I bought SNAP this morning. I’m thinking this through and so this write-up is my “thinking this through thoughts”. I’m not 100% sold on the idea, but it makes some sense, enough to take a starter position. Here’s why.

First, this has nothing directly to do with the news of that the US government is set to hold a press conference on a “significant national security matter”. I was going to take a position in SNAP this week, I had made up my mind this weekend.

I’ve heard a couple of people on Twitter speculating that this might have to do with TikTok. Of course I have no idea if this is the case. But it wouldn’t surprise me.

Forbes had this article on Friday about TikTok planning to spy on US citizens.

While I don’t know if the announcement today will have anything to do with that, I just can’t see the US/EU letting TikTok sit on everyone’s phone given what is going on in China, especially if we see escalation now that Xi is ensconced in power.

Meanwhile SNAP had another shit quarter. That makes it 3 shit quarters in a row.

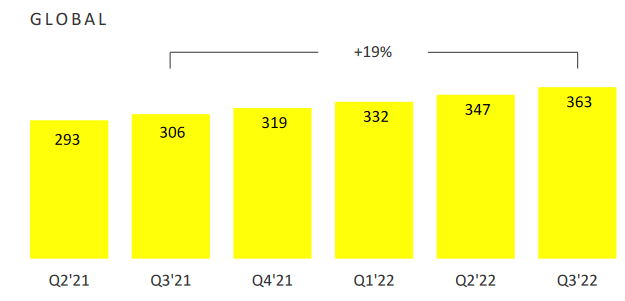

But here’s the thing. This isn’t some dying brand. SNAP saw MAU (monthly active users) grow 19% YoY.

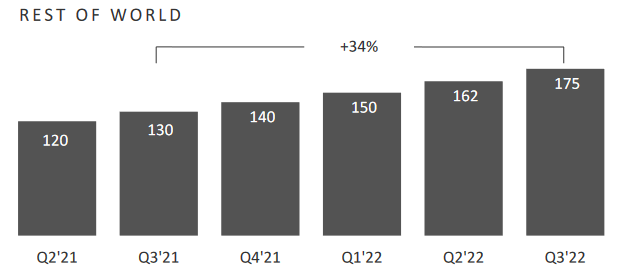

SNAP already has 100 million users in North America. So no surprise their growth there is slowing. But ROW growth is up 34% YoY.

This app is becoming more ubiquitous, not less.

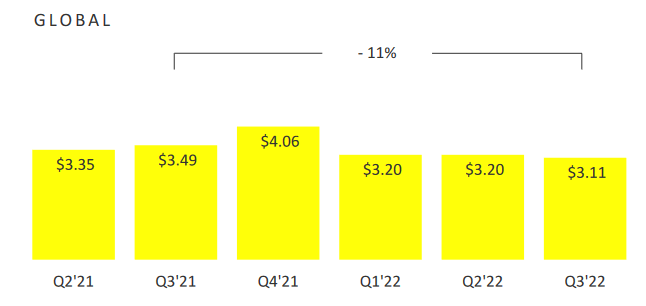

What hurts SNAP is that they aren’t making money off those users. Their ARPU (average revenue per user) in Q3 dropped considerably YoY and QoQ.

But you know, I don’t think that is all that surprising. First, ARPU in the US was only down 1%, while EU was down 5% and ROW was down 9%. So how much of this is currency? Second, SNAP is kinda being hit by the perfect storm of negative events.

SNAP ARPU in the US is close to on par with META average ARPU ($8-$9/MAU). In ROW though, SNAP only gets $1/MAU.

We’ve got the end of stay at home, so kids (especially high school and university kids) are probably not engaging as much. We’ve got the Apple IDFA changes – these were purportedly privacy changes Apple made that made it more difficult to get personal info from users and thus more difficult to target ads, and of course you have the TikTok phenom.

The back to school/work comps will pass. The IDFA stuff will also lap next year, and like these guys on the all-in podcast say (they also have a good discussion of some of the negatives at SNAP), Apple’s real goal here is not to protect our privacy but to build their own ad network, something they are doing and getting better at, which is going to help ad revenue. And TikTok – well we’ll see, but I honestly don’t get it. The US is stopping semi-conductor companies from working in China, it is blocking IP from going to China but it is going to let us give all our phone data to TikTok?

