is referring to the volume averaged borrowing rate. In fact the number is usually is described as just that: a volume weighted average. The reality of the stock lending business is that 80% of equities are easy to borrow and fetch a very small rate (33 basis points). So most of the volume generates very little revenue. The majority of revenue comes from a few hard to borrow stocks. To give perspective, and its a rough calculation because all the data isn’t there, but I calculated that around 50% of revenue from stock lending comes from the 5% most hard to borrow stocks when I used the tables and data from the Beneish paper.

So I’m going to assume it’s a $6 billion market. Byrne has said that they want to cut fees by 50%. He has also said the tZero/lender split will be 20/80. That gives a total addressable market of $600 million for tZero. I expect that to be very high margin revenue, though Overstock hasn’t given us any numbers to put to margins yet.

One consideration that I haven’t accounted for is the impact of collateral on the prime brokers numbers. I’m still fuzzy on how this will work. I believe that the prime broker revenues quoted are fee only revenue. However the prime brokers also makes some money from holding collateral of the borrower. Some of this collateral return is passed back to the borrower as a rebate, but the rest is profit to the prime broker. I don’t know how the collateral will be considered with tZero, but if the lenders are now going to participate directly in the interest generated, that may be included in that 20/80 split, which would make my above estimates low.

Even ignoring the collateral, the opportunity is considerable. At 10-20% market share, which should be a reasonable objective if the platform is successful, tZero stands to generate $60-$120 million of high margin revenue. An 8x revenue multiple on $120 million puts you at $1 billion valuation.

Of course there are plenty of folks that don’t think tZero will succeed in capturing any of the market. I guess that’s what the next few months will prove out. For what its worth they’ve gone from $0 to $100 billion in two months. And they’ve brought on board Quantum Fund and Passport, who presumably aren’t making their investments in Overstock because of their desire to make a play in e-commerce. But we’ll see.

What is e-commerce worth?

The second element I’ve spent time on is e-commerce. To be honest, for the longest time I was scratching my head about the e-commerce numbers I was hearing. Marc Cohodes estimated in his Grants presentation that the business could fetch $70+ in a sale. D.A Davidson valued e-commerce at $58.

When I was stepping through the valuation, I had trouble coming up with those numbers.

Starting with the existing business, I calculated that EBITDA from e-commerce (after eliminating the losses from Medici) for 2015, 2016 and 2017 were $33 million, $31 million and around $18 million for this year.

Byrne said on the third quarter call that there would be “hundreds of basis points of synergies” if they got together with a “bricks” retailer. I assumed 200 basis points. Presumably there would also be sales growth from the membership base of the “bricks” acquirer being directed to Overstock to shop. I assumed 20%.

With all these assumptions the best I could come up with was about $80 million of EBITDA including all the synergies. That made it hard to justify where the big buy-out numbers were coming from ($70 per share is about $1.75 billion before considering the Soros and Passport dilution, or more than 20x EBITDA including all the synergies).

But then I found something I missed the first time on the conference call. @teamonfuego, who has been working on Overstock valuations as well, pointed to this passage late in the call. My underline:

Yes, so this synergy goes both ways. So for example, if we were combined with a large chain, these large chains have similar logistical footprint. They typically have a dozen or so mega distribution centers, each of which are feeding a couple dozen distribution centers, each of which are feeding 10 to 15 stores. If we were integrated with such a company, we could overnight I mean, you would have a system that was competitive with Amazon, fulfillment by Amazon or even nicer than fulfillment by Amazon in several ways. We built, this thing, Saum and Stormy, actually, built some years ago, SOFS. This thing we called SOFS is a software logistics system for an agile network supply chain. We’ve only had it hooked up to our 3 distribution centers, but it could be hooked up to thousands, and it was actually built to be hooked up to as many as we wanted, you don’t need thousand, you need a dozen. So just by, for example, if we were part of a large brick-and-mortar chain, that itself was like $200 million, $250 million of various logistics cost, all right to the bottom line.

I’ve actually talked to a couple of people now that acknowledge that e-commerce logistics are a problem for many of the bricks retailers, and a solution to that problem could be quite coveted.

So who has thousands of distribution centers? Well this article from Forbes is interesting. So I’m not at all saying that Walmart is a potential acquirer, but more generally the article talks about how Walmart specifically but also other bricks retailers are embracing what is called omni-channel commerce. Omni-channel commerce is essentially the process of turning each store into a distribution center. A number of the chains mentioned, along with plenty of others, would have the 1000’s of stores that would make the logistic cost reduction realized. The concept aligns pretty well with what Byrne is talking about above. Needless to say this can change the e-commerce valuation substantially.

Curious Transaction

One of the first things that caught my eye the day of the third quarter earnings release was this disclosure in one of the 8-K’s.

I found it very curious. Why would Overstock terminate an existing loan and lease agreement in order to make a similar loan with Patrick Byrne’s family?

I found it very curious. Why would Overstock terminate an existing loan and lease agreement in order to make a similar loan with Patrick Byrne’s family?

