Research: Datadog

I should be spending my time researching a stock I might buy or at least short. DDOG is neither. But I still find it super interesting to look at so I spent a bunch of time on it. I really didn’t look at everything. I got caught up on pricing, which I will explain, and spent a lot of time on it. I captured a few comments and such as highlights but I read way more in terms of opinion and perception of DDOGs product. These are my thoughts.

Here is the thing about DDOG. It is, by all accounts, a great product. You read the forums, it is best in class by most accounts.

But. A couple problems. First, this is not some revolutionary technology. What DDOG has is a monitoring tool. It really boils down to a GUI – a dashboard. Yes, there are all these tie-ins to data and sampling algorithms and a bunch of other functionality has been added to it as modules and blah, blah, blah. But its all basically – how can we allow IT folks to see what is going on in their network better. When you boil that down, the thing that everyone loves about DDOG is essentially a workflow and a GUI. That’s it.

Now it appears to be an extremely good workflow and GUI. No question there. But there is no magic here. Watch these videos. Go and search DDOG in youtube and watch the other customer videos. They make it pretty clear what the product does.

Meanwhile, as you will see below, DDOG is VERY expensive. IT guys are complaining about the price left and right. I point it out below. When I read the cost/host I thought it was ridiculous. I know how cheap IT guys are. They are always chintzy on spending money. There is a point where IT balks at 5-6-(7?) figure DDOG bills for monitoring. I certainly don’t think the TAM is what DDOG says it is if they are getting to a TAM by assuming every instance and host gets wired up to DDOG at current pricing. No way that happens.

The other thing about DDOG is this is niche. It appears to be a very large market because they can multiply hosts by ARR and get a massive number. But there are probably a handful or two of people in each company that actually need to look at this sort of monitoring data on a regular basis. Contrast that with a TEAM – they have a model where their TAM is the number of DEV/OPS multiplied by their sub price per user. Their users are all using the product every day. And the users are the entire DEV/OPS team. That is really different, if you ask me, than a TAM that is a far fewer number of IT admins that are actively deciding how much they want to spend to monitor their hosts.

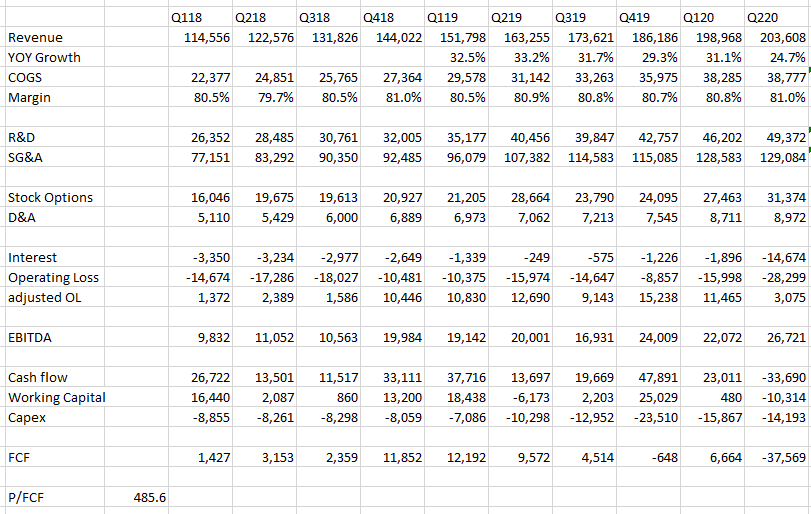

I just don’t think this lasts. At some point a smart IT admin is going to say – hey I can cut $50k out of my budget if I move from DDOG to this or that or just bring it in house. I think you see this already. DDOG customer growth is less than half their overall growth. So much of their growth is existing customers growing their instances of DDOG – or, if you believe some of the horror stories from reddit, getting gouged on pricing from unrealized monitoring that they are billed with.

Not surprisingly, NEWR reduced pricing and added a freemium layer. I’m sure they realize that DDOG has an Achilles heel in their pricing. I wouldn’t buy NEWR on that – it seems to me to have its own problems, but I also bet it starts making more IT guys ask – is this really worth it?

Of course to some it is. It sounds like a great product. Great graphs, easy to integrate, slick to use. But I don’t buy that a great experience is worth this kind of multiple. The moat here is way smaller than investors think it is, IMO and some of these competitors, or maybe some new start-up, is going to take advantage of that and start taking share at some point.