SNAP could obviously keep going down. If the trend holds the stock will do not much for the next 3 months and then drop 30% on the next earnings report. I kid… I hope.

At this price SNAP is a $12.5 billion company, which is down from being a $100b company a year ago. It is slightly cash flow positive, it has 360mm active users. You are paying $35 per user. When I look at other platforms like RBLX, META, SPOT, on a per user basis this seems roughly fairly priced to me. I don’t think SNAP is screaming cheap.

But I’m saying that on the “snapshot” of where we are now. I think there are a bunch of things that could go right from here.

I don’t know if I was the first to start talking about Silvergate Capital but I think I can say that I was ahead of most of the crowd. As is usually the case, I was also one of the first out the door and way too early. I bought Silvergate in September 2020 at $22 and sold it a few months later at $70. It seemed like a crazy win at the time.

But Silvergate just kept on going. The stock was over $200 at one point!!!

It was bizarre to me. This was still a bank after all. And the economics of their cryptocurrency on-boarding platform were okay, but they needed a lot of transactions to make their fees amount to enough to justify the stock price of $200.

Maybe most concerting was simply that this was a bank trading at 4x book value and banks don’t trade at 4x book. Could Silvergate really have found the secret sauce? One that other banks could not replicate?

Well… as it turns out Silvergate sauce is not quite as tasty as we originally thought.

The stock price is down a lot. We’re at $55 now. Below where I sold it two years ago. Trading at 1.4x Tangible Book Value (they were smart to raise capital when the stock was nose-bleed), a decent earnings multiple.

It seems worth a look.

First lets see what we have here. Silvergate is a $1.7b market cap bank. They trade at 11x PE on this year’s earnings, 6.7x on next year’s earnings.

Silvergate makes money from net interest on loans and securities they purchase less what they pay on deposits just like every other bank. What makes them unique are A. their deposits come from crypto players and B. they make money on fees related to their Silvergate Exchange Network, which is the crypto on-boarding platform.

This is all the same stuff they did two years ago. It is really no more or less amazing then it was then, when investors decided it was worth $200+ share.

First, some numbers and notes from their Q322:

EPS of $1.28

ROE was 1.04%, ROA was 13%

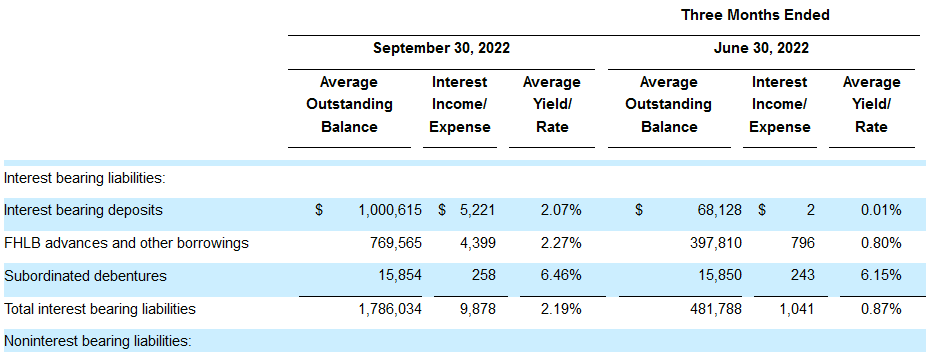

Their NIM was up from 1.96% to 2.31% – 36bps

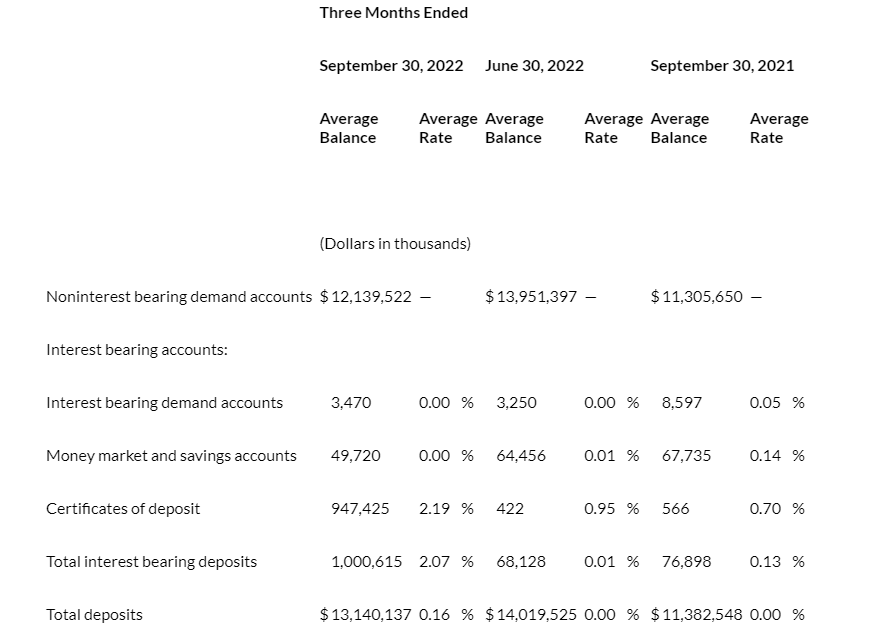

Cost of deposits rose from 0% to 0.16%

Book value is $36

Total deposits was down a touch – from $13.5b to $13.2b

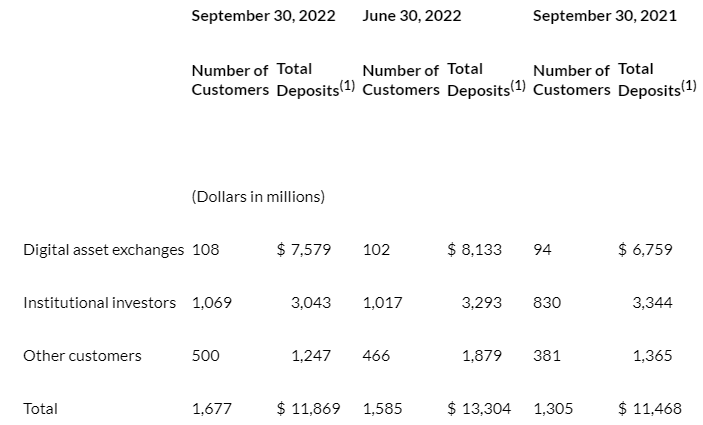

Digital Asset Customers: Q321: 1,305, Q222: 1,585, Q322: 1,677

Digital Asset Transfers down big: Q321: $162b, Q222: $191b, Q322: $113b

Overall net interest income was up $10mm to $84.7mm

Fee income was down from $8.8mm in Q22 to $7.95mm in Q322 – it was flattish YoY – $8.2mm in Q321

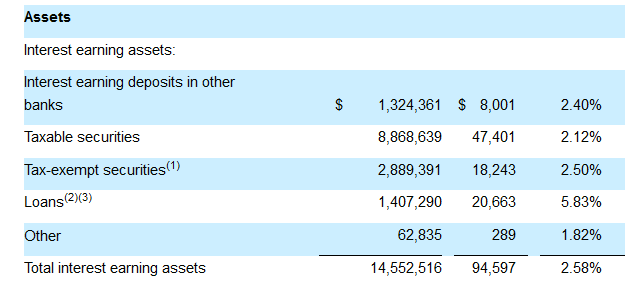

Interest margin on securities was up a lot: from 1.66% to 2.21%

They used more broker deposits and more FHLB advances

A couple of things stand out.

First, fee income. Its not up at all YoY. This was supposed to be a growth driver. I was not convinced. I was right to be skeptical.

It could be worse though. If you look at how much transactions were down, you might have expected fee income to be worse. I couldn’t really find anything that explained why fee income held up so well.

Second, digital asset transfers were down a lot in Q322. Digital asset transfers refers to their main fee business, which is moving money back and forth from crypto to US dollars. I didn’t realize it until reading the transcript today, but Silvergate’s biggest customers are stablecoins, USDC for example (they said back in May they don’t bank Tether).

Silvergate is “the regulated stablecoin transactional bank” – so when coin is minted or burned it goes through SEN.

