Research: Apollo Health and Beauty

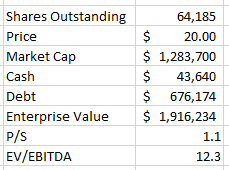

- 73.8mm shares outstanding at $2.78 for market cap of $205mm

- there are another 20.9mm warrants outstanding but they are way out of the money at $11

- they used to be called Acasta Enterprises – beginning July 2018 had operating sub called Apollo Health and Beauty

- amalgamated with Apollo Apr 2020 – changed name to Apollo…

- Apollo has been around since 1991

- employs 500 people

- one of largest private label personal care product manufacturers in NA

- develop and manufacture branded and private label products for retailers

- products sold across 10,000s of stores in NA

- was a breakeven business in 2019

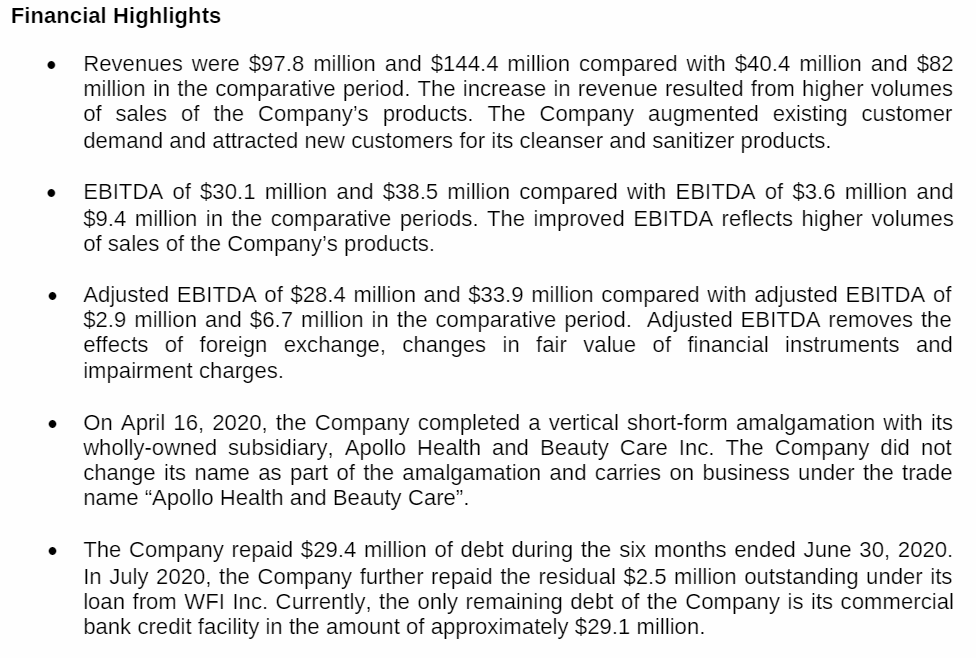

- I guess its their sanitizers and cleaners that are selling:

- they kind of allude to what is going on in Q220 MD&A: The Company attracted new customers and augmented existing customer demand for its cleanser and sanitizer products

- it is actually kinda surprising how little info or promotion of these results there are in the filings or PRs

Q2 Results

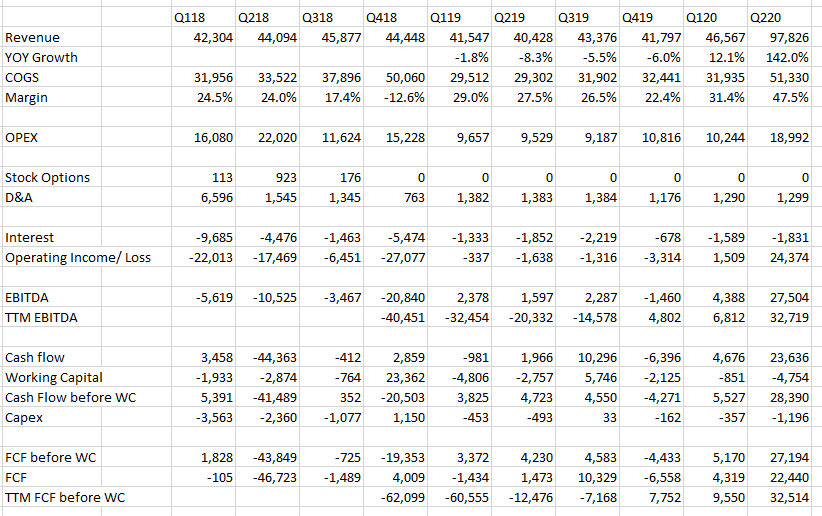

- debt at end of June was $35.7mm – they paid off about $29.4mm of debt in June

- EBITDA in June quarter was $30mm

- SG&A was quite a bit higher too though – up from $2.5mm to $7.9mm yoy in Q220

- also a pretty big increase in professional fees and general office expenses

- EPS in the Q220 was 35c

- it’s a pretty crazy increase in results:

Stan Bharti is chairman of the board (?!?) but he actually doesn’t own any shares according to circular, which seems odd

Stan Bharti is chairman of the board (?!?) but he actually doesn’t own any shares according to circular, which seems odd - run by Charles and Richard Wachsberg

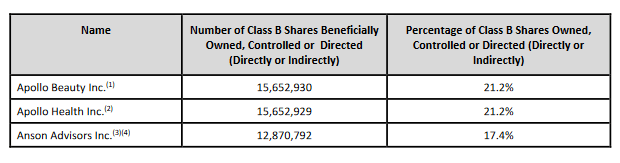

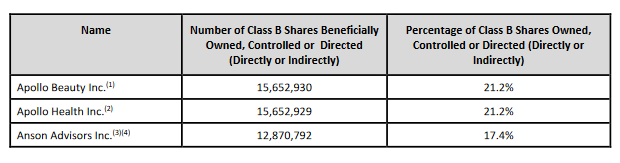

- these Wachsbergs own a lot of shares:

- another 2.5mm shares owned by Carlo LiVolsi, a director

- this does not seem like a scam or promo to me, just looks like they are in the right place at right time

- probably limited to COVID but really, should have pretty good results for a number of quarters, maybe 3-4 I’d guess, which would nearly would match the market cap

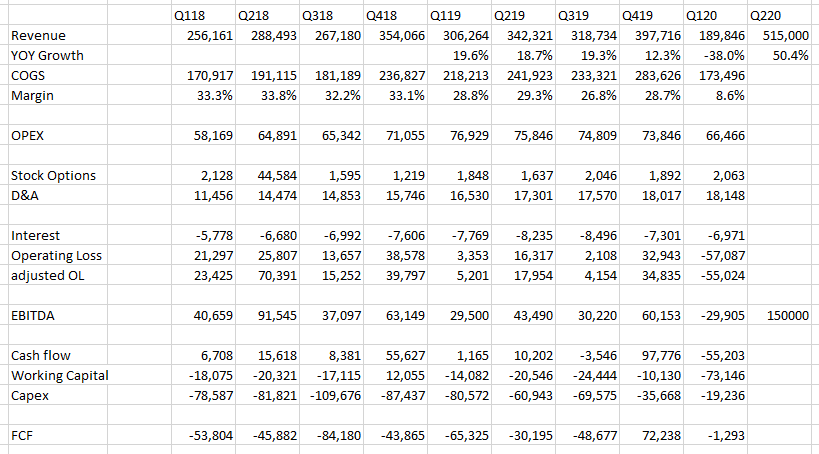

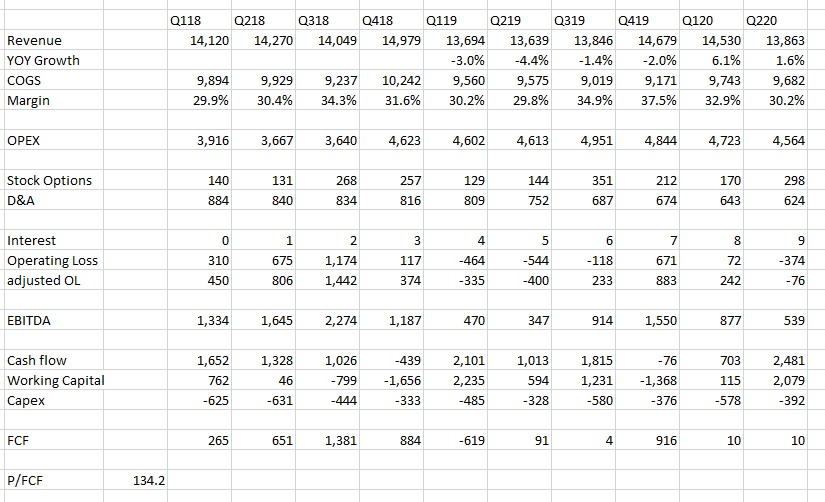

- revenue has been pretty consistent up until this quarter

- these are the last 10Qs of financials. They actually appear to have been turning the corner in Q1:

- it looks like they changed CEO and cleaned out the board a over a year and a half ago:

Acasta Enterprises Inc. (TSX:AEF) (“Acasta”) announces it has agreed with Charles Wachsberg and Richard Wachsberg, who together own approximately 36% of Acasta and are the co-founders of Apollo Health and Beauty Care (“Apollo”), to replace the Board of Directors (the “Board”).

The current Board and the Wachsbergs were not able to agree on strategy going forward and, accordingly, Geoff Beattie, Robert Schwartz and Jay Swartz have stepped down as Acasta directors and Ian Kidson has stepped down as Interim CEO and director.

Stan Bharti, Carlo LiVolsi, Jeffrey Spiegelman, Richard Wachsberg and Charles Wachsberg have joined the Board. The new Board has appointed the Wachsbergs as co-CEO’s of Acasta.