Tough Calls

I did not make very many changes to my portfolio last week. Yet it felt like a busy week because I did so much thinking about it.

It was a good week for thinking. Our family finally succumbed to COVID. My daughters had it during the week. My wife has it this weekend. I think I had it last week as well, I was ridiculously tired and headache-y, had weird neck and shoulder stiffness, had a worrisome (at the time) tingly feeling down my arms for a couple days, but I never tested positive, never had fever, never had a runny nose. So I don’t know.

Market-wise, there are so many things going on right now in so many directions. It is really tricky.

Let’s start with what we know. Biotech is going up. Finally. The question I am starting to ask is when do I sell some of these names? I think its a real balancing act.

On the one hand, I need to reduce my positions and take at least some profits. I have to, regardless of what my suspicions are about where we are going (I kinda think biotech goes higher). But I have to because I just don’t know. No one knows. Biotechs could flip and go back down for any number of reasons.

But at the same time, I did not go through that miserable biotech winter just to sell out for a 20% gain. Many of these stocks are up a lot from the lows. But they are still a double away from where they began the year and in many cases a triple or more away from the high. Its the same business. Just a different market. And markets change.

So like I said, its a balance. I have to trim in places. Sell down a little when a stock really takes off. But I can’t bring myself to a wholesale liquidation, even though the gains this last week have been significant.

I did add one new biotech position this week. Cidara Therapeutics. Its a decent story with a story in a story so here it goes.

Cidara’s lead program is Rezafungin, which is an anti-fungal that treats Candidemia and invasive Candiasis.

These are usually hospital acquired infections. The patients get very sick and many of them die. There is an existing treatment, but its old and, with a mortality of 35%, it doesn’t work that well.

Rezafungin finished a Phase 3 trial with results published in December. They were good results. Good enough to file an NDA (new drug application) with the FDA, which they expect to happen shortly.

I don’t really remember who told me about Cidara. It was back in December and I do remember it was someone telling it to me via a Twitter DM. But that DM isn’t there any more so whoever it was must have left Twitter.

Anyway, at the time I passed because Cidara didn’t have a lot of cash, they weren’t a negative enterprise value (I was all about having more cash than market cap back then if you remember) and I didn’t really know how they were going to get the money to commercialize Rezafungin, which seemed like a hurdle.

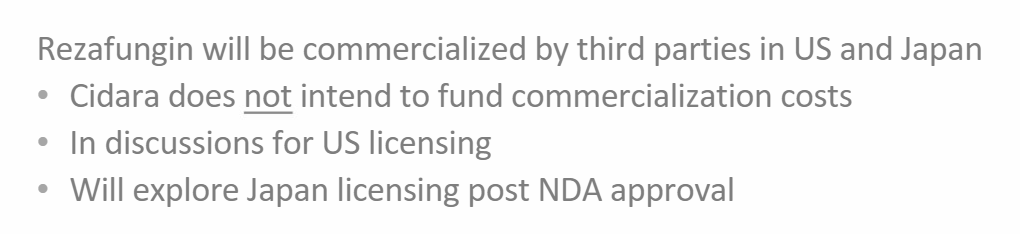

Flash forward to last week and I saw they did a Research and Development day. I went through their presentation, not really thinking much of it, when I saw this slide:

And that is like, Oh, well that’s interesting.

One thing I didn’t mention is that Rezafungin is already partnered for ROW ex-US and Japan. They had a partnership with a firm called mundipharma, which is where they got the cash to get this far:

So now Cidara is thinking that they will partner the rest of it. I listened to the Research Day call and they said they have had a lot of incoming interest in a partnership since the Ph3 results. Interesting. They say they think they will have something in place by the time they file the NDA. Interesting. They also say they will be filing the NDA shortly. Interesting.

But nothing here is a sure thing. I could get totally screwed on this by some sort of crummy financing that comes with the partnership. In fact, this is just what happened to me with another stock – Precision Biosciences – a few weeks ago.

Let me digress this story into another story that illustrates the caveat.

So I hold this other little biotech, Precision Biosciences. It’s kind of a crappy company. They do something like CRISPR but its probably not as good, the clinical results are promising but at the same time not promising, they do the same CAR-T stuff Caribou does and have the same problem with durability. And up until very recently the stock has been a complete disaster.

The stock was down at like a buck-20 a few weeks ago. It was finally trading less than cash. I was tempted, but I also didn’t know how they were going to make it as a going concern given the cash burn and the low cash levels. It seemed like they just might go bankrupt.

Then I saw this tweet.

So I was like, oh, that’s interesting. And I bought DTIL.

About 8 days later DTIL announces a partnership with Novartis. For sickle cell, because every gene editing company needs a sickle cell program. But whatevs, its cash, $75 million, and that will keep them afloat and put another program in their pocket and all those shorts betting the company is going to go bankrupt are going to have to cover.

The market realizes this and the stock SOARS in after hours. I mean SOARS! It goes from $1.30 to $3. I’m rich! (well, not really because I don’t own that much, but nevertheless, its a win).