- founded in 2010

- 1,403 employees

- cloud native, SaaS platform addressing observability – monitoring cloud technologies

- offers “single pane of glass” view of IT cloud environments

- they break down silos between Dev and Ops

- their initial use case was infrastructure monitoring, from there expanded to APM and logging

- now added network monitoring, synthetics, security monitoring

Customers

- 12,100 customers as of Q220

- Had 8,800 customers as of Q219 – so customer growth was 37.5%

- Have 1,015 large customers, up from 594 yoy

- large customers are those with $100k or more – these are most of the revenue

- has net retention rates above 130%

- most customers adopt multiple products – 68% of customers have multiple products, up from 40% yoy

Product

- an event stream to see what has been going on in your environment

- so you tie in your hosts and integration by installing your agent into each

- then you create dashboards to see operations of each host and integration

- two types of dashboards – screenboards and timeboards

- can choose what hosts or integrations you want to show on the dashboard, what metrics, etc

- the graphs that you can create are quite detailed, very customizable, queryvalue maps, hostmaps. etc

- they have integrations to tie in a bunch of different

- functions – surface the relevant data you are collecting – transform the data with stuff like absolute value, log function, interpolation, divided by time

- notifications – get alerts – two types, desktop, emails, but also can add to snap, PD, ServiceNow, Zendesk

- can send notifications in a comment for any event in event stream

- use monitors to send notification when some metric is triggered

- collects metrics every 15s or so

- I’m surprised the TAM for this is so large?

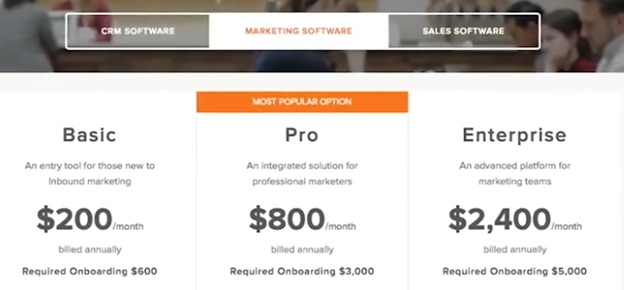

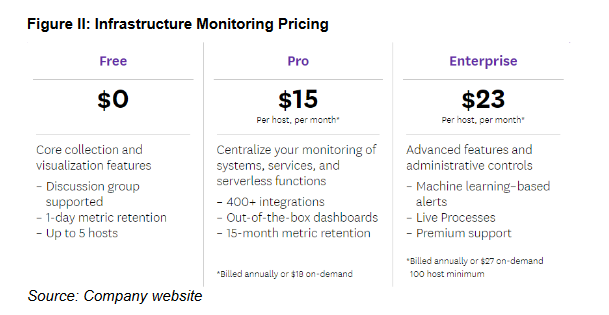

Pricing

- they have a freemium model, with a low end first tier

- model is on pay per host/application base – you pay for each instance that you monitor with DDOG

- it seems like they charge a lot:

- $23/host/month seems expensive

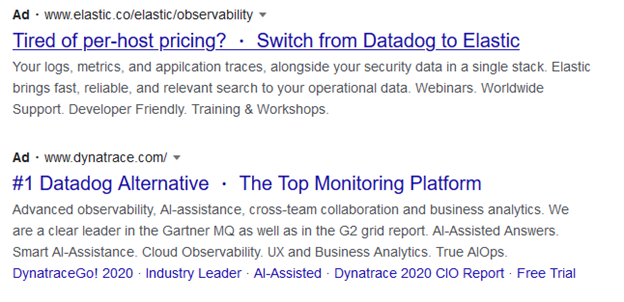

- when I type in “datadog expensive” into google these are the two ads I get:

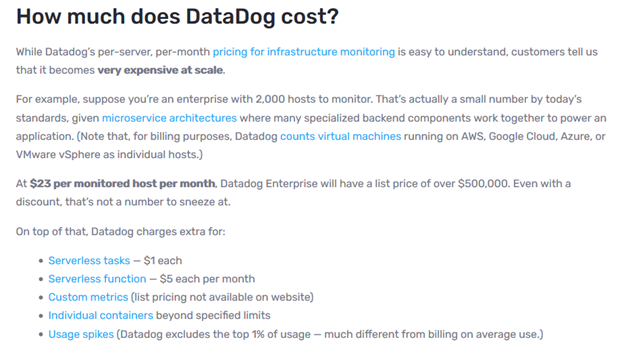

- another site making the point:

- their application performance monitoring is expensive as well: APM list pricing starts at $31/host/month and app analytics list pricing is for $1.70/million analyzed spans/month.