USDC, like the rest of crypto, has been slumping in terms of market cap (not in valuation, since it is pegged to the dollar). There have been less USDC deposits at Silvergate. They said on the call that:

So, I think in the quarter between Q2 and Q3, we saw the total market value of USDC declined from $55 billion to $47 billion, which is about a decrease of 15%. Silvergate average deposits were down about 13% or so

So we know the deposits at Silvergate are tied to stablecoins. Yet if you look at the balance sheet, Silvergate has not seen a noticeable decline in its overall deposits. From my notes above “total deposits were down a touch – from $13.5b to $13.2b”.

How is that possible?

It turns out that while deposits did not decline, digital asset deposits did. Overall deposits only dropped $262mm. Digital asset deposits dropped $1.4b.

How did Silvergate make up for the difference? Using certificate of deposits (CDs), which skyrocketed to $1b.

That is no problem, except… CD’s carry a 2.07% rate on them, whereas the deposits they replace carry a 0% rate.

The result is that “the average rate on total interest bearing liabilities increased from 1.17% for the third quarter of 2021 to 2.19% for the third quarter of 2022, primarily due to the impact of increased interest rates on short-term borrowings”.

As you can see from the table below, those interest bearing deposits increased rather rapidly QoQ. If they keep increasing like this, they are going to squeeze net interest margin a little eventually.

But there are mitigating factors. Mainly, that Silvergate is not run by crazy crypto bulls. They are run by bankers doing banker things.

Silvergate is a bit funny for a bank because they don’t actually make very many loans. They only have about $1.4b of loans outstanding. Most of their assets are securities.

Silvergate is also very smart by only buying short-dated government securities. If you look at their security book, its almost all coming up in less than 12 months.

Here’s the thing about where Silvergate is at. If you look at the interest they collect, 2.58%, its only a smidge higher than their interest bearing liabilities – 2.19%. On the surface, this could be a big red flag.

But not as much as it might seem. For one, that is only considering interest bearing liabilities, and even though they are losing some non-interest bearing deposits, most are still non-interest bearing. For two, because they have prudently invested in very short dated government securities, they can reinvest at higher rates even as they need to pay higher rates for deposits.

And because there are so few loans, Silvergate doesn’t have to worry too much about default risk. They have no trouble with regulatory capital (their common equity tier 1 capital, a measure of how much capital they have to cover losses, is a rather ridiculously high 41%).

All this makes Silvergate a little uninteresting right now. They seem to be run pretty conservatively, so I don’t think anything is going to blow up here. On the other hand, because their main source of fee income is tied to crypto, it is hard to get excited about buying the stock.

They said themselves on their conference call that their business is based on Bitcoin and crypto volatility. Volatility brings on transactions and they get more fees the more the money moves. Until we get through this bear market I’m not sure we are going to see meaningful upticks in Bitcoin transactions.

The one other interesting thing of not is that they are planning a true dollar token:

We continue to balance our culture of innovation with our prudent risk-based approach to launching new products and are actively engaged with regulators and policymakers in anticipation of launching a regulatory compliant tokenized dollar on the blockchain. Unfortunately, we no longer expect that to happen this year.

The stablecoin they want to issue themselves is tied up with regulatory hurdles. But I can see why they want to have their own stablecoin.

The thing right now is that they don’t have stability in deposits. When transaction volume decreases, stablecoins don’t need to hold as much deposits with them. Silvergate said on the call that “we have always encouraged our customers to take their sort of excess deposits, if you will, or the deposits that they don’t need for issuance and redemption to other banks that do pay interest.”

So in bad times those deposits go away. That wouldn’t be the case if they had their own stablecoin.

You know, all this time everyone talked about how the risk to Silvergate was a big bank getting in the business. That they would eventually get squashed.

That may still be the case in the long-run. But it seems to me that the big risk right now is a long crypto-winter that pulls money out of the bank and eventually causes them to have to shrink.

It would be no spectacular blow up. It would be just slow dimming until the next Bitcoin bull market comes.

On Friday a lot of large banks reported earnings. I have read through pretty much all of those transcripts this weekend.

None of the comments I hear from the banks are particularly concerning.

Which brings me to the question I have? Do banks usually not see what is oncoming until it is too late? Maybe they are not leading or coincident indicators?

