Peabody Energy and why it is very tricky to make a decision right now

It is very hard to know what to do with commodity stocks right now. For those that have held commodity stocks into the run-up (which could even mean “since Monday” given the incredible melt-up we have had), we are sitting on big gains.

Do you sell on those gains or are bigger gains to come?

In my last post I described some of the risks of holding commodity stocks right now. They are:

- Some sort of peace agreement

- The removal of Putin from power, one way or another

- Global recession

- Western countries outside of Europe getting fed-up with paying high prices and starting to view this as a “Europe problem”

All of these are on the table I think.

On the other hand, you have the reward of holding commodity stocks. Yes, they are up a lot, but how much higher could they go in a scenario where prices are higher for longer?

Let’s take the case of Peabody Energy.

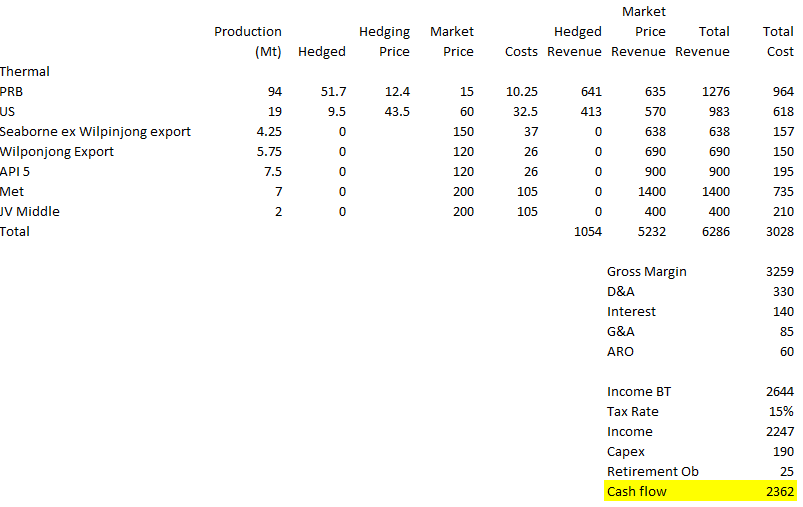

The great thing about looking at Peabody is they laid out their 2022 guidance in very understandable terms a few weeks ago. So it is very easy to model what their cash flow will be under different scenarios.

Peabody is, in a way, at the epi-centre of the crisis. Russia is the third largest thermal coal exporter. Russian coal accounts for roughly 30 per cent of European metallurgical coal imports and over 60 per cent of European thermal coal imports.

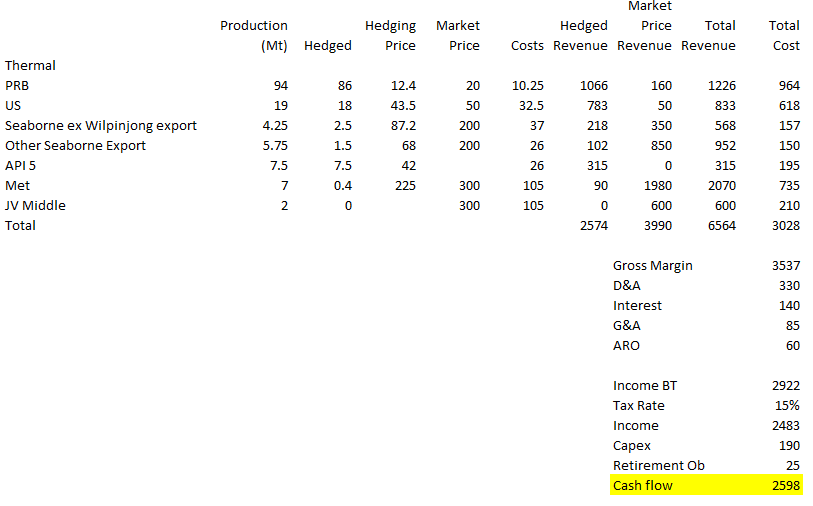

This guy put together a nice spreadsheet of Peabody. I’ve copied that below with a couple of changes.

