Week 290: Renewal

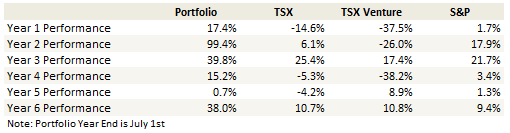

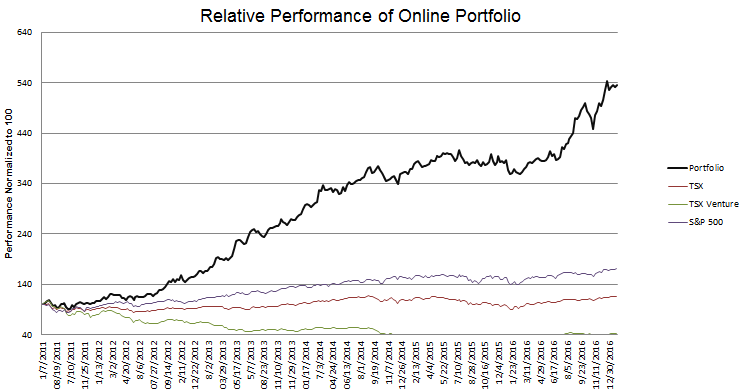

Portfolio Performance

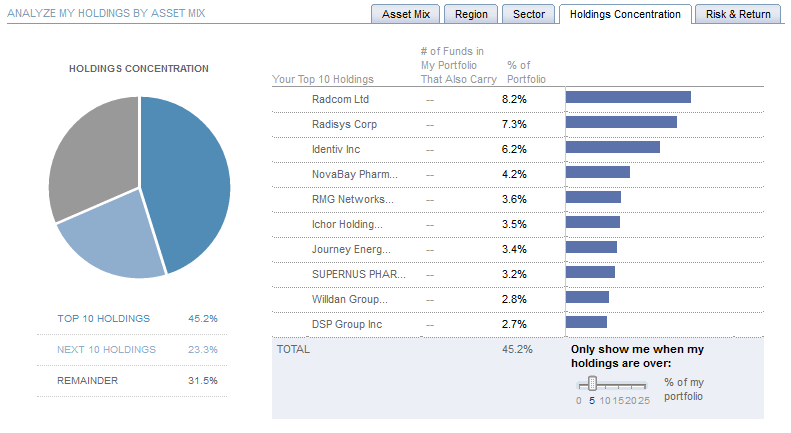

Top 10 Holdings

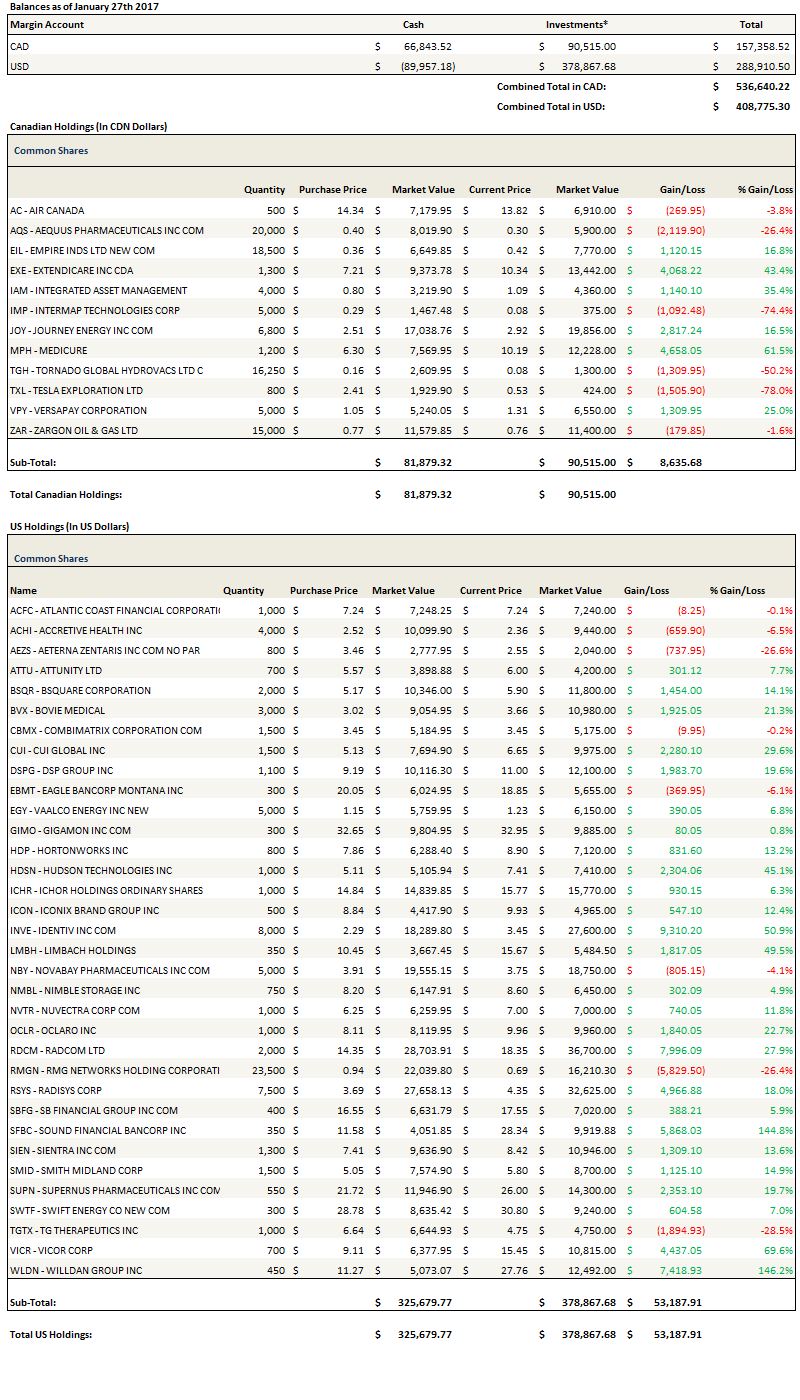

See the end of the post for my full portfolio breakdown and the last four weeks of trades

Thoughts and Review

I came into the new year wanting to reduce my exposure. I had racked up gains last year that I had held onto for tax gain reasons. It’s also been a good run, and there are at least a few signs that the market is topping out.

I also find too much exposure leads to poor decisions. The lack of cash causes me to ignore ideas I might otherwise pursue and I start to feel stuck with the positions I have. I end up “hoping”.

When it comes to investing “hope” is a dreaded word for me. Hoping that a takeover happens. Hoping that a news release comes out. Hoping that this quarter is different.

Moreover, hope is inextricably tied to patience and patience, while not so toxic as hope, has a love/hate relationship with me. Patience is necessary. You have to wait to have your ideas play out. And I do this. I sat on Willdan for 3 years before it decided to more than triple in 6 months. You can’t cash out on the first gain or jump ship on the first sign of loss.

But too much patience, at least for my style of investing, is counterproductive. It wastes capital of all kinds. When I am too patient with my positions it also means I am not looking for new and better ideas.

So every so often, maybe once or twice a year. I take a hard look at every position and ask myself if I really want to own it? Do I really believe in this idea? And I force myself to sell at least some of them.

I have to go through a renewal. I sell off a bunch of positions, reduce a bunch of others, and, at least in terms of my own mindset, I start over.

