Mauled to Exhaustion

Bear markets are exhausting.

For one, there is the whole losing money business. For two there is the increased difficulty of it all. For three, bear markets uncover truths that just make you tired.

In a bull market you can have a thesis and you can watch it play out. You can feel the exhilaration of being right as the market confirms what you knew (really suspected) all along.

In a bear market you realize that this is mostly hooey.

It is not that you can’t have a thesis or an idea. Bear markets are obviously great for the short-selling ideas. You can bet against a business and do wonderfully.

But even then, what underlies the win is the impermanence. Every short is just the broken thesis of a former long. While some longs may be scams that deserve to go down, most are not. A bull thesis that may have rightly been right for a month or a year or a decade now turns out to be terribly, terribly wrong.

So what was it? Right or wrong?

It is just circumstance. If circumstances had been different the perfect short may have been the perfect long, at least until those circumstances changed. Look at the group that has fought Tesla all these years.

The same goes for the bear market bear. You know your time is short. You know that your thesis is also built on sand that will harden fast if the business turns. A pivot, a return of dis-inflation, an acceleration of the business, a takeover, a sudden shift in strategy or even just a boat too heavy with other shorts, and all those arguments you have of why the stock should go down will be useless.

A bear market strips it all to the bone. It is just a game, with its own internal rules, and those rules are only loosely tied to daily workings of the companies at hand. If the rules were more closely tied to the business itself, stocks would never go up that much and not come down so much either.

The opportunity is just in the game and its rules.

Oh well.

We are a year and a half into this bear market, and I continue to mostly stand still. Had I just sat in cash for this time I would only be marginally worse off. In the accounts where I can’t short, I would be about the same. If you factor in the effort, the argument can be made that this would have been the better tact to take.

Where I can short, what is a bit frustrating is that, some 9 months in and 20% lower, I have actually been right about a lot of shorts, but that “right-ness” hasn’t been reflected as much I would have hoped in my overall portfolio performance.

Wondering how this happened, I took on the task of looking back. What I had shorted back in January, when the bear market was new and not really considered a bear market yet.

My shorts in January were inspired! Here they are: I went short Adobe at $515, Hubspot at $526, Cardyltics at $67, Salesforce at $218, Carvana at $157, Datadog at $144, Lightspeed at $40, BigCommerce at $33, Atlassian at $319, Fastly at $32, Open Lending at $19, OneSpan at $16, Daqo at $36, Tesla at $308 (split adjusted), Nvidia at $216, Sea at $128, Paycom at $312, Netflix at $400, Quantumscape at $21, Okta at $202, Silvergate at $137 and Amazon at $142 (split adjusted).

Quite honestly, on those names alone you would be hard-pressed to not assume I had shot the lights out this year. All of these stocks have been decimated.

Yet, I haven’t really shot the lights out. I’ve done okay, but not as well as it should have been given those names above.

<portfolio snapshot>

So why did my overall portfolio not kill it even when I had made a number of correct decisions like shorting all those stocks above?

That is really what I wanted to think about when I pulled up my short list from January. What exactly happened?

First, the obvious reason is that my longs did not do that well. Looking at January transactions, there are some pretty awful stock picks there. I went long Finance of America at $3, Precision Biosciences at $3.50, Smith Micro at $3.90, Checkpoint Therapeutics at $2.30. What in God’s name was I thinking! Yikes!

All these stocks were disasters that fell precipitously from where I bought them.

But this doesn’t really explain things in full, because in all of these cases I did not stick around for the collapse.

I sold all or part well before they could make too much dent in my portfolio. If there has been a savings grace for me in this bear market, it is that I have been quick to reconcile with my propensity to be wrong, and have taken action swiftly and without remorse.

But if I can only marginally blame my longs, what can I blame the rest for?

To get an understanding of what happened, I made a spreadsheet and ran the numbers and those January shorts alone.

If held all my January shorts until today instead of doing what I did with them, it would have contributed an extra 7.2% of positive performance.

While I did not run numbers on shorts I initiated for other months, I bet that in total my bypassed gains exceed 10%, maybe even 15%.

With most of these stocks I shorted I was quite confident they were going down. Yet all these gains were bypassed because I didn’t sit tight. Why?

Here is the crux of it I think:

Bear markets are a mauling. But not just for longs.

The mauling is far more general. Bear markets are made for a mauling of conviction. They are indifferent to whether that conviction is bullish or bearish. All preconceived notions of what the future may hold must be exterminated.

The reality is that if I had stuck with all of these shorts from January until today, they would have added a lot of gains. But the path from A to B was fraught with temporary losses that proved too great for me to take.

