Week 163: Knowing when you are not at an advantage

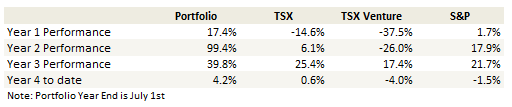

Portfolio Performance

See the end of the post for the current make up of my portfolio and the last four weeks of trades.

Recent Developments

Note that this update is as of Friday, August 15th. I have been a few days delinquent in getting it out.

I have strayed from my bread my butter of late, away from the tiny micro-caps that pass everyone else by and into the world of still small but not so obscure caps. These are stocks like Air Canada, AerCap and Bellatrix among others, still far from being large caps, but big enough to receive the attention of analysts and funds.

I am not so sure of my own advantage with these stocks. I may be overstepping my own abilities to think that I can see something here the market is not. I am under no misconceptions about my research. There is simply no way that I, as an individual investor with a couple of hours of free time every day, can match the depth and scope of the research that the institutions have. Read more