Week 82: Lots of Flux

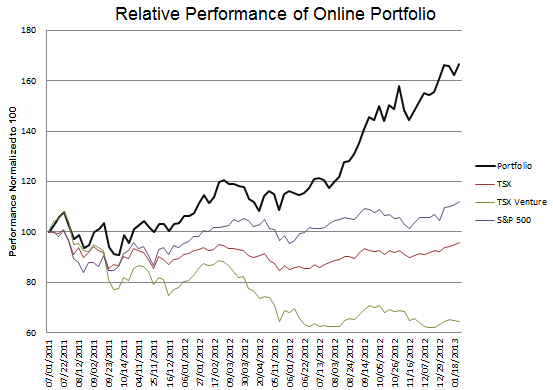

Portfolio Performance

Short Lived Niko Experience

I wrote about a new position in Niko in a short summary 3 weeks ago. A couple weeks later I sold the stock. What can I say – its part of my process. A lot of times I only get clarity about a stock once I own it. I buy a position, sit on it for a few days or a week, and do some more background and some more thinking on the name. With that my opinion becomes more clear.

The discomfort I developed with Niko was partially the result of another batch of less than stellar drilling results, but mostly the result of my conclusion that this isn’t the right time yet. The driver of the share price will be the settlement of a new gas price contract in India. I don’t think this is likely to occur until the existing contract expires, which is not until next year. In the mean time Niko will continue to experience production declines in India, and they are open to negative news flow on drilling. Read more