I took a ~3% position in ChipMOS Technologies (IMOS) last week. It hasn’t quite worked out the way that I had hoped. I’ve had a tiny starter position in the stock for a while, but I up-sized that position significantly when I added at $16 last week. It closed at a little under $15 on Friday. As I wrote in an email to a friend:

I overreacted with IMOS. Totally misread the TW emerging market exchange listing. Thought the closing price of 8150 was a game-changer event. Not so much.

Perhaps not as eloquent as I would like but it gets the point across. I’ll elaborate below.

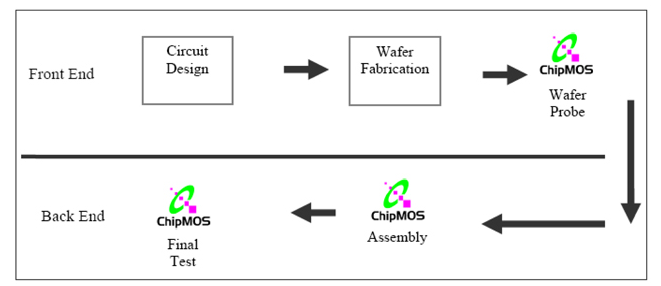

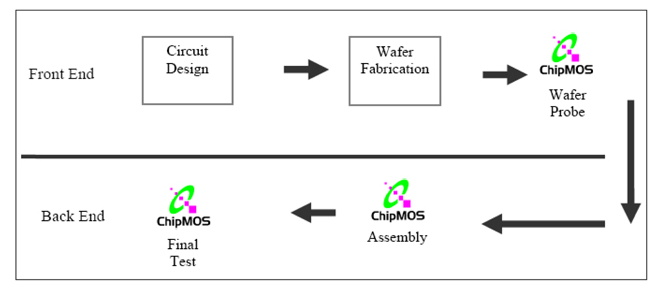

ChipMOS provides assembly and testing for memory and logic/mixed signal semi-conductors. The following diagram illustrates where ChipMOS fits into the semi-conductor manufacturing process.

In 2012, the company derived 29% of revenue from testing of memory semi-conductors, 33% of revenue from assembly of memory semi-conductors, 23% from testing and assembly of LCD semi-conductors, and 16% from bumping (gold plating) of semi-conductors.

The company generated about $200 million in EBITDA last year and has an Enterprise Value of about $430 million (their cash position is about the same as their debt) which makes the company cheap on an EV/EBITDA basis. While ChipMOS doesn’t look quite as good on an earnings basis (they earned 94c per share on a GAAP basis last year) that number will improve going forward as their depreciation expense declines significantly (depreciation was $157 million in 2012 but should be nil by the second half of 2013).

A key point with ChipMOS is that the stock trades at a significant discount to its competitors on the Taiwanese exchange. ChipBond, which is a close competitor, trades at a 50% premium on a earnings basis, and, according to one brokerage report, a 200% premium on other industry metrics.

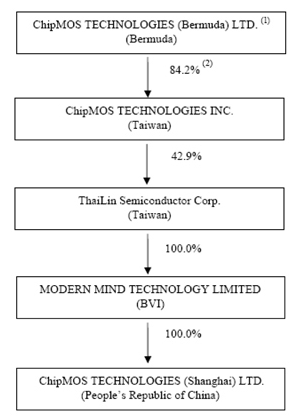

The primary reason for the premium seems to be nothing more than the Taiwanese exchange listing. The catalyst with ChipMOS is therefore a listing later this year for its Taiwanese subsidiary, of which ChipMOS owns 83%.

The first step in that process took place last week when the ChipMOS subsidiary was listed on the Taiwanese emerging markets exchange, which is a junior exchange. Stock quotes can be accessed on Bloomberg with the trading number 8150.

The stock opened with a bang. The original pricing on 8150 was $15tw. On the first day of trading the shares opened at $20tw and closed at $40tw. Since that time they have settled back to $33tw.

The $40tw price implies a value of $33USD for ChipMos shares on the NASDAQ. The current price of $33tw translates into a price of ~$27USD for ChipMos.

Presumably this gap will narrow. One of the reasons it has not is because the float on the subsidiary is quite small (ChipMOS did not release a large amount of shares for trading because of the low offer price. It was testing the waters), the volumes are tiny, which limits any arbitrage between the two companies, and its still not trading on the main Taiwanese exchange.

I jumped the gun when I bought into the run-up after the first day of trading of the Taiwanese sub. At the time I thought that the price of the sub would be enough to validate a higher price for the NASDAQ listed equity. That wasn’t the case. My spidey-senses seem to be a little off lately; I have been having a tendency of wrongly predicting the market reaction, both to the high and low side, of late. But that’s another story.

Nevertheless, the story remains intact, even if it will not be realized as quickly as I had hoped. I am going to hold my shares with the hope that the re-valuation occurs in the weeks and months ahead, as we come closer to a listing on the main Taiwanese exchange.