I did my last big reset last January and that one was sparked by the market moves. It was not pleasant. This reset was more minor. I shook things up enough that I could refresh my perspective. It seems to be working so far.

Changes to the Portfolio

I sold a number of energy positions: Jones Energy, Resolute Energy, Gastar, Granite Oil and Key Energy Services. I didn’t time these sales particularly well, as many of these names have rallied further after I sold.

You might ask why I sold Key Energy Services so soon after buying them? Partly it was logistics; in the account I track with the practice portfolio I wanted to raise cash and so I had to look for names to sell.

Second, it had appreciated 20% from my original price and, in light of my first reason, seemed like an easy gain. Energy services is a tough business and so this isn’t a stock I wanted to hold for a long run. Nothing has changed with the company though, and in my actual account I still hold my warrants, which give me exposure to upside in the stock.

I also sold Contura Energy. I did more research on the met and thermal coal market and I concluded it was more likely that coal prices would decline than increase. In particular, much of the increase seemed to be because of closures in China that could just as easily be reopened and there was evidence that was already happening. I’ve been in and out of the coal market since 2006, I know how volatile it can be (especially met) and I also have experienced that when the coal price is declining it doesn’t necessarily matter how cheap the company appears, the stocks will follow the price of the commodity. Maybe that won’t happen in this case, maybe Contura is “cheap enough”. But I couldn’t ignore the precedents I had seen.

Even with these changes I still don’t have enough cash in the practice portfolio. I’m running about 20% cash in my regular portfolio and am a little less than flat with the online account.

