Wading into another Biotech: Eiger Biopharmaceuticals

As I have talked about on occasion, I am a newbie to biotechs. To help with my learning curve I rely on a number of biotech investing gurus . One of them is, Daniel Ward, and over the last few months I have gotten a couple of ideas from him. One of these is Eiger Biopharmaceuticals (EIGR).

What I like about Eiger is that they have five trials in mid-stage development and plenty of data readouts in the short term. So (in theory at least) they shouldn’t have been killed by any particular read out.

But that thesis hasn’t played out as I had hoped yet. The stock tanked a few weeks ago from $11 down to below $9. The collapse coincided with data presented at European Association for the Study of Liver (EASL) conference in April. The results were for phase 2 studies that were investigating how their drugs Lonafarnib and (to a lesser degree) PEG IFN Lambda were successful in targeting the Hepatitis Delta virus (HDV).

These aren’t the only programs that Eiger has in progress. In total there are 5 programs, targeting 5 indications with 4 different drugs. In addition to the two drugs targeting HDV, Eiger has a Post-Bariatric Hypoglycemia program, a pulmonary arterial hypertension program and a Lymphedema program. All of the programs are in Phase 2.

I’m not going to go into all the programs in this post (its long enough already). I’m going to focus on the Phase 2 results for Lonafarnib that were presented at EASL. For more detail on the other programs, there is a good presentations archived on their website from the BIO CEO conference that describes all the programs and gives some background into the HDV indication that I won’t get into here.

Eiger and HDV

So to recap, Eiger has two drugs targeting HDV: Lonafarnib, which they obtained from Merck, and PEG-IFN Lambda (Lambda), which came from Bristol Myers. Both of these drugs are in Phase 2 of development.

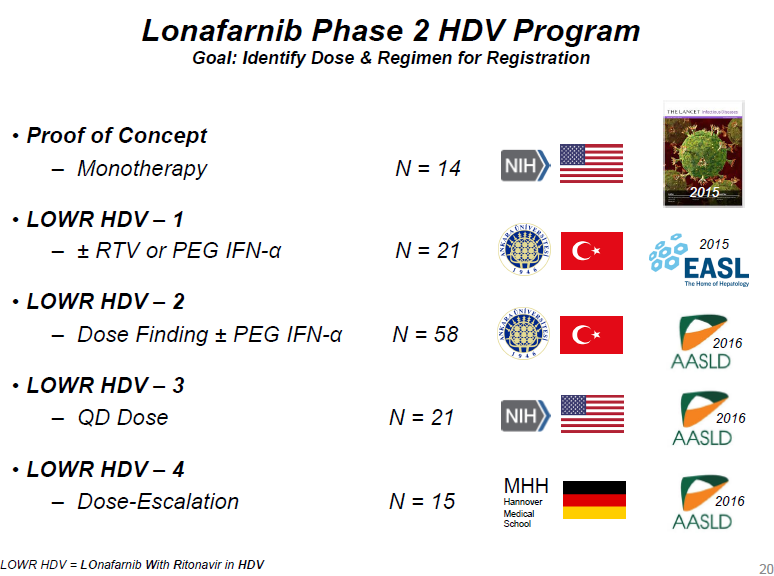

Three phase 2 studies were presented at EASL. LOWR HDV-2, 3, and 4 as listed below. The LOWR HDV-1 program had been completed and presented in 2015. LOWR-2 had already had early results presented in 2016. LOWR-3 and LOWR-4 were brand new data:

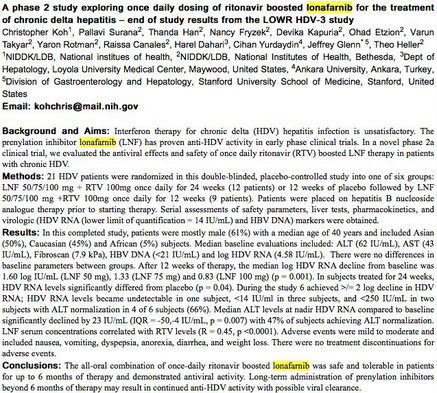

The LOWR-3 and LOWR-4 programs looked at different dosing options of Lonafarnib boosted by another drug called Ritonavir (Ritonavir is a drug used for HIV and you add it to the mix to improve efficacy). LOWR-2, which also looked at dosing, had an additional wing of the study where a number of patients trialed a 3 drug cohort that included PEG-IFN-Lambda in addition to Lonafarnib and Ritonavir. This was the only part of any of the studies tha looked at Lambda, which will have its own results presented later this year.