The first scenario I’ve modeled is at $200 thermal and $365 met coal (Peabody receives a 15-20% discount on their met/pci coal). This is actually below current prices but well above the historical norms.

Peabody has a market cap of $3.3 billion and an enterprise value of $4.2 billion. So under this scenario, if these prices were realized for a full year, Peabody free cash flow would be roughly 80% of their market cap and 60% of enterprise value.

Now let’s look at the extreme. Right now, thermal coal is at $400. I don’t know what PRB coal is at, but the last time thermal was $400 PRB went to $30. What happens then?

While this scenario seems very unlikely over any long period of time, it could be approximate to what they earn in the very short-run. Peabody’s free cash is about $1 billion more than its current market cap.

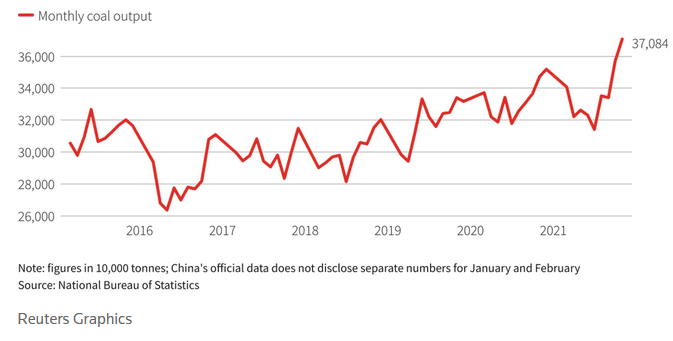

Russia supplied about 200 million tonnes of coal to the world last year. China produces 4.07 billion last year. China had to push their producers late-last year to get to that level. You can see that below:

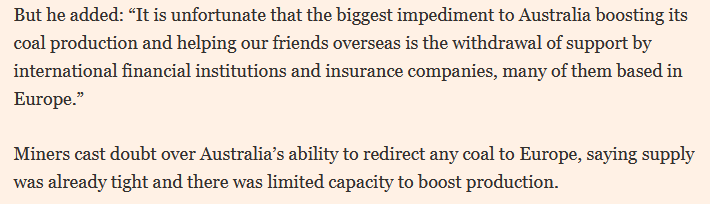

Australia is a big coal producer but this was their response a few days ago.

It is not entirely clear that the world can quickly make up any deficit.

That means the big questions are:

- How long will the spike last

- What is the new equilibrium if sanctions continue for a long period of time

The thing is, if there are still sanctions through 2023 much of the contracted coal that Peabody signed at lower prices is no longer under contract. The PRB coal, for example, is only 55% committed for 2023. It is pretty easy to see how even at much-reduced prices (from current levels), but still very high historic prices, 2023 would set up as another huge cash flow year for Peabody.

Are these the right prices for that scenario? I don’t know. But this is a scenario where we are in a conflict through 2023. If that is the case I know the prices are going to be higher than the 2021 prices. How much, its really hard to say.

Peabody is an easy example because they have given such detailed guidance. But working though similar scenarios with my other positions. Its the same result to varying degrees. For example, Cardinal, my biggest oil position, should do $400+ million of free cash at current prices. Cardinal’s market cap is $1.1 billion.

But… I am not actually trying to make the case to own Peabody or Cardinal or any other commodity stock here. FWIW I sold some of my position in Peabody (which I had added only on Monday) because it was up 40% in 5 days and I mean, holy cow, it feels irresponsible not to take some profits on that. I sold a little of Cardinal as well.

What I am trying to say is that it is really, really, really tricky to know what to do. It is truly about balancing the risk and reward based on your own individual circumstance and tolerance. Because Peabody could be a $50 stock in 6 months but it could also be a $15 stock in two weeks.

Outcomes to the upside and downside have suddenly become more extreme. That is why one of the only things I’m fairly certain of is you have to take down exposure to both.

World on tilt.