Week 246: Hidden in Plain Sight

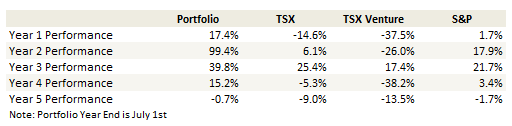

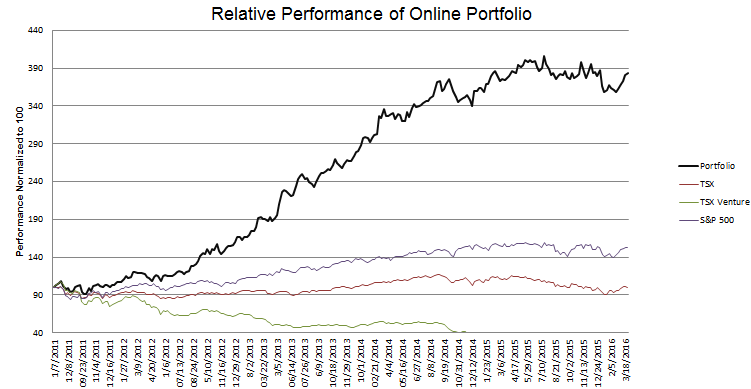

Portfolio Performance

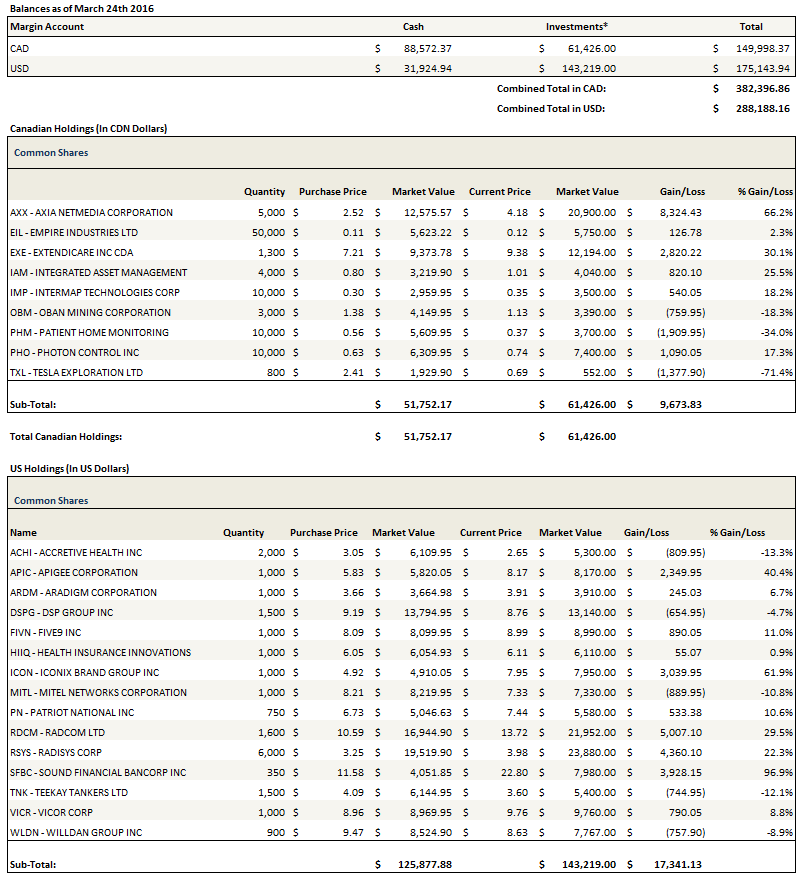

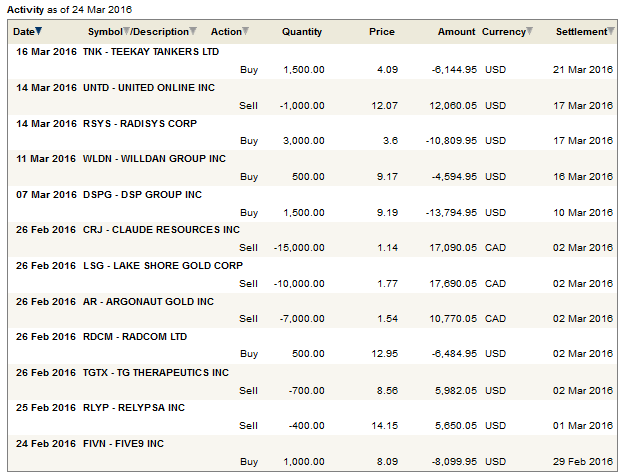

See the end of the post for the current make up of my portfolio and the last four weeks of trades