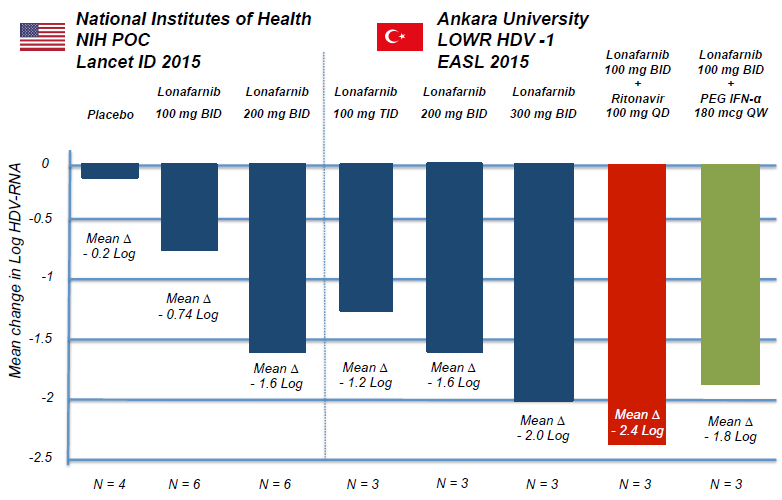

So what happened to make the stock tank on the results? First, they weren’t perceived to be as good as earlier data. The most apples to apples comparison that can be made is between the 100mg leg of the LOWR-3 program and the LOWR-1 program. Here are the results from the earlier LOWR-1 program after four weeks:

The LOWR-3 program gave 100mg of Lonafarnib and 100mg Ritonavir once daily for 12 weeks to 3 patients. So that should be comparable to the red bar above. The abstract from LOWR-3 is below. The relevant sentences are about 3-4 lines down in the results section (ignore the highlights, they are just artifacts of a word search I was doing).

The mean log decline for LOWR-3 at the 100mg dosage was 0.83 log IU/ml. This is quite a bit less than the red bar from the earlier program.

The LOWR-3 study was more comprehensive than just the 3 patients taking 100mg Lonafarnib for 12 weeks. There were also 3 patients at a 75mg dose and 3 others at 50mg that took the drug for 12 weeks (I’ll talk more about these in a second). In addition to this there were 12 more patients given the drug for 24 weeks (at the same dose increments of 50mg, 75mg, and 100mg). In the abstract it said that six of these 24 week patients saw greater than 2 log IU/ml decline in HDV RNA, so that’s good. But there was no mention of an average HDV RNA decline for all 12 patients, which seems an odd omission. It would be nice to see the entire paper to get all the data.