I see a lot of comments about a impending crash. There is the longer run recession issue, but the more immediate one is that all this tightening by central banks is going to break something. Yet I don’t really hear it in these transcripts. Could the banks be so blind?

I really don’t know what the answer to that is. But they really don’t seem to see much of a problem, at least some far.

PNC:

Credit quality largely unchanged, not seen any meaningful deterioration in credit

In regard to our view of the overall economy, we expect moderate growth in the fourth quarter, resulting in 1.8% GDP growth for the full year 2022

JPM:

“Things are roughly the same” as 3 months ago

Health of US consumer: nominal spending still strong… both discretionary and non-discretionary are fine

Combined debit/credit spend up 13% yoy

Spending is growing faster than income

Banking system itself is “extremely strong” with “lots of liquidity”

“credit trends strong across the portfolio…credit quality remains strong”

“the current credit environment is benign. In fact, our net charge-off ratio in the third quarter remain near historic lows, and we are not seeing any meaningful early-stage metrics that causes concern.”

“would not be surprised to see an economic slowdown develop at some point”

C:

“There is accumulating evidence of slowing global growth, and we now expect to experience rolling country level recession starting this quarter.”

“The U.S. economy, however, remains relatively resilient.”

“while we are seeing signs of economic slowing, consumers and corporates remain healthy as our very low net credit losses demonstrate, supply chain constraints are easing, the labor market remains strong.”

WFC:

“While we’re closely monitoring trends with economic conditions expected to weaken given inflation, geopolitical instability, energy price volatility and rising interest rates, our customers continue to be resilient with overall strong credit performance and solid cash flow”

“we continue to closely monitor activity by segment for signs of potential stress and for certain cohorts of customers”

“continued high inflation has kept the Federal Reserve aggressive with rate hikes, leading the housing market to slow rapidly and the heightened uncertainty about the economic outlook and geopolitical events caused the financial markets to be volatile. However, labor demand remains robust, consumer balance sheets remain healthy, and customers have capacity to borrow. Overall, our consumer deposit customers’ health indicators, including cash flow, payroll and overdraft trends, are still not showing elevated risk concerns”Overall, our consumer deposit customers’ health indicators, including cash flow, payroll and overdraft trends, are still not showing elevated risk concerns”

Out of curiosity, I went back and looked at the comments of banks during the summer of 2008 on their Q2 conference calls. A couple of takeaways. First, they didn’t see the complete collapse of the financial system that was about to occur in ~4 months. But… second, they did see something coming. All the talk was tightening lending standards, credit weakening, a pullback in spending, of course housing.

It was a very different tone than the Q3 calls so far.

While banks were not hinting at the calamity brought about by Lehman, they were seeing conditions that were clearly quite tenuous.

This is a very different tone than we have right now.

There used to be this podcast that I listened to that was a great podcast. It was called Reply All. It was all about the internet and how silly and beautiful it is. It unfortunately blew up because one of the hosts got “canceled”. He was canceled because behind the scenes he was mean to other employees of the show, which was not all that surprising, since what made Reply All great was how he was mean to other employees on the show.

But alas, it is an unfortunate tale of loss that is for another time. The relevance here is that Reply All used to do this segment where their boomer podcast company owner (Alex Blumberg) presented the millennial hosts with tweets he didn’t understand and the hosts had to figure out those tweets and explain them. That segment was called Yes, Yes, No.

At some point the boomer podcast owner decided he would flip the table around and do a different segment where he, a sports enthusiast, would present sports tweets that he understood to the non-sports-enthusiast podcast hosts and explain them to the hosts. This segment was called Sports, Sports, Sports.

And that brings us to today. My new segment is called Banks, Banks, Banks.

This is the second installment. My first was on Home Capital. I didn’t want to blast out an email on that one because HCG is always such a powder keg. If you want to view the post just send me a note.