Thoughts and Review

The market was up and so not surprisingly I had much better performance in the last month. Even so, I performed better than I might have expected given just how much uninvested cash I have sitting around.

It just goes to show how much of a drag the losers have been. I’ve had my share of winners in the last year, but my performance has been flat because I also had a bunch of crappy losers.

It would be one thing if I couldn’t distinguish between the winners and losers ahead of time. But when I look back at what has cost me over the last year, it has been pretty predictable; stocks where I am stretching for a trade, stocks where the value wasn’t clear, or stocks where my primary motivation was their attractive yield.

I’m going to make a concerted effort to prefer cash to those positions going forward.

In the last month I haven’t been actively looking at stocks. I’ve been surprised by how quickly the market has bounced back and I remain skeptical that it can continue. So with the exception of a couple of opportunities that I will describe below, I am will remain holding a high cash position until I see a reason to believe the market will sustain a move higher.

Takeovers!

I went a long time without a takeover and then in the matter of 6 weeks I got 3 of them. First, both of my gold stock picks, Lake Shore Gold and Claude Resources, were taken over. I bought Lake Shore at $1.12 and, after the takeover offer from Tahoe Resources to exchange each share of Lake Shore for 0.1467 shares of Tahoe, the stock now trades at a little under $2. I bought Claude at 76c. Silver Standard Resources made an offer of 0.185 shares for every share of Claude. At the time of the offer this amounted to $1.65. I’ve sold some of each position and so have reduced stakes in both. They have been solid performers and I am not unhappy.

A few days after the Claude Resources news my long held fiber-to-the-home play, Axia NetMedia, got scooped up by a private equity firm, Partners Group. While I was happy to see a quick takeover of both of my gold stock positions, I was more divided by the news from Axia.

The problem is that the opportunity at Axia is much greater than the $4.25 takeover offer. The company has a massive build out on its horizon in both France and Alberta. Its becoming clear that fiber-to-the-home is not just a “higher speed-nice-to-have” but a necessary conduit to access all forms of media. Axia’s cash flow stream once this build-out is complete will far exceed the price paid by Partners Group.

The problem is getting from here to there. As Axia outlined on their last conference call, the capital necessary to realize the growth is a stumbling block for a $200 million Canadian company. Axia warned on their last call that they were evaluating alternatives; that they would try to raise capital and if not consider offers by a larger entity with greater access to capital. Partners Equity is a $50 billion investment management firm. The only reason that a firm that large bothers with a takeover this small (Axia was a $200 million market capitalization before the offer and under $300 million at $4.25) is because they see significant upside.

Radisys, Radcom, Willden, and what the Market Misses

I’ve made a number of mistakes over the last couple of months but one thing I have done right is add to my positions in Radcom and Radisys in the face of market weakness.

Radisys has had a big move in the last month, moving as high as $4 from $2.50 in January. I have added to my position on the way up.

The Radisys move over the last couple of weeks has been instructive. Consider that during the fourth quarter conference call the company announced a large contract from a Tier I customer (from this transcript):

And finally, and maybe most important in this release is, we secured orders totaling approximately $19 million, the majority of which is contained in deferred revenue at year-end for our new data center product targeted at telecom and cable operators which we expect to launch more broadly in the coming months.

The stock moved a little but nothing that couldn’t be explained by what were decent quarterly results.

About three weeks later Radisys officially announced the product, DCEngine, with this press release, along with the name, details and comments from the Tier 1 customer, Verizon.