Indeed I was not surprised when I saw that this transaction was picked up by a few of the shorts on twitter a couple days later. They pointed to it as an example of a questionable related party transaction. I can’t disagree, it’s certainly odd. But I wonder if it’s missing the point.

I dug into exactly what the master lease agreement was for. As it turns out, Overstock entered into the MLA on November 25th 2015. The lease is to “finance certain software and/or software licenses(s) (“Licensed Software”), software components, including but not limited to, software maintenance and/or support“.

The lease and debt agreement occurred close to the time of the closing of the acquisition of SpeedRoute. The purchase was initiated in August 2015 and it closed some time before the beginning of 2016. In fact the day before, on November 24th, Overstock issued an S-3 amendment for potential selling stockholders from SpeedRoute of Overstock stock.

The timing makes me think there’s a pretty good chance these are Speedroute’s assets that Overstock is doing the MLA for. Reading through the MLA, those assets were secured by Overstock’s land and building. So you had tZero software secured by Overstock.com assets.

I have to wonder if Overstock cancelled the loan and MLA in order to disentangle the two entities. Byrne decided to take on the loan and MLA himself (via his family) as a short term plug. Keep in mind there was no reason to end the relationship with US Bank. The agreement extended to 2020. Also, the terms of the loan to Byrne’s family was at a higher interest rate, so this couldn’t be construed as an economic . Obviously the optics of leasing out from your own family are unfavorable, and I can’t see doing that unless you had another motive.

I may be totally off base about this, but I just have to think you don’t make this change unless you are pretty far down the road to some sort of separation.

Bitt

While all the focus is (rightly) on tZero, Byrne did point to Bitt as his second most promising investment. I knew Medici owned 11% of Bitt but didn’t know they could own up to 35% with warrants.

Bitt is in the business of digitizing currency to the blockchain for governments. they are “creating digital wallets for citizens, for people, essentially frictionless payment system, including remittances, which incidentally are a $500 billion industry globally, remittances alone, on which the vig is about 15%.”

Bitt is close to completing their first use case in Barbados. Catlin Long (from Symbiont) commented on this on her blog back in 2016:

More central banks in small countries will follow the lead of the central bank of Barbados, which green-lighted a blockchain start-up called Bitt to create a digital Barbados dollar that uses Bitcoin’s blockchain as an alternative method for settling foreign exchange. Small central banks are searching for alternatives because local banks are losing access to US financial system, owing to the retreat of American correspondent banks from small countries — a trend called “de-risking.” This is choking off trade, which is the lifeblood of most small economies. Folks, this an unintended consequence of laws requiring U.S. banks to comply with strict anti-money laundering and know-your-customer regulations. These laws are hurting the developing world — and, ironically, boosting Bitcoin as a valuable alternative payment system. Kudos to Barbados for its creative solution!

Byrne said on the call that Bitt’s development in Barbados is undergoing 4 weeks of testing. So its pretty close to coming to fruition.

I mean, this thing has a global application, and what I think the first to market with the kind of wallet we’re bringing to market, I just saw, I mean, it’s all in testing. It’s all done. It’s all being tested for another 4 weeks, it’s really slick. It’s really better than anything I’ve seen in the market, that’s a potential enormous business.

While I don’t really have a sense of what the addressable market is for a digital currency, I suspect if the blockchain really does snowball and become the preferred method of recording transactions, it would be pretty big. If Bitt can be first to market with a successful launch in Barbados, I think that the company is probably worth quite a bit (pun intended).

A few other random thoughts

1. On the conference call Byrne said that “the market” wanted Overstock to get their ownership in tZero down to below 50%. I think that makes sense for optics. It makes me wonder if we get some sort of divestiture announcement before the ICO. Maybe selling a 20% stake to a strategic investor, which along with the ICO would take the overall stake down to 50%? Purely speculating here but it would seem to make sense to do that before the ICO. I didn’t really understand the whole “bitcoin fork” reason for the 15 day delay.

2. The securities purchase agreement for the Quantum Fund is lacking the normal disclosure that no non-public information has been exchanged (h/t 20slots for this). Note that in the Passport agreement, the statement is present (any information that constitutes or could reasonably be expected to constitute material non-public information…)

3. Who was the man in the next room?

4. There was some insider selling over the last few days. At a glance it appears like they were selling out, but after closer inspection its clear that each of these insiders own significant amounts of restricted stock. For example Sam Noursalehi, President of Retail, sold 5,000 shares. He owns 48,000 shares of restricted stock in addition to the remaining 11,000 shares he owned. I’m not too worked up about these sales.

5. The shorts have been out in full force on Overstock. Lots of tweets and articles. I’m actually somewhat comforted that so far, while I can see that the shorts are digging through IP addresses, looking for backdoors to tZero platforms and searching through the Linkedin connections, I haven’t really seen anything that scares me that much. Of course that could change tomorrow. I’m sure there will be another article.

{kind=link}