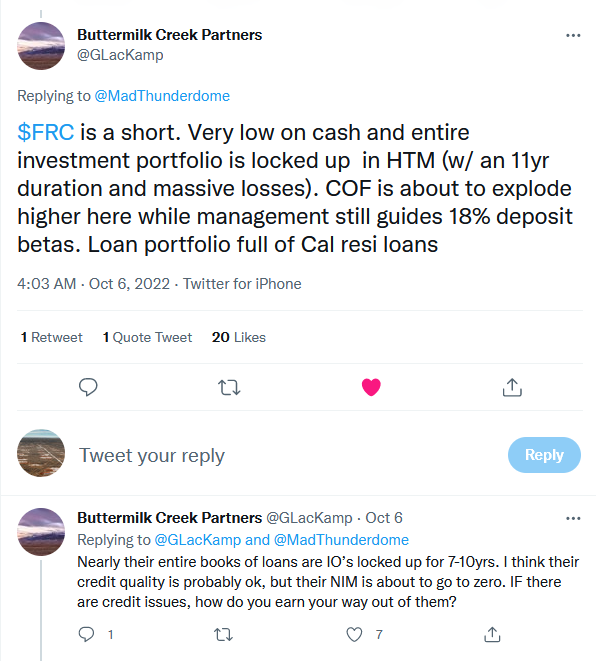

Today I will be discussing this tweet:

I found this tweet interesting because A. Buttermilk is advocating a short on a regional bank that had already been beaten up pretty darn bad and B. I didn’t know WTF he was talking about.

As it turns out, First Republic presents an interesting case. A whole pile of US banks reported on Friday (JPM, C, PNC, WFC, USB). Almost all of them had pretty good days, with most being up, which is an impressive feat considering the market as a whole was very much not up.

First Republic, however, did not do well.

Thankfully, I did not have a long position on FRC. I only sort of half-follow them. They are just one of the charts I have in my bank chart list, and I keep them there because they are a big, regional bank so I need to watch whats going on.

But then I saw the above tweet the other day, and I didn’t understand it. So I tried to figure it out.

I could spend a bunch of time going through what FRC is and does. But I won’t. Suffice to say that they are a California based bank, they pride themselves on their relationships with the households they lend to, they are known for having “pristine” credit quality, and they like to make mortgage loans. There is really not a lot going on here – its plain jane sort of stuff.

