Shoot First and Ask Questions Later

I’m starting to figure out why I am doing what I’m doing.

That may seem like an odd thing to say. But its true. I started to do things a month and a half ago and I didn’t really know why.

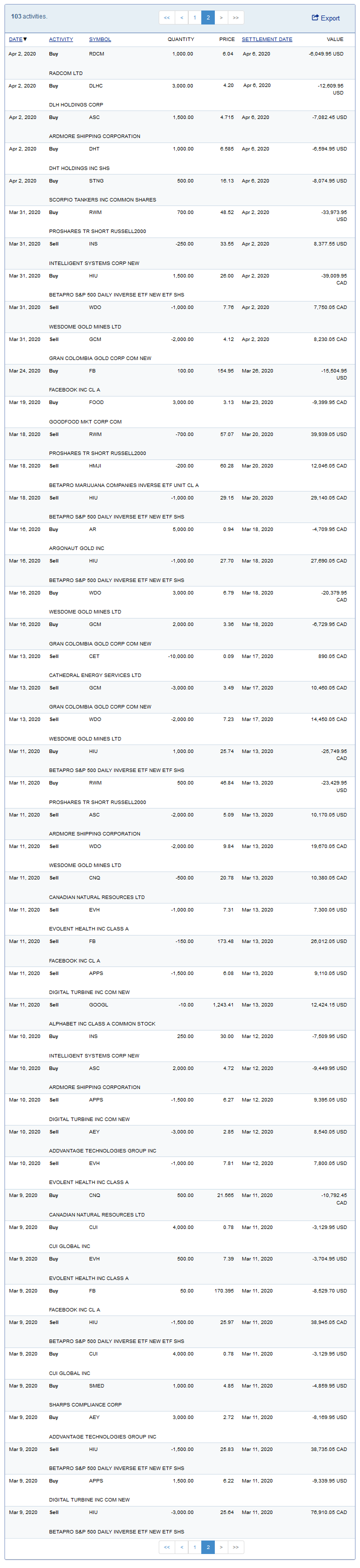

If you go back and look at my transactions and my last few posts you can kind of see it happening. I started, in the depth of the crisis, to buy gold stocks. Nothing too surprising so far – this was a pretty easy one for me. I know gold stocks well and I know the 2008 analog. They are the last one’s in, first one’s out. I thought that would happen again. So far it has.

Second thing I started doing was buying mortgage stocks. This may have seemed a bit foolhardy at the time, after all with the shit hitting the fan how many people are going to pay their mortgage? Fintwit told me these names were shit and they’d all go belly-up.

But again I knew these stocks pretty well, and from past performance I knew that the mark-to-market nature of their business, and because liquidity = solvency for most of these names – well that meant these stocks usually followed a pattern of taking a big hit up front and then doing better (even if they didn’t prosper) once the Fed was firmly at their back.

I’ve continued to add a few names to the list – buying Altisource Portfolio Solutions, Real Matters and even a little Ocwen a couple weeks ago.

Third thing I did was buy SaaS and technology stocks. Here is where things really went on tilt. I don’t buy SaaS stocks. But I’m buying SaaS stocks now. Hand over fist. I even bought LightSpeed POS (aptly named perhaps) last week, a stock I have shorted in the past!

Look, I wrote in my last post a few of the reasons why. I now have a better understanding of the margin compression of their growth model. The work-from-home environment is clearly a huge tailwind for most of the names. Low interest rates raise the present value of their earnings 5+ years out.

But even at the time, I was thinking there is more to this. I knew I was buying them for another reason, I just hadn’t figured out what it was.

Fourth thing I bought, well actually fourth and a little bit of fifth, is I bought natural gas stocks. I even added to that with an oil stock (for shame!), buying Whitecap last week.

But let’s stick to the natural gas stocks, because that is more on point here. I bought the natural gas stocks in part because I thought the oil shut-ins were going to drive down natural gas production, and that we might even be surprised by how the drop in light liquids pricing (C3+) would drive even more natural gas shut-ins in the more liquids rich basins (where the economics are really tied more to the liquids then the gas).

But I also bought these stocks for another reason – they were among the first to go up. There can be exceptions of course (and natgas could turn out to be one of them) but the stocks that rally first out of a crisis tend to do so for a reason. And these stocks rallied hard. They were like SaaS charts, which is saying something for a sector that has been shit for 5+ years.

