This idea is bound to generate a lot of skepticism. Its the kind of wildly unprofitable, clever but challenging, just getting off its feet sort of business that a lot of readers are going to recoil at and probably tell me why it’s an inevitable zero.

And that’s okay because that is definitely a potential outcome here.

I got this idea from @teamonfuego on twitter so hat tip to him. I don’t think he owns it any more though.

Here’s the story

DropCar is actually two businesses. It is DropCar, which is a start-up valet and parking service, and it is WPCS International, which operates a communications infrastructure installation business.

These two businesses came together via a reverse merger. DropCar took a little under 85% of the capitalization while WPCS took 15%. The transaction closed at the end of January.

DropCar

DropCar is a fairly recent start-up. The company was formed in 2015. They operate exclusively in New York City. There are lots of articles available explaining the business and how the service works (here, here and here for starters).

DropCar offers a basic car garage alternative, a hourly chauffeur service, a premium service and a B2B service.

The basic service, which they call STEVE (they use people’s names for each of their offerings, I guess to mimic that its like a virtual valet or chauffeur), allows you to have your car parked at one of their garages, and when you need your car you arrange a pickup and a driver will bring it to your door. Similarly, you arrange a driver to meet you to take your car back to the garage. The service goes for $379 per month.

With the hourly service, the driver comes to your door but stays with the car through your travels and drives you around, eventually dropping you off and taking the car back to the garage. The cost of this service is $15 per hour.

The new premium service was launched in January. For a higher monthly fee ($499 per month), you get all the benefits of STEVE along with a maintenance and care program.

The B2B service arranges pick-ups of vehicles for maintenance by dealerships, fleet leasing centers or other auto-care facilities. DropCar has a reasonably sizable list of New York based dealers that have offered this service: Mercedes of Manhattan, Lexus of Manhattan, Jaguar, Land Rover of Manhattan, Porsche and Toyota.

DropCar is also trying to develop a critical mass of drivers wherby they can leverage their model to participate into the new “flat fee service” option being offered by dealerships. This is where consumers pay a subscription fee on a monthly basis. Its early, but it’s in the trial stage by by many dealerships (other articles here and here). DropCar would be like the delivery man for these services, picking up and dropping off cars and bringing them in for maintenance when required.

They are also looking to leverage the data they collect. They began to hint at in this recent excerpt of a January press release:

Not only does it harvest an increasingly valuable trove of big data (e.g. consumer auto-related data), but it proactively benefits from best-of-breed sources such as Google and Waze. Along these lines, DropCar management eventually plans to monetize its software/middleware platforms and big data harvests through licensing agreements.

Failed Model

DropCar is not the first to try this sort of business. They were preceded by Luxe and Valet Anywhere. These companies did not fare well.

Historically, companies such as Luxe, which closed operations in July 2017 and subsequently sold their technology to Volvo in September 2017, as well as Valet Anywhere, which closed operations in July 2016, have unsuccessfully tried to build similar on-demand service models.

DropCar differentiates itself from these failed attempts in a few respects. They say the mistakes of their predecessors was due to:

- use of expensive in-city garages

- parking-only focus

- low valet utilization rates tied to only servicing consumers (B2C)

DropCar is trying to correct these mistakes by arranging garage space at the edges of cities, providing higher margin services like the usage of the personal valet and the business to business solution (B2B) being offered to dealerships and fleet owners, and trying to integrate all the services at a scale where they can efficiently utilize their drivers.

I don’t believe that DropCar is primarily interested in the consumer business, though that is the easiest and therefore has been the first to ramp. I think the B2B business will eventually be the better opportunity. In the latest update the company said the following:

In anticipation of a substantial enterprise expansion, DropCar recently converted a large portion of its seasoned valets into field management roles. While this transition momentarily tempered valet-base expansion, it enables DropCar to efficiently absorb the anticipated demand surge in 2018 from Tier-One automotive OEMs, dealerships and concierge service subscribers.

Its also clear that this is going to work better in some cities then others. New York City is ideal. The company identified Los Angeles, San Francisco, Chicago, Dallas, Miami, Boston, Washington DC, and Philadelphia as US expansion destinations. Globally they see Beijing, Shanghai, Tokyo, Singapore, London, Paris and Rome as possible expansions. But I don’t expect the business to be able to scale like an Uber, because many cities aren’t big enough or are too sprawled out to make the service effective. Luckily the stock is cheap enough that it doesn’t have to.

Rising Revenue but no Profitability

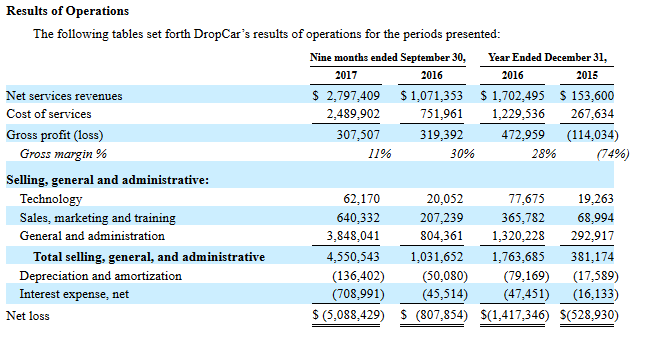

DropCar is growing, but they are not profitable. Below on the financials from the prospectus for the first 9 months of the last two fiscal years.