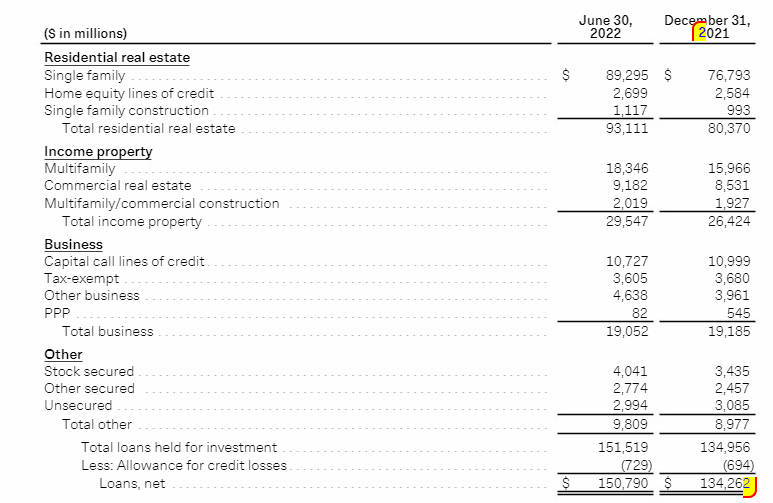

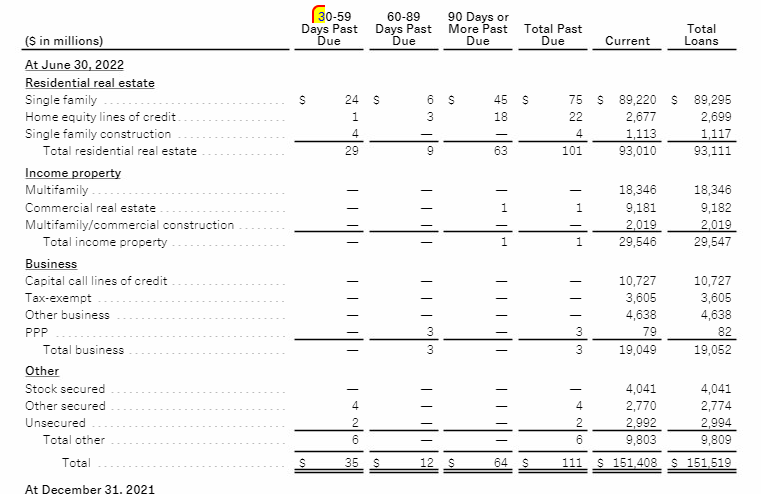

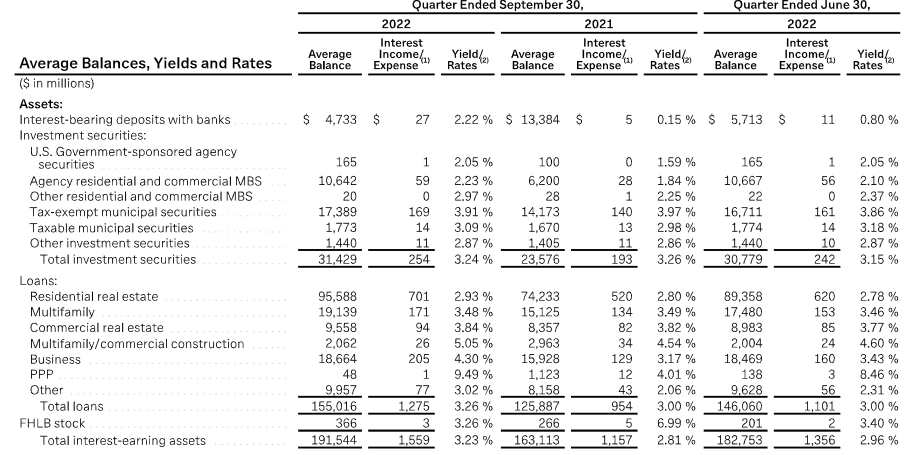

Anyway, this is First Republic’s loan book at a high level (I’m using the Q2 tables here because the 10Q wasn’t out when I looked at this but it is essentially the same for our purposes after Q3):

A couple of things about this loan book. First, its a lot of residential real estate loans. $93mm of $150mm in Q2. Second, though you can’t see it in the table, their balance sheet is pretty stuffed with loans. After Q3, they have $158b of loans and $172b of deposits. Compare that to a JP Morgan, where loans are ~50% of deposits.

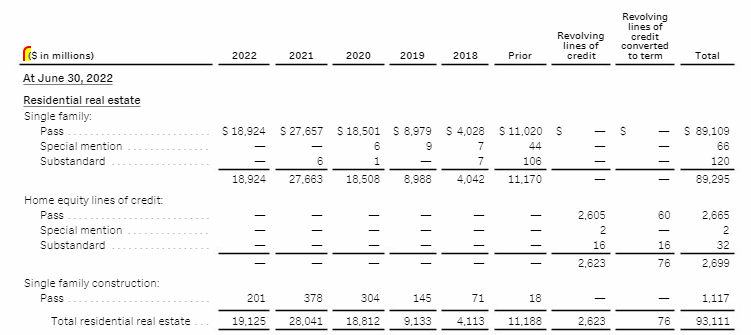

Like Buttermilk says, 52% of the single family home loans are in California. Take that for what its worth. More importantly, 60% of their single family home loans are interest only loans (I/O), with a very long interest only period – they amortize to maturity after 10 years.

I honestly didn’t even know interest only loans were still a big thing in the US. Who knew?

What’s more, most of these loans were made quite recently, in the last 4 years, meaning they are all still I/O and will be for a very long time:

Now, to First Republic’s credit, these loans are not going bad. Very little of their SF loan book is past due.

If you compare the past due loans at the end of Q3 to the number at year end, it is actually doing better now, so its not like there is some big looming default risk here.

Instead, the risk is more on what they are going to earn from these loans.