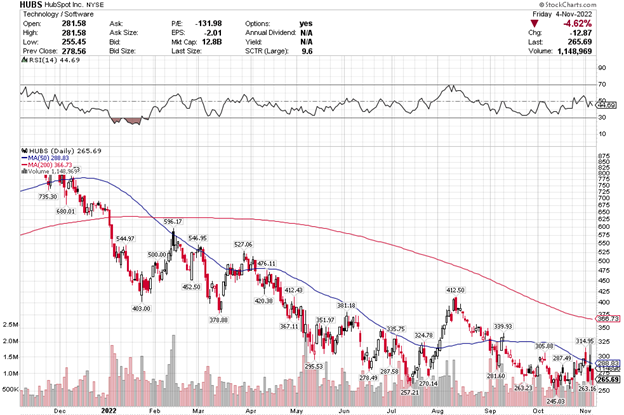

Let’s look at an example. Hubspot. I shorted Hubspot on January 6th at $526. I shorted again a few days later at $501.

Hubspot is a great example because it was such an overvalued POS in January. I mean, my goodness, it is just software. I was quite convinced in January that HUBS just had to go down. It was extremely overvalued on any metric, it was not really making any money, it spent gobs on stock-based comp that concealed real wage expense and from what I could tell it was not even all that great of a platform.

And in fact, HUBS has gone down. The stock price is $265 today. Had I just sat and held that HUBS short, for every $1,000 I had shorted I would have made $500.

Sounds easy. But here is the trajectory of HUBS.

It is the path where it gets tricky.

Holding that short would have meant watching all my gains wiped away in an early February rally, watching all my gains again wiped away in a March rally, and then, after finally making a killing down to the July lows I would have had to endure a move back to $412 in mid-August, wiping out more than half the gains one last time.

This is not an easy path. It is a mauling of conviction.

What did I do?

A couple of comments about my actions above.

First, I was clearly skittish about this position. I was worried it might not work. More than once I covered only to re-initiate the short in days at basically the same level. This for a stock that I truly despised and that seemed horribly mis-priced to me.

Second, once it got to $380 in June, I did not short HUBS again even as it fell to $265. Why? The answer is in that last cover.

If you squint really hard at the chart of HUBS, you will notice that on June 2nd HUBS got to $381.18. This marked the short-term high before another leg down.

I covered my HUBS for the last time at $380.82. That is 36c below the high.

I don’t remember the particulars of that day, but I think it is safe to say that I panic-covered at the top. I was so disgusted with this decision that I stayed away from the stock from there-on even as it began to fall anew.

If I add it all up, I captured 44% of the gains with HUBS that I might have captured if I had just held the short from January 6th until today. When I do the same for my January short book as a whole, it is a little under 50%.

To say it one way, the bear market mauled me out of more than half my winnings.

It brings to mind a well-known quote from the actual Reminiscences:

“After spending many years in Wall Street and after making and losing millions of dollars I want to tell you this: It never was my thinking that made the big money for me. It always was my sitting.”

But there is a catch here. It is hindsight. In March I did not know that Russia would invade Ukraine and set forth a cascade of events that would lead us to 8% inflation and 4% interest rates just 6 months later. I did not know the Fed would tighten to this degree.

Most importantly, I did not know that my portfolio would stop going down in mid-June and recover through the summer.

While as I said, I don’t remember the specifics of June 2nd, I will tell you the generalities of where my headspace was.

On June 2nd the S&P had just finished a rally back to 4,100. I had been caught more-short than I should have been into that rally. At the same time, some of what I was long – a number of the biotechs, Finance of America (my god to think I went back to the well twice here!), some of the regional bank stocks – had not done all that well even as the market rallied. I felt horribly offside.

So I did what I always do when I feel horribly offside. I sold. I reduced my longs across the board and I reduced my shorts. Including Hubspot.

I did not cover Hubspot because I thought the bottom was in. I covered because too many things were not working and so I had to get back to a place of neutral and re-evaluate.

You could argue it was a mistake. I mean, from a strictly HUBS-centric point of view it was a mistake. From the Reminiscences point of view, it was a mistake. Again, quoting from the book:

“Men who can both be right and sit tight are uncommon. I found it one of the hardest things to learn. But it is only after a stock operator has firmly grasped this that he can make big money.”

But now we come back to the “game”. The concept of a “mistake” is premised that there was some sort of goal that was not achieved in part because of that decision.

What is the goal here? Is it to be right? To be able to say I rode HUBS all the way down. To brag that I nailed a big short? Who am I saying this to?

This is not a movie. And no one really cares.

I’m past the point of trying to “make big money”. The only goal is to keep on keeping on. Remember that the fate of Livermore was not a good one.

I want to come out of this bear market in the best position possible for the next bull market. The only scorecard is the roof over our heads the meals on our table.

It is a game. The bear market makes that plain. But the bear market also makes plain that the essence of the game is that it is not a game at all. So know your rules and stick by them, or risk getting mauled.