“As Verizon introduces open, flexible technology that paves the way for central office transformation, we look to companies like Radisys to assist us in that journey,” said Damascene Joachimpillai, architect, cloud hardware, network and security, Verizon Labs. “Network modernization will rely on solutions such as DCEngine that meet service provider needs with open source hardware and software technologies.”

The stock has moved straight up since this press release.

I think this demonstrates how poorly small cap companies like Radisys are followed and how slow the market can be to react to positive developments. While I find it easy to second guess myself when what I construe as good news in announced and the stock doesn’t move, it is worth reminding myself that this isn’t always an indicator of importance.

With that in mind consider the following situations, Radcom and Willdan Group, two stocks I have had in my portfolio for some time, and Vicor and DSP Group, two new positions that I have added. I believe all four of these situations represent similar “hidden in plain sight” opportunities.

Radcom

First, Radcom. Radcom announced in early January that they had signed a contract with a Tier I customer for their next generation service assurance solution MaverIQ. There wasn’t a lot of details provided, only that the initial phase of the contract would be completed mostly in 2016, and was worth about $18 million.

On their fourth quarter conference call in mid February the company gave more color. They said the contract for NFV deployment was much bigger than the $18 million announced. I’m pretty sure its with AT&T.

While they declined from giving guidance (historically the company has given virtually no guidance in the past so this was no surprise) they were willing to say that they expected their cash level to increase to $20 million from current $9 million by end of the first half of 2016, and that the increase in cash would be due to new revenue and not deferred payments.

They also gave an indication of just how big the deal with AT&T might be (my bold):

We just said that we received an $18 million initial deal out of a bigger deal. There is – it’s a large transformation, so it’s not – I think when you’re envisioning it, so I’m going to try to help you model it, right. So when you’re envisioning it, envision something between 2.5 to three year evolution for the very significant portion of the transformation, okay. It doesn’t mean that everything stops after three years, but envision that over the course of those three years, that number $18 million that we’ve disclosed is just an initial number out of something bigger, that’s bigger than that. And I can’t disclose the accurate numbers here. There is things that it depends on. There is – it’s more complicated just throwing other number out there, but it’s much bigger than $18 million, okay.

In addition they made it clear that they are ahead of the competition, witnessed by their comments about Netscout on the call. They are in the process of trials with other Tier 1 customers and believe that the next-gen service assurance market will be a “winner takes most” market where they can take the most.

Radcom is a $130 million market cap company. They just said they can generate $10 million of free cash in the first half of 2016, that the contract they have announced is actually much larger than the announced number, and that they have a product that is significantly better than the competition.

If Radcom can win a couple more contracts in the next year the stock should trade significantly higher than it is now. it probably gets bought out at some point. In the mean time I think its quite a good growth story. The market is really not paying a lot of attention to the “color” provided on the conference calls, and instead is focused on the rather puny revenue that the company generated in 2015 ($18.6 million) and the rather lofty valuation for the stock if you use that backward looking measure.

Willdan Group

Update: I got a response from Willdan IR and they say the revenue is not new revenue and is included in guidance. I am still of the mind that this is an expansion of scope though and I am happily holding the position I added that I describe below.

Second example. On their fourth quarter conference call, which I thought was quite positive in terms of the outlook provided for 2016, Willdan stated the following about their ongoing contract with Con-Ed:

We have the extension for 2016 at a value of approximately $33 million. We’re prepared to go beyond this baseline and expect to. The good news is that we continue to perform well for Con Ed and as a result we are in discussions to expand our scope of activity in the second half of 2016 to include more programs targeting customer segments, for example, more of Brooklyn, Queens and larger projects, 100 kW to 300 kW in our SPDI program, the type of programs that will include in the larger retail stores and warehouses and more real estate.

Note that the transcript is incorrectly referring to the SPDI program, which should read SBDI (small business direct install program).

Flash forward to Thursday. In a press release Willdan said the following:

Willdan Group, Inc. (“Willdan”)(WLDN) announced that it has been awarded a one-year, $32.8 million modification from Con Edison to an existing Small Business Direct Install (SBDI) contract. Under the modification, which extends through the end of 2016, Willdan will be delivering approximately 86 million kilowatt-hours in electric energy savings to Con Edison’s small business customers throughout the entire Con Edison service territory. This includes the Bronx, Brooklyn, Queens, Manhattan, Staten Island and Westchester County, New York. Willdan described this forthcoming modification in its recent fourth quarter earnings conference call.