- Competition

- compete against Dynatrace, which has a cloud based service with similar functionality, and New Relic, which had an on-premise solution that they are offering now at a cheaper price

- NEWR is offering a free tier that they say would cost $10,000 with competitors

- but they changed tiers – reduced from 11 SKUs to 3 SKUs, results in some prices going up:

- NEWR is definitely decelerating – growth rate was only 15% last quarter

- DDOG has revenue retention in the 130% range

- this is an interesting take:

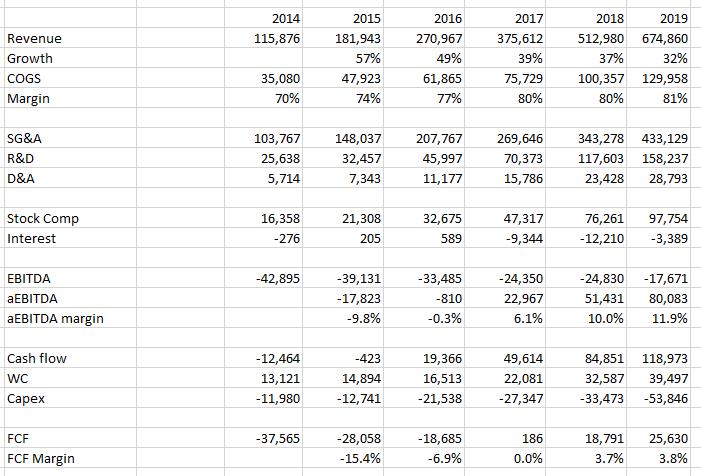

Despite all the buzz on Datadog, New Relic still has an entrenched presence in the infrastructure/application monitoring space as one of the original vendors, and though Datadog is gaining mindshare that doesn’t mean the space isn’t still new and greenfield enough for two big players By next fiscal year, Wall Street consensus expects both companies to be at a similar scale (~$750 million in annual revenues), but Datadog is now trading at >8x New Relic’s market cap. Despite New Relic’s lower growth, both New Relic and Datadog are cash flow positive

- NEWR has FCF margins of 14% – had $23.3mm of FCF in Q220

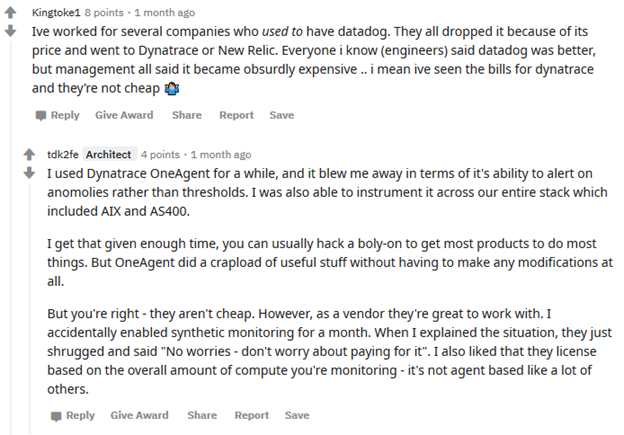

- from this reddit forum I get the sense that the Dynatrace solution is maybe as good or better than DDOG but it is expensive https://www.reddit.com/r/devops/comments/ige5jr/whats_your_preferred_cloud_application_monitoring/

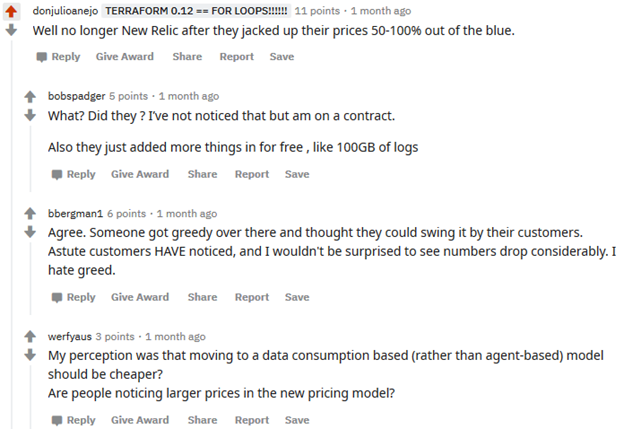

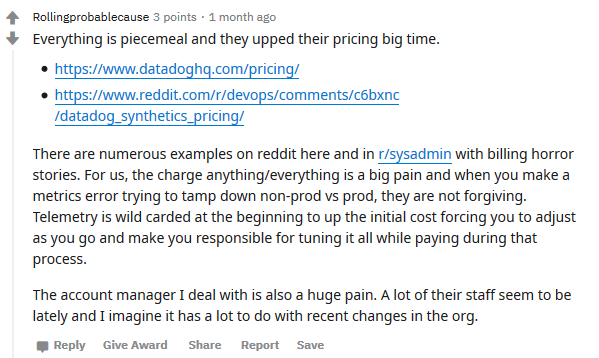

- here are comments on how DDOG is expensive:

- also Datadog has “shady pricing”:

- this is another good thread on it – DDOG is an extremely good product, but its also very expensive – https://www.reddit.com/r/devops/comments/i99zim/explain_datadogs_popularity_like_im_a_5_yo_a_5_yo/

- the problem is, their product is basically just a GUI with a bunch of hooks into other apps/hosts to sample data – this is not some crazy IP that can’t be replicated