The company was actually closer to profitability in 2016 then in 2017. Gross margins have shrunk in 2017 and expenses, particularly G&A expenses, have risen.

You can spin the gross margin decline two ways. Either its evidence of a soon-to-be failed model, or it is evidence that they are ramping up for growth. I’m betting on the latter. Below is an excerpt from the prospectus (my highlight):

DropCar increased its valet workforce by 75 employees to 110 full time employees, or a 214% increase during the nine months ended September 30, 2017 as compared to September 30, 2016. This increase is based on increased demand in valet services, as well as anticipated growth in the next three to six months.

Similarly, the rise in G&A can be explained by expansion and costs associated with the reverse merger. About $850,000 of the year over year increase was attributed to payrolls, another $900,000 to merger related legal fees, $410,000 due to advertising and recruiting and $650,000 due to stock options.

Current Revenue Run-rate

According to a recent company update, the consumer subscriber base is currently more than 1,400, which is up from 500 at year end 2016 and 1,000 at the end of June. Automotive movements were also up significantly:

Overall consumer automotive movements exceeded 28,000 during the fourth quarter of 2017, up from approximately 10,700 in the fourth quarter of 2016. Quarterly enterprise movements have eclipsed 5,700 versus approximately 2,000 a year ago.

Based on the monthly rate of the base consumer business ($379 per month) and the current user count, the revenue run rate from the consumer business is $6.3 million. I’m not sure what the revenue is from the B2B business. The best I can do is extrapolate from their summer presentation. In it they said they had an overall $5 million revenue run rate from about 1,000 subscribers. This implies the B2B business was around $800,000 at the time. Assuming some growth to the B2B, I’m going to guess that the run rate of the entire business is about $7.5 million right now.

WPCS: Merger and Business

The reverse merger with WPCS International seems to have been initiated by a large holder of DropCar, Alpha Capital Anstalt. Presumably DropCar agreed to go public because of the access to capital, which they will undoubtedly need more of. I’m not sure why they decided to go the reverse merger route instead of an IPO. That is always something to be wary of and if anyone can shed light on this it would be appreciated.

WPCS has operated an unprofitable communications installation business for some time. They upgrade cabling and wireless infrastructure for institutions like hospitals, schools and government offices.

The business did $16.7 million of revenue in fiscal 2017 and $14.5 million in 2016. It consumed $1.3 million of cash flow in 2017 and $2.6 million in 2016.

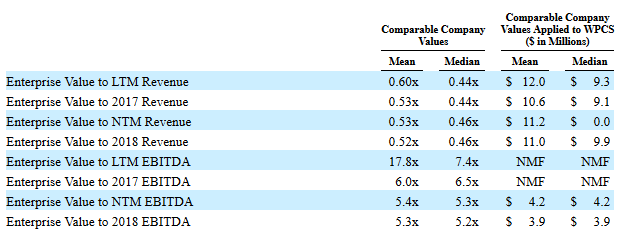

In a comparable company analysis performed as part of the merger agreement, Gordian found a fair value based on revenue of $10-$11 million and based on EBITDA of around $4 million.

This analysis was based on Argan, Ballantyne Strong, Dycom Industries, MYR Group, TESSCO Technologies, and Vicon Industries.

Alpha Capital Anstalt Forced Selling

Here’s what really got me digging into the idea.

Originally I bought some shares of DropCar when the stock spiked on Tuesday. I unfortunately bought into the spike at $3.15, and that was a mistake. I briefly looked like a genius as the stock rose to $3.50 but that quickly turned into a fool.

I wasn’t planning on buying more, but as I dug into what happened on Friday and then Tuesday, I came upon this disclosure from Alpha Capital Anstalt.

As part of the terms of the merger, DropCar needed to raise at least $4 million in capital. Alpha stepped up and provided the liquidity for the raise. However this took Alpha above their maximum allowable ownership, as this disclosure notes:

All of the foregoing securities issued to Alpha contain a 9.99% “blocker” provision designed to prevent Alpha from being a beneficial owner of more than 9.99% of the Issuer’s Common Stock.

I haven’t found it yet, but I bet they had something like a 30 day grace period before they had to get their stake down below 10%.

This is essentially what occurred on Friday the 16th, Tuesday the 20th and Wednesday the 21st. There were two 13-D forms (here and here) issued by Alpha where they disclosed that they had reduced ownership significantly, eventually down to 9.9%. In the second it was noted they were no longer in breach of the terms:

Does not include shares underlying the Series H-3 Convertible Preferred Stock nor the four classes of Warrants that Alpha Capital Anstalt (“Alpha”) can beneficially control under a contractually stipulated 9.99% ownership restriction. The full conversion and/or exercise of Alpha’s securities would exceed this restriction. Alpha’s ownership is now below 10%.

