A Bit of Vindication

After a few tough weeks (in particular a CRISPR drawdown and the general biotech drawdown – which I bought into the way down – blah – was particularly grueling) I feel a bit vindicated these last couple of days. It was probably a good thing I have been away on vacation most of the time and not able to dwell on the ups and downs.

There were a couple of interesting bits of news last night.

Biorem

The first was news out from Biorem. I talked about Biorem way back in January. I have held my position since then and it has done basically nothing. Biorem released their second quarter results last week and those results were fine but did not hit the inflection I am hoping for.

Biorem’s backlog, however, remains very large ($30 million – which is over a year of revenue) and in their earnings release (no conference calls for this microcap) they stated ““Barring some unforeseen developments we expect a much stronger second half of the year as we deliver to projects delayed from the first half of year as well to projects originally scheduled for delivery in the second half of the year”.

The opportunity for the stock price to appreciate on such an improvement in their business increased markedly this morning. Biorem announced a share buyback. But not just any share buyback. A “60% of outstanding share” share buyback!

They are buying back 23 million shares from TPFG Environment Investment Limited for 52c. 23 million its a lot of shares! This is above the recent trading price of 45c but below where I was willing to buy shares back in January.

If the results in H2 are indeed better than H1, the purchase of these shares is a steal. There are now ~15 million shares outstanding. That means the stock has a market cap of $7.5mm. Yes the cash is gone, but it has been put to good use.

Derek Webb, who is CEO, and Doug Newman, CFO, have 400k shares and another 2.2mm in-the-money options between them.

Just as a reminder on what Biorem does:

While I can’t be sure of how the second half will materialize it feels to me like Biorem has improved the potential reward side of the equation by buying back so many shares. Consider that they did $2 million of earnings last year. With only 15 million shares, that would have been 13c EPS. On a stock that is 55c that seems decent.

Dixie Group

This is the second time in the last year that I have written about Dixie right after earnings. The first time was (briefly) last November. I owned the stock for a couple weeks then sold it for a bit of a gain.

Well I am at it again with Dixie. Ironically, I bought in this morning at pretty much the price I got out of it back then.

For some reason Dixie’s results of late make me think of Larry David – pretty, pretty, pretty, good. Kinda of that not quite believing, skeptical, wondering whether it will all blow up tomorrow kind of vibe.

But to Dixie’s credit they put together another good quarter.

Dixie has 15 million shares outstanding so a market cap of $45 million. They have about $75 million of debt.

In Q2 Dixie topped the $100 million mark in sales for the first time since Q2 of 2019. They had EPS of 22c per share.

The third quarter looks pretty, pretty, pretty good so far as well:

Our residential floor covering sales and orders for the first 5 weeks of the quarter have continued at a very strong pace, well ahead of the same period a year ago. Both residential sales and orders are approximately 30% ahead of sales and orders last year and 2019 as well.

Dixie is in the process of selling their commercial flooring business. Its a weak business (sales have been down since COVID) so I don’t know what they will get for it. It is also not the manufacturing facility – that is going to be used to expand the residential business. In Q1 commercial did $14 million vs. $21 million the year before. I won’t know Q2 until they come out with the 10-Q.

I’d hope they could fetch at least $25 million for the commercial business (though I have to admit, without the manufacturing I’m not sure what the rest is worth).

The bottom line with Dixie is that they just keep putting together surprisingly good quarters and the stock, while better than it was back in November, has a ways to go to reflect that.

Finally, Eiger Pharmaceuticals.

Honestly, last night I was planning to write a post on how stupid things had gotten with Eiger. The stock, which closed at $7.55, was trading at a market cap below $260 million with above $160 million in cash. A $100mm EV for a company with an approved product (Zokinvy) and two pretty good shots on goal at the $1 billion+ HDV market just seemed crazy to me. I never thought the stock would get this low again.

Well biotech woke up this morning and Eiger did with it. Its about time! Still, Eiger should be higher, if you ask me.

I last wrote about Eiger in November, when Zokinvy was approved. Zokinvy targets Progeria and processing-deficient progeroid laminopathies.

BTIG did a writeup on Zokinvy where they said Eiger would get $650k per year for each patient. There are 20 patients in the US, 23 in the EU and 180 patients identified worldwide (there is estimated to be 400 total but some of those I’m guessing are no identified yet?). I’m not 100% sure how Eiger collects on that steep $650k because in the US, where they are collecting revenue already, they say that none of these patients pay directly. They did about $3.5 million in revenue from the drug in Q1 but that included the initial inventory stocking.