Fifth, I’ve made bets on a few small, biotech names. Stocks that were whacked by the virus but shouldn’t be impacted much. I started with Eiger Pharmaceuticals a month ago (another former position that I know well). I’ve added a few more names on top of that the last couple weeks including Dare Bioscience and Immunic Inc.

Ok, so there are all my bets on the table. There are some other individual names I have bought, a stock like Rada Electronics, where it doesn’t really fit a thesis per se, I just think it is a stock that is going to do well. But mostly the stocks I own revolve around these themes.

But what’s the big theme here? What do these sectors all have in common? Why am I buying these things?

Here is what I’m starting to wrap my head around in the last couple of weeks. There is a lot of thoughts in my head about this, but I’m going to dumb it down to two basic points.

First, this virus has caused a huge hit to the economy. Massive unemployment all around. Many small businesses are going to close. That unemployment is probably going to be slow to come back because small businesses do most of the hiring. For a lot of people, its going to remain a tough go for a while.

The other side of the coin is we have this huge stimulus. This thing could be $10 trillion+ in the United States alone. And everyone gets free money. There was an article in the Globe and Mail a week ago that the Canadian Emergency Response Benefit (CERB) that gives $2,000 to everyone that lost some wages plus the 75% wage top-up to businesses have completely offset, in the aggregate the wages lost due to layoffs.

Think about that for a minute. In total there is the same amount of money out there now as there was before. It’s not necessarily in the same hands. some people are worse off for sure, but that means some are better off.

And that doesn’t count the money that isn’t going to people. There are the backstops of pretty much every asset market out there by Central Banks. They are buying government bonds, mortgage bonds, high yield bonds, its money for everyone and everything.

So you’ve got all this money out there and its basically compensating for the loss of money due to the virus. But – and here is where we have to go back to point 1 – that money can’t go back to all the usual spots.

In the real world a lot of sectors are still doing bad. Even as they improve as the lockdowns lift, they are still going to be sluggish until we get a vaccine. That means that this money, at least at the margins, is not going back to air travel, to restaurants, to hotels or airBNB, or to Uber. You can go down the list.

What I think this means is that one of two things can happen (or maybe a combination of both) – the money is going to go into savings (Robinhood?), or it is going to go into the parts of the economy that it can still go into – and those parts are going to boom.

In the investment world its the same dynamic. At the margins, the money isn’t going into mall REITs or office REITs. Its not going into airline stocks, restaurant stocks, or travel.

Instead, it is going to all get funneled into businesses that are at least doing okay – even better if it is a business that is doing great.

Like I have pointed out in my last couple of posts, we are (to my initial surprise) in an environment where there are some businesses that are doing okay. Some businesses are doing way better than okay. The shift in work, the shift in activities, and (depressingly) the hollowing out of small business is allowing larger, mostly publicly traded companies to take market share – and that means that some businesses, mainly larger, publicly traded businesses, are doing very well.

SaaS is the obvious example here. You can argue that this move in SaaS is getting a little stretched technically. Sure. But if there was ever a time that was ripe for a crazy sector specific bubble, this has to be it. And these businesses, they are doing well; they are raising estimates and those long runways of growth are getting pulled in as demand moves online faster. It makes me wonder if they may just be the vehicles for a real, honest to goodness, bubble. Remember that in the 2000 internet bubble the numbers never really made sense. But it still happened.

I am reminded of something I’ve heard from some very smart people – that the best case for the stock market is if the Central Banks are flooding the world with liquidity but the economy isn’t strong enough to accept it all. Because then all that money that needs to go somewhere goes into assets. The banks have to lend to someone.

Is that not the case that we have now? What’s more – this concentrated money flood scenario is even more concentrated today – because that money can’t even go into all the markets, it can only go into the pieces that are kind of, sort of, doing okay.

Look, I’m not married to this idea yet. If I was I would sell my short S&P hedge. I’m not quite ready to do that yet. But I have to admit, I am struggling to see the fatal flaw in the logic.

In the short run that is. The flaw in the long-run is this can’t end well. If this idea is right, then we end up with some sort of Nasdaq 5,000 or Nikkei 40,000 scenario before it is all said and done. Bubbles burst.

But we are a long way from that. And maybe this is totally wrong. Maybe insolvency will overwhelm the whole thing and send us back down.

But maybe not. There just may be too much money out there, with no where else to go.

{kind=link}

{kind=link}