It is likely not a coincidence that the share dump by Alpha corresponded with high volumes and wild price swings in DropCar on the 16th, 20th and 21st:

In my opinion its unlikely that any of the prices we’ve seen since the closing of the merger agreement (January 31st) are particularly reliable indicators of the business’s value.

The stock began to tank from $4.50 down to $2.50 almost immediately after the merger closed. I think its possible that Alpha began selling as soon as they could, knowing that they had to get their stake down to below 10%. I think it’s also possible that other investors gamed the stock, knowing that Alpha was going to be a forced seller regardless of price. I did find reference to the disclosure about the blocker as early as February 5th, though there was more implied language of it much earlier in the prospectus, which was available back in December.

Who knows what really happened. Nevertheless it seems a reasonable bet it had little to do with the fundamentals.

Conclusions

Like many of the stocks I take a chance on, DropCar is no sure thing. There are failed precedents, they are losing money, and while the Alpha pre-merger capital raise brought in $4 million in cash, that is still likely only enough to get them through this year.

What I like about the stock is that the top line is growing and there is evidence it will grow further. In particular, the company is expecting a surge in the B2B business. From the recent company update (my highlight):

In anticipation of a substantial enterprise expansion, DropCar recently converted a large portion of its seasoned valets into field management roles. While this transition momentarily tempered valet-base expansion, it enables DropCar to efficiently absorb the anticipated demand surge in 2018 from Tier-One automotive OEMs, dealerships and concierge service subscribers.

Following the merger there are 7.8 million shares outstanding (from here). The market capitalization is around $20 million at the current price ($2.50). If I’m right about the current revenue run rate ($7.5 million) then the company is trading at a little over 2x DropCar’s current revenue run rate. Given the growth rate, that’s not particularly expensive.

As I pointed out above, the WPCS business could be worth anywhere from $4-$10 million in its own right. I would imagine that gets divested at some point to bring in more cash. There is also the $4 million of cash on the balance sheet,though this is going to get burned through this year.

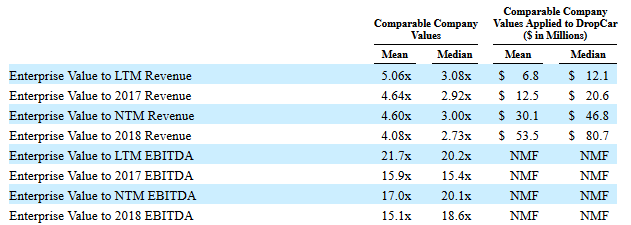

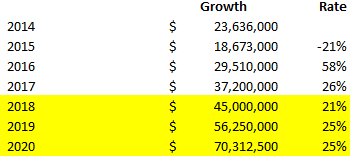

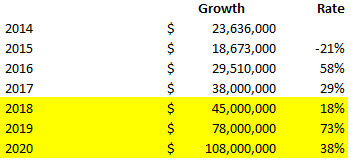

But here’s where it gets really interesting. In the merger prospectus Gordian performed a similar competitive valuation analysis for DropCar to what I showed earlier with WPCS. Here is the valuation table they came up with:

As you might expect, the valuations are quite different depending on whether you look backwards or forwards.

The forward numbers are pretty interesting. In particular I believe you can back out 2018 guidance from this analysis.

It looks like Gordian (presumably under DropCar’s advisement) is estimating 2018 revenue at more than $19 million, or more than triple current revenue and a 400% increase over 2017 (please refer to my note below, its really important to see how I got this number). I don’t usually bold things in these posts but that is a big number and I think its worthy of attention, both to consider and also to verify that I haven’t screwed something up.

(***Let me explain how I came up with my more than $19 million estimate. First, I think they have their mean and median columns mixed up in the table above. You can’t make sense of the numbers if the higher multiples are giving lower valuations. As well, the revenue numbers only line up if you switch the mean and median columns of the Comparable Company Values. For example, looking at the 2018 revenue line item, 80.7/4.08 is $19.77 million of revenue. Similarly, 53.5/2.73 is $19.6 million of revenue. So about the same, as you’d expect. But if you lined up the mean and median columns you’d get 53.5/4.08 and 80.7/2.73, in which case the revenues wouldn’t match up. Therefore I think the columns are flipped in the Comparable Company Values rows and that’s how I came up with the $19 million number.***)

Like I mentioned above, I don’t think the current price is necessarily reflecting anything other than the forced selling of Alpha. On top of that you have a stock that just went public via a reverse merger with a kinda crummy little communications business that nobody cared about. You have very few followers other than some day traders that are hitching themselves to the ride up and down and don’t really care about the business one way or the other. And you have a market capitalization that is tiny enough to be ignored by any fund. So there’s no interest in the stock yet.

If, and this is a big if, DropCar can get to the kind of revenue number that Gordian’s projections assume, that’s going to change. There is no way this should be a $20 million company if it can grow revenue like that. Its got to be WAY higher.

If they don’t grow revenue then it’s probably a zero. So that’s the risk and the reward. Its the kind of situation that is either going to crash and burn or go through the roof. Just the sort of option I like.