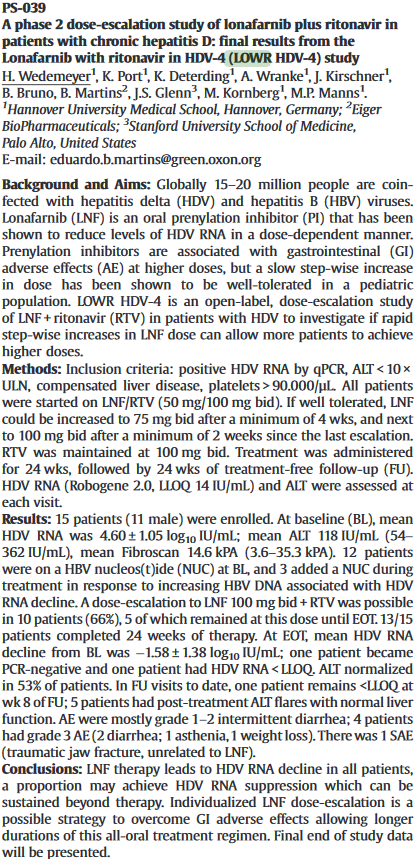

A second study, LOWR-4, looked at an increasing dosage. In this study 15 patients were given gradually increasing dosages of Lonafarnib. They started 50mg Lonafarnib, escalated to 75mg if tolerated and then to 100mg. They were also give 100mg of Ritonavir throughout, just like the other study. Below is the abstract.

The mean decline in HDV RNA for this study was 1.58 log IU/ml which, while below the 2.4 log IU/ml from the LOWR-1 study (remember again the red bars from above), is not too bad considering the dose was lower for some of the study.

Maybe the more interesting take-away from the LOWR-4 study was that the standard deviation of patients was +/- 1.38. I Maybe misunderstanding what that means but it seems like a lot of dispersion to me. I suspect it suggests that the drug performance has a large degree of variability in different patients.

So far what I’ve described is how Lonafarnib didn’t work as well as previous studies, but that it still worked pretty well. There was a definitive decline in HDV RNA levels, and it was well tolerated in all 3 studies, so there is no reason a patient couldn’t stay on the drug longer to presumably greater affect.

I think the final piece of the puzzle of why the stock went into a tail spin is evident when we look back at the 12 week dose comparison from the LOWR-3 study (the one I said I’d come back to). I briefly mentioned how in addition to the 100mg Lonafarnib arm there were other patients taking 75mg Lonafarnib and 50mg Lonafarnib along with Ritonavir. A comparison of the results of these different wings is surprising:

After 12 weeks of therapy, the median log HDV RNA decline from baseline was 1.60 log IU/mL (LNF 50 mg), 1.33 (LNF 75 mg) and 0.83 (LNF 100 mg) (p = 0.001)

According to the above, the lower dosed patients had a better response(?!?). This is odd to say the least. I don’t think the market liked that.

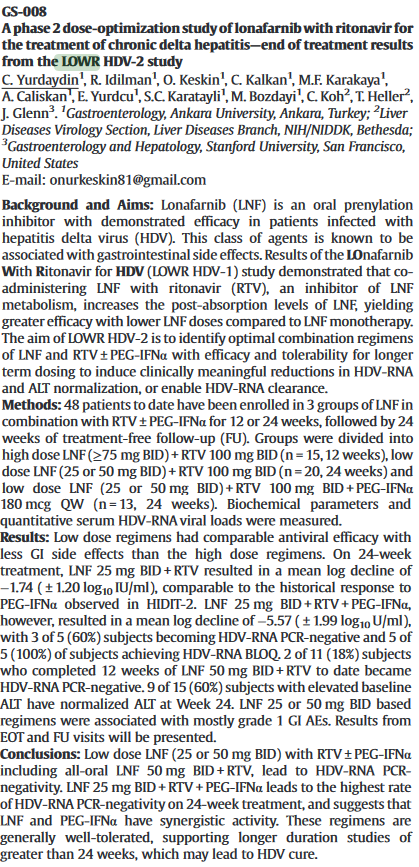

The LOWR-2 results also showed increasing the dosage had a murky impact on efficacy. I’ve pasted that abstract below. As I mentioned earlier, this is the second presentation of LOWR-2, as it was completed earlier than LOWR-3 and LOWR-4. There is a video of the earlier results that were presented here.

As the abstract describes, one arm of the study had 25mg Lonafarnib twice daily along with 100mg Ritonavir. Those patients saw a mean log decline of 1.74 log IU/ml (albeit for 24 weeks), quite a bit better than the higher dosed 12 week patients from the LOWR-3. I realize this comparison is not quite apples to apples, but again, it adds to the cloudy picture around efficacy and increased dosing. Indeed the study concluded that “low dose regimens had comparable antiviral efficacy with less GI side effects than the high dose regimens.”