Based on the language used it seems pretty clear to me that the $32.8 million is in addition to the $33 million baseline contract. They talked in the fourth quarter conference call about scope expansion with respect to the SPDI and this is scope expansion to the SPDI.

If I’m right, then the market hasn’t caught onto this yet. Full year guidance is $170-$185 million and so $33 million is significant.

It’s possible I am wrong. Maybe Willdan is just re-releasing old news. I would be surprised though. I have followed the company for some time and their management does not strike me as the sort to throw out a press release with a big number that is a rehash of an already disclosed contract. It just doesn’t strike me as something they would do.

I think its equally possible that this was the Thursday before a long weekend, that there are maybe one or two analysts following the company, and so no one that was around to check the news cared enough to notice it. Yet.

For what its worth I added to my Willdan position significantly. What the heck; I’m buying the stock at the same price I was buying it at a few weeks ago before this announcement anyways. What’s the downside?

DSP Group

I have been watching DSP Group for a couple of years and have owned it once in the past. The previous time I owned it the story was primarily one of valuation. The stock was trading at $7 and the cash and investments on the balance sheet accounted for nearly $6 of that. But there wasn’t a clear story behind the business itself and so I sold the stock after it went a few dollars higher.

In the two years since the story around the company’s business has been evolving for the better. The legacy business that they have, and for which I had a lack of excitement in my first endeavor, is the design and manufacturing of chipsets used in the cordless telephones. It’s profitable and brings in decent free cash, but it’s an industry in decline to the tune of 10-12% annually in recent years.

This business has fallen off the cliff even more in the last couple of quarters. Slower demand and an inventory build has led to 20% plus year over year declines. These declines are expected to moderate back to trend in the second half of the year. However the bad numbers drag down the overall revenue numbers for the company and are hiding some pretty decent growth businesses.

DSP Group has been investing in a number of new technologies that are starting to bear fruit. Lets step through them briefly:

- HDClear – they have developed a new technology that will improve voice quality on next generation phones. On the fourth quarter call the company announced that they had a couple of wins and one of the wins was with a Tier I device supplier. Turns out that is Samsung, where it has been designed into the S7. They expect $2 million to $3 million in the first quarter and guided to lower double digit or high single digit revenue for the year. When I look at some of the numbers I wonder whether it could be higher: according to this article from Reuters (here), DSPG should get 70c-$1 for each HDClear chip sold. The Samsung S6 sold over 50 million units last year.

- VoIP – their VoIP business unit had $22 million in revenue in 2015. They have guided for 50% growth in 2016.

- IoT – Eight OEM’s and three service providers have launched products based on DSPG’s ULE technology. They have a ULE chipset that can be used in home automation, security, remote healthcare or energy management products. They generated $3.8 million of revenue in 2015 and they think that can get to $5 million in 2016.

- Home Gateway – Home Gateway generated $14 million in 2015. It is expected to take a step back in the first quarter of 2016 with around $2.5 million of revenue, but this is going to climb as the year progresses and some new product launches, in particular a North American telecom provider.

- SparkPA – DSP Group announced a new product, a power amplifier to be used in the high end access point market. They don’t expect any revenues from this business in 2016 but it will ramp in 2017 and they consider the market they are tapping to be over $100 million

The company gave quite a bit of color about the revenue expectations for each of these businesses in 2016 on their fourth quarter conference call. If you add up the expected 2016 revenue from the new businesses alone you get around $57 million. These businesses grew at 35% in 2015 and the company said that in aggregate they expect higher growth in 2016.

When I think about a company with an $80 million enterprise value and $57 million of high growth revenue products, it doesn’t make a lot of sense to me. I understand that overall the company’s revenue is not growing because of the out sized contribution of cordless declines. But this business is profitable and therefore not a drag on the company, in fact it even helps fund the growth.