As for my remaining positions…

I still have reasonably big positions in Radcom and Radisys, but along with many other stocks I reduced these positions as well. I am balancing my expectation that the first and second quarter results from each of these names will likely be modest with the awareness that positive news in terms of new contracts could happen at any time will send each stock much higher. However I did decide to add a little Radcom back on Monday, which is not reflected in the update.

I also reduced Willdan. Its just gone up so much. I took some off at $27 and $29, which turned out to be a little early as the stock briefly hit $31. I don’t plan to sell any more; I still really like where the company operates (energy efficiency), they should see some benefit from infrastructure plans, have the ability to pull together cheap accretive acquisitions and will also benefit from changes to the tax code (their tax rate has typically been above 40%).

Finally I reduced my positions in Attunity, Hudson Technologies and Nimble Storage. I’m not completely confident that the results for these companies in the next quarter are going to be stellar. I prefer to wait to see the results an add back depending on the reports.

And a few new positions…

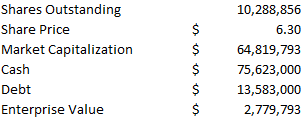

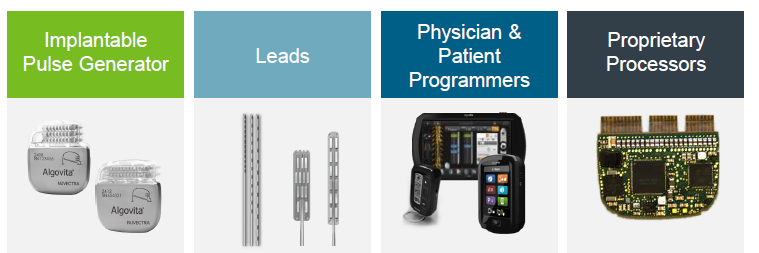

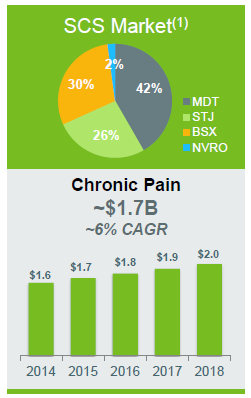

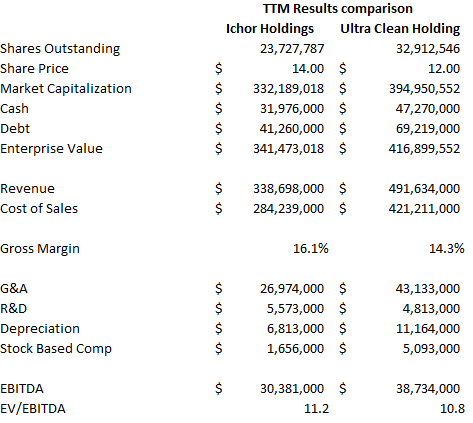

I took five new positions in the last month. I wrote up two of them, Ichor Holdings and Nuvectra.

I tweeted that I took a position in Vaalco Energy (hat tip to @teamonfuego)

Also h/t @teamonfuego for pointing out $EGY, small offshore Gabon producer, not big growth but very cheap, operational issues under control

— LSigurd (@LSigurd) January 27, 2017

And I tweeted that I took a position in Combimatrix:

bought 2 new small biotechs $NVTR, trading at ~cash, ramping neurostim therapy, $CBMX h/t @teamonfuego, also low EV, ramping diagnostics

— LSigurd (@LSigurd) January 27, 2017

I have a write-up in the works about Combimatrix and have plans for one on Vaalco after that.

The last position that I took was in Gigamon. I have written in the past that I been waiting for this stock to correct and continually regretted not buying it when it was lower. The company announced poor numbers for the fourth quarter and the stock took a massive beating. I was happy to step in. The stock could go lower but I am not convinced that their announced portends a trend so I wanted to get at least started with a position here. If the stock dipped into the $20’s, I would double down.

Last Thought

I’m very edgy about Trump and his economic agenda. Given the role that Steve Bannon has taken on, its worthwhile to read and listen to what he has said. I might do a more detailed write-up on this in the future, but for now consider this speech. Bannon’s ideas remind me of what you hear from gold bugs and all those economic podcasts that portend the financial end of the world. He talks about the contingent liabilities, the trade deficit with China, its all those things you hear from the newsletter writer/economic podcast cohort. Some of what he is saying has merit, but if he is going to attack what he sees wrong I don’t know if this plays out well.

Portfolio Composition

Click here for the last four weeks of trades.

{kind=link}