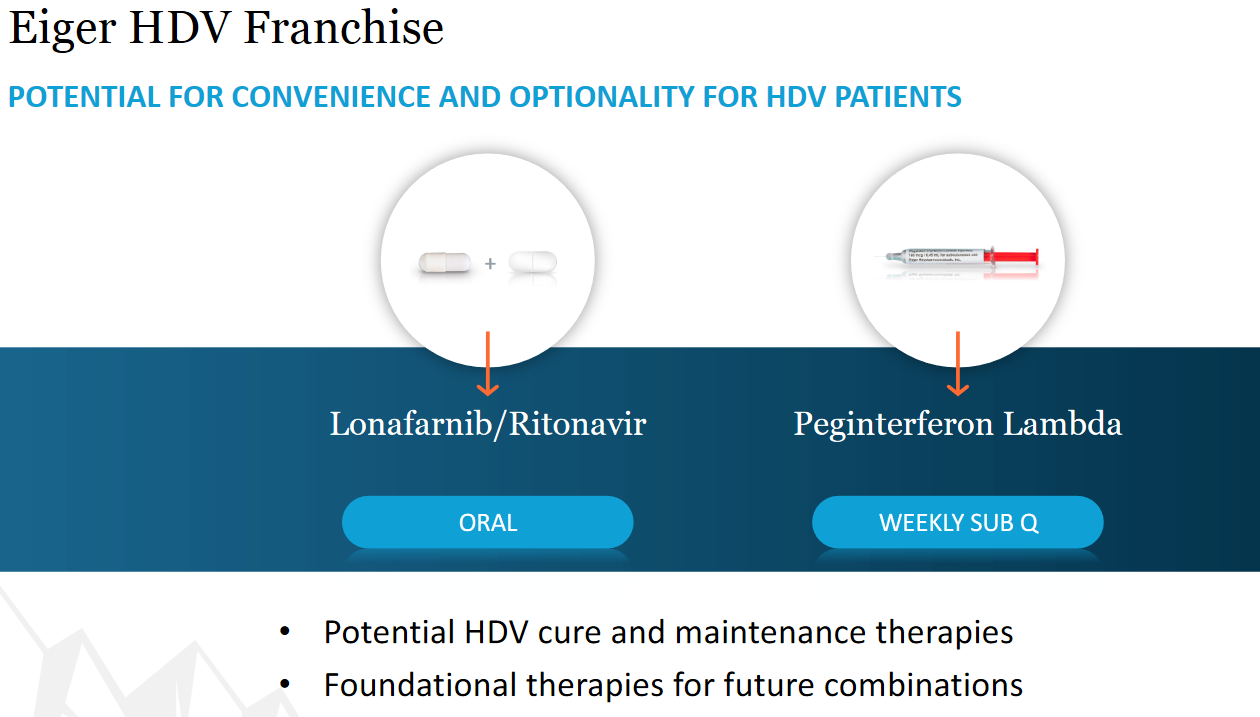

Eiger has two drugs targeting HDV.

At the Ladenburg Thalmann conference Eiger outlined the oportunity for these therapies:

So what does this mean for our commercial opportunity? Well, if you think about those 300,000 patients — roughly 100,000 in the US and 200,000 in Western Europe — and we’ve done considerable market research and benchmarking and believe that a treatment for HDV will cost $150,000 per patient, per year. And if you think about the number of patients then you would need to diagnose and actually get onto a treatment to create a $1 billion market opportunity, it’s 3%; it is roughly 3% in the US and 3% in Western Europe. So that’s less than 10,000 patients in total.

In other words, it is easily a $1b market.

Lonafarnab/Ritonavir is in Phase 3 and will complete enrollment this year. Lambda is just starting its Ph3 and will begin enrolling shortly (we should get an update on that with earnings tonight).

There is a wildcard too. Lambda is also working its way through a Ph3 study with COVID. Eiger had this to say about that at the TL conference.

Now Lambda is also currently in a Phase 3 trial, as I mentioned earlier, investigating newly diagnosed outpatient COVID-19. We generated positive Phase 2 results out of the ILIAD study in Toronto at Jordan Feld’s clinic, demonstrated a potential to improve clinical outcomes and curb community spread. Treatment was well tolerated. This is a single subcutaneous injection upon — literally upon diagnosis, and the patient goes home.

So we believe Lambda represents a potential true outpatient treatment versus monoclonals, which have to be intravenously infused. And even in patients who are vaccinated, the threat — as you may now be well aware, the threat of variance is a major concern.

Brazil is on fire with COVID. We were lucky to have the investigators in the TOGETHER trial come to us and request that Lambda be included as an arm. We have now dosed our first patients, and we look forward to updating on what could be a registration-enabling study for Lambda in COVID in Brazil.

Eiger kind of blew the opportunity with COVID early on because Lambda Ph2 data actually looked very good, but they were slow to get it out into trials. But with Delta, they get a second chance. If they report good data the stock could move on that alone. Consider HGEN, which is worth $950 million right now.

I think Eiger is getting thrown out with all the biotechs. Its just been a complete disaster in biotech land since March, and I am hopeful this rally puts it behind us. I think if it does Eiger should do very well.