I think the stock should trade at least at 2x the revenue of its burgeoning new product lines. This would be a 50% upside in the stock. If the growth continues I would expect it to be even higher.

Vicor

I got the idea for Vicor from a friend who emails me regularly and goes by the moniker Soldout. He gave me a second idea some time ago, called Accretive Health, that I didn’t initially buy and has done really poorly for the last half a year but that I added recently and will talk about another time.

As for Vicor, the company has a market capitalization that is a little under $400 million, $60 million of cash on its balance sheet and no debt. The company sells power converters. They offer an array of AC-DC and DC-DC converters that are used in telecom base stations, computers, medical equipment, defense application, and other industries.

Vicor has a history of high-end products and so-so results. Their technological edge goes back to the 80’s, as they were the original inventor of the DC-DC brick converter, a device that allows the power converter to sit on the circuit board, which in turn allowed a single DC voltage to be distributed throughout the system and converted as required to lower voltages. However they haven’t made a significant profit since 2010, and even then it was only 80c per share.

The story going forward is simple. The company says that with recent design wins and product launches, in particular wins for new data centers that will utilize the VR13 standard (more on that in a second), as well as high performance computing, automotive and defense, they can grow revenue 3-5x in the next couple of years. That estimate comes directly from management (from the third quarter call).

I think it’s fair to say that the array of products that have been introduced and the products which are about to be introduced, for which the development cycle has ended and we’re very close to new product introductions, that in the aggregate these products are more than capable of supporting the 3-by-5 revenue growth goal that we had set for ourselves, and with respect to which we suffered delays.

The increases in revenue in 2016 will coincide with the move to the VR13 class of processors made by Intel (known as the Skylake family of processors) and that are used in a number of high end computing applications. These processors require power conversion levels that are easily addressed by Vicor’s high efficiency products. Vicor has already had a number of design wins to be included in VR13 system designs. The move to a VR13 based architecture has been slower than expected though, and the company has pushed back the revenue ramp from originally beginning in early 2016 to now occurring in the second half of the year. The company describes the VR13 opporunity below:

VR13 is a class one processor, it’s a class of processors, and it’s processors that in many respects represent the significance that [inaudible] performance relative to the earlier class, which is VR12.5. Now this can be potentially look confusing because, as you follow Intel’s introductions with respect to the many different flavors of these devices, some of them play in a space where now we do not play, and other ones are targeted in particular to higher-end datacenter, more intensive — computing intensive applications. And those are the ones that are relevant to our revenue opportunity.

Vicor has significantly more design wins for the VR13 product line than they did for VR12.5 (again from the third quarter conference call):

To the extent our footprint with factorized power solutions across applications and customers will increase going from VR12.5 to VR13, this product transition is a mixed bag as it may cause near term softening in demand but should result in substantially greater total revenue as VR13 applications begin to ramp. On a related note, we have started to see significant design wins for our new chip modules as point of load, board mount devices and in chassis mount VIA packages, which validates our expectations of market reception of these products.

Vicor’s technology differentiates them from competitors. For example they have introduced a factorized power 48V architecture that includes components that can step down voltage directly from 48V to 5,3 and 1V without an intermediate 12V stage. I believe they were the first company to come up with this solution and I have only seen one other advertising the capability. Stepping down directly from 48V has higher efficiency and takes up less board space than existing architectures. On the third quarter conference call the company said the following:

In my recent visits to customers in the U.S. and Europe, I confirmed spreading a rising level of interest in our factorized power 48-volt architecture and are now frontend solutions for automotive, datacenters, high-performance computing, and defense [ph] electronics applications among others.

The 48V products are particularly interesting to data center and server applications where power losses due to the intermediate step-down to 12V are undesirable. Google, for one has championed a 48V server solution with a new 48V rack standard. Vicor released a press release describing Google’s initiative:

Patrizio Vinciarelli, President and CEO of Vicor, commented: “By developing its 48V server infrastructure, Google pioneered green data centers. And by promoting an open 48V rack standard, Google is now enabling a reduction in the global cloud electricity footprint.”

