Drug Price Reform is Off the Table

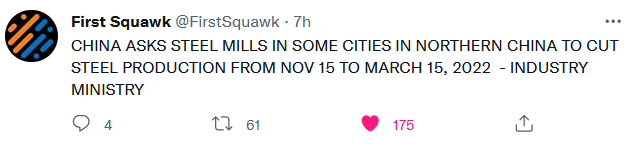

On Thursday morning before the market opened I saw this tweet come out from one of the biotech folks that I follow.

This was followed up by at least one analyst turning more constructive on biotechs:

One of the stories I remember from Reminiscences of a Stock Operator (the book) is that when the San Francisco earthquake hit, the market took a while to react because it was in a bull market.

Momentum is a strong force and the example here was that even the obvious devastation of an earthquake could not immediately topple the market.

Well, biotech stocks are in anything but a bull market. And momentum cuts both ways. The news came out and the market yawned. On Thursday you could have picked up many names at discounts to where their share price was just a few days before.

Nevertheless, in my opinion, this is very big news. My running thesis has been that the underlying “ask” behind the last 6 months of misery in biotech-land has been the specter of higher drug prices.

This article, written about a month and a half ago, put it starkly. It says that “Merck would cut its R&D efforts by nearly 50%” under the drug price reform proposal at the time.

If these sort of cuts came to pass, it would have had huge ramifications for all biotechs. Mergers and acquisitions would dry up. Money flow into the sector would slow. It is no wonder that biotechs have been down in the dumps.

So again, I think that this news, if it holds and isn’t more political gerrymandering, should be the bottom.

I bought biotechs on the news. But even I was not immune to the momentum. I bought some at the open, but not too much – just in case. Which really means, just in case biotechs keep on being biotechs.

The stocks I bought were not the same clinical stage spec companies that I’ve been playing with for the last year or so. This time I bought companies with approved drugs that generate revenue and cash.

A lot of these companies have been beaten up to 52-week lows. Even as the market has soared higher, they have not. Three of the four below are at a level that is roughly the same as their level at the height of the covid panic.

- I added one of the behemoths, Bristol-Myers Squibb (I came a hair away and should have added Abbvie though). BMY is a $130 billion company and trades at 7x next years earnings.

- I added Incyte Corp. They are a $14.8 billion company with $2 billion of cash and close to $3 billion of revenue. They are expected to grow 20% next year (they have grown at a ~20% CAGR the last 5 years) and trade at 10x next years EV/EBITDA.

- I added Vertex Pharmaceuticals, of which I am reading the book The Million Dollar Molecule right now. They are the leaders in cystic fibrosis, have a $48 billion market cap with $6 billion of cash, trade at 9.5x EV/EBITDA and are expected to grow 11% next year.

- I added PTC Therapeutics, which reported earnings just yesterday, beat revenue estimates and raised guidance, trades at ~6x sales (this is the only one of the list that is not profitable yet) and is expected to grow 35% next year.

If there are other cheap names with decent prospects, please email me!

In addition to these I already hold a bunch of clinical stage biotechs that I have held for some time.

I am fairly heavily biotech weighted. Which makes sense. It truly has been the pain-trade and I seem to gravitate to those.

We will see what next week brings. While it was a slow start on Thursday – I did notice that by end of day Friday they were beginning to pick up steam.

Markets react slowly when an earthquake makes them change direction.

—–

PS: In one other bit of news that is worth mentioning but not a whole post, Vidler Water, which I wrote about back and June and have been quietly sitting on, announced the sale of some credits this week.

While this sale is not a sure thing yet (it is a small amount up front with the option for a larger amount to be purchased before year-end), it could be very important to the Vidler thesis.

My only real worry about Vidler, and the reason I kept my position not super big, was that they had a lot of water credits in the Harquahala Valley, Arizona. My concern was that I read something and talked to someone else who questioned whether those credits were really worth what Vidler was saying at the time (they said a little under $400/acre-ft).

Well this deal is pricing one batch of those credits at $400 and another at $450. So if a material amount of credits sells in this deal, it vindicates the pricing. Which alleviates my concern. So I did what I had to do when something like this happens. I doubled down on my position.