But then, BUT THEN – half an hour later – half an hour – they announce a bought deal financing. AT $1.39!!!!!

What a mess. The stock comes right back down. It trades at $1.50-ish the next day, a far cry from $3. I still hold my shares and they are doing pretty well because of the biotech resurgence, but still, it was a total gong-show.

So back to Cidara. Its kinda the same situation. You have a cash strapped company that just hinted they may come up with a deal that gives them some cash. If they get that cash, the market will flip from ‘this company ain’t going to make it’ to ‘this company can live to fight another day’.

But like DTIL, Cidara also could decide to completely screw over their shareholders in the process.

Neverthless I took a small position in Cidara on Friday. Small because of all of the above reasons and also small because I don’t really understand the molecules they are pivoting too. Its something called their Cloudbreak platform, they are going after oncology, its a big switch. I need to dig into that to make sure there is actually something there.

So that’s biotech. Oh, and Eiger had news of sort. Something is happening. We don’t know what. But at least we have a date to work with.

Onto SaaS. I did lighten up a bit on the SaaS stocks I bought (OKTA, AYX, DDOG, CRWD and ZM, which I added more recently). They have had a nice move but I’m not sure how long it will last. They have a few headwinds.

First, interest rates aren’t exactly heading straight down and in many ways these stocks are little, micro interest rate bets. Rates go down, future earnings go up and the stocks with them.

I don’t know what to make of rates. On the one hand I get that a lot of this inflation should be transitory and the market is probably finally caring about it just at the time it should stop caring about it.

On the other hand, I’m not sure. And when I’m not sure, I don’t have to be long the stocks that express that idea.

Second, I can’t help but shake the feeling that this is a little like telecom in 2000. Back then, there were all these telecom companies that were booming and then all of a sudden they weren’t booming. It stopped on a dime largely because they were all booming on the backs of one another. Everybody was buying from everyone else.

I have a feeling some of that has been going on with SaaS. And I really wonder if some of this “secular growth” is going to turn out to be less secular then we thought because of it. So I don’t want to be too long and I may sell the rest this week before earnings start to hit.

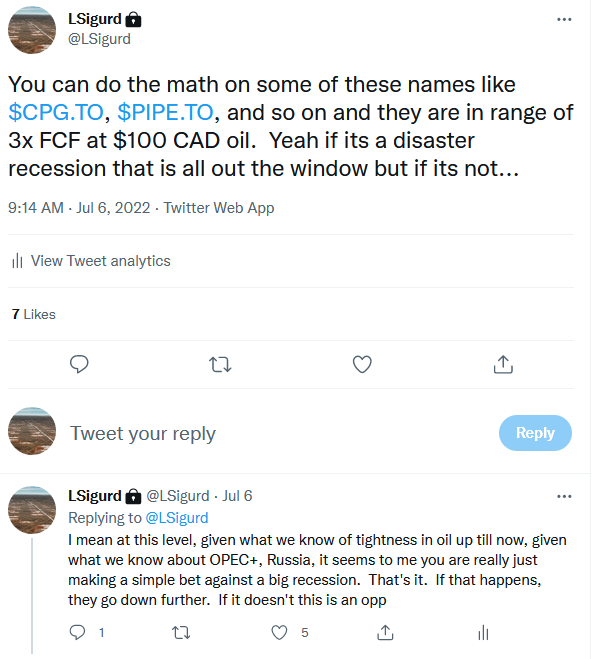

Finally oil and gas. I spent the first couple days last week frustrated that my oil stocks kept going down. So I kept buying them. Then I spent the last two days of the week selling what I bought as they came right back up again.

I made the case for owning some oil stocks in my last post. I tweeted that I thought it was getting a little silly on Wednesday.

Crescent Point had a nice pop the next day after they increased their dividend. So that’s great. But, I don’t want to be too long oil stocks here.

There is still this whole recession thing that seems quite plausible. And then there is Biden’s visit to Saudi Arabia. A good point was made on one of the Gulf Intelligence podcasts last week. I can’t remember which guest, but they pointed out that Biden would only be going to Saudi Arabia if he already has some sort of deal in the works. It would be too embarrassing otherwise.

I thought that made sense. I’m not sure exactly what Saudi Arabia can do, but they may be able to at least put on a show by making it look like they increasing production.

See the thing with Saudi Arabia is that they ALWAYS increase exports in the fall once their own domestic consumption (for air conditioning) begins to slow down. So that, and some releases from their strategic reserve and what-not could make for a big announcement and fan fare that makes it look like they are coming to the rescue. That makes me a bit nervous being too long oil here. I’ll keep my positions reasonably small.

Last, last thing. I put back on some of my index shorts again. I’m not unhedged any more. The market is well off the bottom now. It could verily easily keep going up. But I’m not really getting paid for heroics so I thought I’d feel better knowing that I’m not making a strictly one way bet.