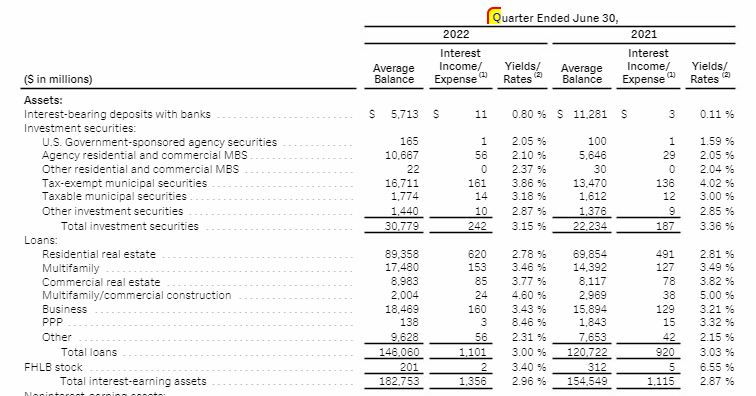

We know that interest rates have gone up a lot. Many banks are seeing their net interest margin increase in Q3. That is why the banks that reported on Friday all did well.

When I looked at this earlier this week I was looking at First Republic’s Q2 numbers. This is what I saw:

Their residential real estate loans were actually seeing a tiny decline in yield. Now that was a bit odd because I/O loans are usually adjusted rate mortgages, or ARMs. I looked it up. But I don’t think that is the case here. They must be making fixed rate loans, or at least loans that have some sort of lag attached.

Now they do say that 23% of their loans are adjustable rate or mature in 1 year. But they don’t tell us just how much of that is adjustable and I have to assume the 23% really is skewed to the <1 year maturity because rates didn’t budge YOY on any bucket in Q2 (and only moved marginally in Q3, as you will shortly see) and if there was a sizable amount of adjustable loans those rates should be moving.

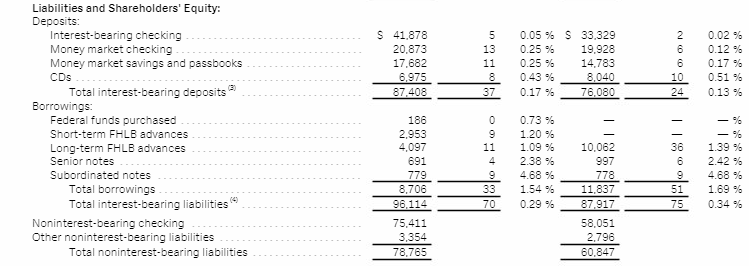

Nevertheless, in Q2 FRC was okay, because their deposit rates were quite low as well. They had hardly budged off a very low number (this is a Q2 10Q table).

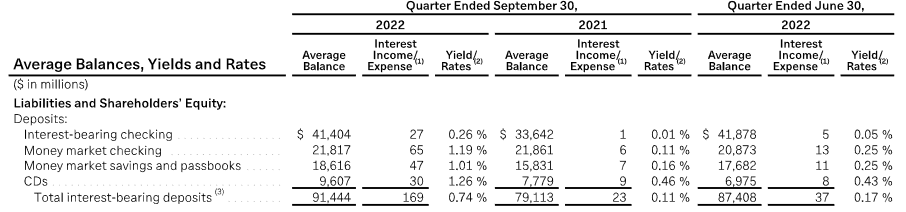

So everything was rosy. Cue the foreboding music. But, but , but… that changed in Q3. Some might call this an inflection. Here are deposit yields in Q3:

So deposits are costing more. But because their I/O loan book is not so adjustable, their loan interest did not keep up:

First Republic acknowledges they have a bit of an issue here. They guided NIM down for Q4.

In their closing remarks, they also kind of implied that things will likely get worse before it gets better:

Analysts are a little concerned. This is from another tweet, quoting the JPM analyst, who by the sounds of it has been a bull on the stock, and now appears worried about NIM:

And I think that is the story here.

Going back to the original tweet, let’s sum it up in Reply All style. We start with First Republic, a safe, plain-jane, regional bank that makes a lot of loans that people use to buy homes with. Many of these loans are long-term, interest only loans that appear to not be adjustable rate. Their loan book is also very full relative to their deposits – they have very little room to write more loans. Some investors like Buttermilk clued in that this might be a problem but until now, it wasn’t. In the third quarter it became a problem. Investors saw that First Republic needed to provide higher rates to their depositors but that they weren’t seeing a similar increase in rates from their (largely fixed rate real estate) loan book. This caused their interest margins to decline in Q3 and First Republic had to warn that these margins would likely keep going down. Everyone freaked out and sold the stock.