The company has been building out their capacity and their existing cost structure can support the anticipated rise in revenue.

So we have significant design wins. We have been working furiously to establish automated manufacturing capacity. There’s been good progress to that end. You know, there’s equipment coming in, factory flaws, have been prepped for it, and we’re going to have a turn now in the very near future in anticipation of volume ramp in Q1 of next year.

If you step through how the numbers would play out and assume that revenues double at some point, a modest increase in SG&A and no improvement in gross margins as revenues ramp, you can see the leverage to earnings that quickly develops. Note that the company has significant net operating losses that will shelter them from tax:

Keep in mind that I’m not trying to exactly predict how earnings will ramp. This is not intended to have the accuracy of a forecast. Its intended to demonstrate the magnitude of the earnings leverage if the company can make good on their expectations.

I have a position in Vicor and expect the stock to move significantly higher if they can realize their revenue expectations.

Tanker Stocks

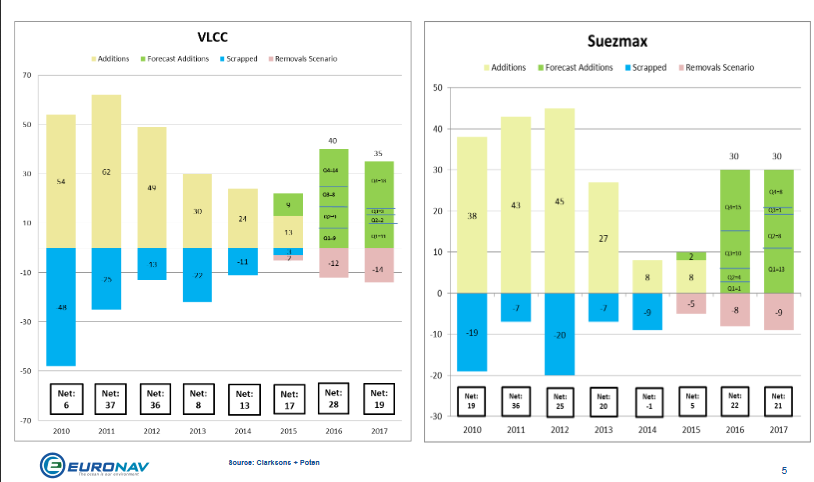

After watching the tanker stocks dramatically under-perform for the last two months I decided to take a closer look. I concluded that you can attribute the negativity entirely to the order book for Suezmax and VLCC’s over the next couple of years. The slide below is taken from the Euronav September 2015 presentation.

Note that since that time the gross additions for Suezmax have fallen by 3 in 2016 and risen by 15 in 2017, while gross additions have risen by 5 in 2016 and 5 in 2017 for VLCCs.

The rule of thumb on VLCC demand is that every 500,000bbl/d of demand requires about 15 ships. The new ships being added covers somewhere between 1Mbbl/d to 1.5Mbbl/d of additional demand. This seems to be inline with 2016 demand expectations, which I believe are around 1.2Mbbl/d according to the EIA.

Some of the new build activity was likely a rush to procure ships before the introduction costly NOx Tier III compliance requirements which adds an additional $2 million to $3 million to the price of newbuildings (source here)

Adding it all up, this seems like a balanced market to me. But the stock prices of the tanker equities are trading like a dry bulk type oversupply was about to occur. I think the extremely low prices we are seeing in these stocks will be corrected at some point during the year, if for no reason other than the typical rate spikes that we see periodically.

I have taken a basket approach and bought positions in Teekay Tankers, DHT Holdings and Ardmore Shipping. Of all these names I think I like Ardmore Shipping the best because the order book for product tankers, where Ardmore has all of its fleet, is the least concerning but also think that in the $3 range Teekay Tankers seems particularly overdone.

These should be viewed as trades. A move to $5 in Teekay, somewhere in the $11s for Euronav, $6.50 for DHT or $10 for Ardmore and I will cut them loose. All of these price targets are well below where the stocks traded at the beginning of the year. I just don’t think conditions have changed that dramatically to warrant the change in stock price.

Portfolio Composition

Click here for the last five weeks of trades.

{kind=link}