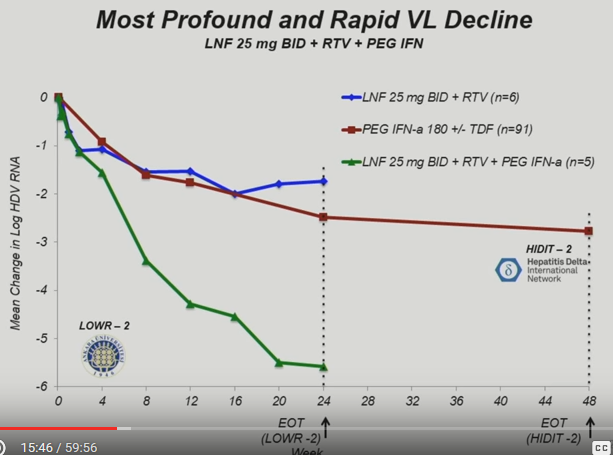

By far the best piece of news from the LOWR-2 study (and I think what the market is really overlooking) was the outsized effect of the arm that used Lonafarnib, Ritonavir and Lambda together. Repeating the relevant excerpt from the abstract (my underline):

[Lonafarnib] 25 mg BID + RTV + PEG-IFN alpha, however, resulted in a mean log decline of -5.57 ( ± 1.99 log10 U/ml), with 3 of 5 (60%) subjects becoming HDV-RNA PCR-negative and 5 of 5 (100%) of subjects achieving HDV-RNA BLOQ

In the conclusion the authors speculated at a cure:

NF 25 mg BID + RTV + PEG-IFN alpha leads to the highest rate of HDV-RNA PCR-negativity on 24-week treatment, and suggests that LNF and PEG-IFN lambda have synergistic activity. These regimens are generally well-tolerated, supporting longer duration studies of greater than 24 weeks, which may lead to HDV cure.

Note: In my original write-up I mistakenly equated PEG-IFN alpha with PEG-IFN Lambda. I didn’t pay enough attention to the Greek symbol being used. These are different drugs. Alpha was used in the 3-drug tests with Lonafarnib that I talk about here. But in future tests Lambda will be used. Lambda is the drug that Eiger owns. Eiger says that Lambda has similar downstream signaling pathways as Alpha and that because it targets a different receptor it is expected to have less side effects. But obviously this means there is a little more uncertainty than if Lambda had been used in the 3-drug trial. So my conclusions below are a little less pronounced.

To get a better sense of just how well the 3-drug cohort worked, I snipped this screenshot from the earlier presentation of the results. The 5 patient group taking Lambda in addition to Lonafarnib and Ritonavir is in green.

This seems quite promising.

What do I think of all of it?

Well for one I think it’s a great learning experience for me. I’m digging into data and trying to make sense of it, and at the end of this investment I’ll be able to look back and see what I got right and what I got wrong and hopefully learn a lot for the next time.

With respect to the HDV phase 2 results, I suspect that the stock has overreacted. I understand that the results are messy, but there is clearly efficacy here. Maybe the most important point to consider is that Lonafarnib is producing a large standard deviation and these are a small sample of results. So the noise is producing some inconsistent data.

Moreover, it seems very significant to me that the 3 drug combination that includes Lambda had such impressive results. With two drugs in development for HDV there are a number of ways Eiger can win here.

The other consideration that I haven’t focused on in this post is that this is only one of Eiger’s programs. As I mentioned earlier they also have a Lambda program, a Post-Bariatric Hypoglycemia program, a pulmonary arterial hypertension program and a Lymphedema program. Each of these are in Phase 2 and will have read-outs this year.

There are a lot of shots on goal here. And this is a $70 million market capitalization stock with $60 million of cash, so its not pricing in a lot of success. Again, I would recommend going back to their presentations to learn more about the other programs. I’ll probably talk more about each of them as new data comes out.