The Gong-show we call the Russell Rebalancing

I think that the most frustrating weeks in the market are the one’s where you actually get quite a bit right, but you don’t do particularly well because of it.

That is what happened to me this last week.

This was by far one of the most difficult weeks of the year for me. I have no problem with being wrong. I’m wrong A LOT. I can correct it when I’m wrong. Reevaluate, change course. But when I’m right and it doesn’t matter, that is when it is SUPREMELY frustrating. I must have said the words ‘how the hell am I not going up?’ about two dozen times this week.

As I wrote in my last post, I was finding it hard to be bearish at the end of the last week. Sentiment was awful. Everyone was acting like the world was falling apart and all I saw was some tightening and a continuation of the momentum collapse. As such, I had covered most of my shorts. While no one was calling for a rally, that is how I positioned myself.

And we got it! Exactly as I thought.

But here’s the problem. My portfolio is hardly any better off now than then. My wife’s account, where I’m a little more conservative and take smaller long positions, was actually down a bit on the week!

THAT is frustrating. It is one thing to be wrong. But it is another to be right and still be wrong.

So what happened?

Well first, there was one thing I wasn’t right about. Gold stocks. No surprise there. They kept going down. And so I lost money there and have already reduced these positions somewhat.

But my foray into gold stocks was not completely without merit. I was prescient enough to have a revelation on Tuesday. I’ve written a couple of times about how gold and SaaS move with one another with some correlation because both like low real rates. It is not a perfect correlation and other factors impact it, but there is a kernel of truth to it.

This occurred to me on Tuesday, as it also occurred to me that if we were actually going to rally, these bombed out names should do well, so I bought SaaS. I took positions in DDOG, OKTA, CRWD, SNOW and AYX. I have since sold CRWD after it took off 15% the next 3 days.

Imagine if I hadn’t. How much would I have been DOWN on the week?

This is a trade for now. I’m not really convinced this is the bottom for these stocks. I’ve been reading about A. layoffs and hiring freezes around Silicon Valley and B. declining digital ad spend. These two things make SaaS treacherous because of knock-on effects. For example – are companies going to need more JIRA licenses (that is Atlassian) if they aren’t hiring? How about Datadog – this is infrastructure monitoring where pricing is per host – are we going to see as many hosts signed up (hosts are servers or applications that need to be monitored) if companies are cutting back on spend and trying to get profitable?

So buyer beware I think. This is a trade, a bear market trade, and one I don’t want to overstay my welcome on.

Let’s see, what else. Well there was the Canadian dollar, which always works against me on an up week like this, but that is expected. And I also had a couple of single stock hiccups. Rada Electronics got acquired and the stock tanked. CRISPR Therapeutics tanked on their Innovation Day (and I made it worse by selling into the tank, buying back, selling again – indecision is killing me right now).

And then I had this damn Russell rebalancing. I HATE the Russell rebalancing. The number of times I’ve gotten hosed by the Russell rebalancing is too many to count.

Consider BCB Bancorp. This is a stock that is lucky to trade 10,000 shares in a day. You can put a bid out there and it will sit for days without getting filled. Yet on Friday BCBP traded almost 2 million shares and the stock tanked to $16.50 on a day when the market was up 100 points and the KRE (the banking index) was showing a big white candle. There was no news. I am positive it was all Russell funds selling an illiquid stock to balance out their holdings with the new index make-up.

Well at least BCB Bancorp didn’t drop 30% in the last 5 minutes of trading. That happened to Corvus Pharmaceuticals and a number of other biotechs (IFRX was the worst I saw – it went from $1.30 to 78c in the last 5 minutes).

With Corvus, because my luck is complete garbage right now, I actually started a tiny position early Friday (I mean, come on!). I talked about Corvus a while back. It is far from the perfect investment but everything has a price. It is trading under cash, has a stock position in Angel Pharmaceuticals worth $30 million, they have an anti CD-73 molecule that I think could see a partner at some point, and there is enough cash there that I don’t think a crazy dilutive raise is imminent. And most important, it has a chart that is perking up nicely.

I should say had a chart. On Friday at 1:55 Corvus completely fell out of bed as Russell rebalancing sellers sold indiscriminately. The stock went from $1.10 to 80c in maybe 2 minutes.

Look, I don’t like to add to losing positions. It is a rule I try to stick by. That goes doubly for losing positions I just initiated that day. But with Corvus, I think the frustration of the week got to me. I was fortunate (unfortunate?) to get an email alert right away saying Corvus had hit a 52-week low. Then I did a quick check to see if news had come out (it hadn’t), and I suspected this was Russell shenanigans. I knew Corvus had no data pending and I knew there was plenty of cash on handso the chance of a highly dilutive offering seemed unlikely. So I just said screw it, if you are going to give me this stock at 80c I am going to buy whatever you give me.

And that is how I became the largest shareholder of Corvus Pharmaceuticals.

LOL, I’m JOKING, JOKING, kidding, kidding. I couldn’t resist the set-up.

But I did buy some more Corvus, its a 2% position for me now, which is larger than the 0.5% position I had intended to hold earlier in the day. I am hoping to be able to reduce it back down to a more reasonable level this coming week, now that the rebalancing is over and hopefully some sanity returns.

There was one other instance Friday where Russell rebalancing gave me an opportunity that I could not pass up. I tweeted about this one.

As you know, I own Bioceres – BIOX. Its an ag tech name, they genetically engineer seeds, they engineer better fertilizer, better adjuvants. I think it is a very interesting little company that the market overlooks because its in Argentina and trades by appointment.

BIOX has a merger agreement with another company Marrone Bio. I own some Marrone Bio as well because it trades at a discount to the merger value and over the next month or two that should close.

I don’t believe there is any reason to think this merger doesn’t close. It seems to be progressing as expected. Marrone Bio has traded at about a 5-6% discount to its implied merger value for the last while, which is pretty typical stuff.

But on Friday that all went to hell. BIOX went up about 30c to $13 while Marrone Bio went down as much as 7%. Marrone Bio did it on 10 million shares traded, a ridiculously high amount.

Usually any trade with Russell rebalancing comes with the nagging uncertainty of – what if this isn’t because of the Russell? What if the timing is coincidence, what if the stock is going down just because its going down?

Well with Marrone Bio you actually had a benchmark of where the stock should trade. BIOX at $13 means fair value for Marrone Bio, given a 0.088 share exchange, is $1.144. So when Marrone Bio is trading at 97c, that is getting to be quite the discount.

As you might expect I added to my Marrone Bio position.

So those are my Russell rebalancing stories. On none of these stories was I up on the week. I lost money on BCB Bancorp, on Corvus, and on Marrone Bio. I also had a couple other biotechs that had been up with the market on Friday give up all their gains in the last 2-3 minutes of trading. Fun times.

Final topic of conservation – oil. Going into this week I had no intention of buying back any of my oil stocks. I thought I was done for good. I had sold them all back in May, then I fooled around buying them back a couple weeks ago as I was sucked in by FOMO against my own better judgement only to quickly sell them again for what I thought was for good.

But then this week the oil stocks went down, and down some more and down some more. By the end of Thursday Obsidian Energy and Crescent Point were back to levels of mid-February. Pipestone was all the way back to where it was last November!

The only reason that these stocks should be that far down is if you think this is a redux of 2008. And there is a cohort of guys on Twitter calling this 2008. But I do not think this is 2008. I think this is more like a 2001-2002 Triple Waterfall. It is going to take time, it is not going to flush out the excesses in a single swoop, it will continue to ebb and flow until all hope is gone. And this isn’t an oil triple waterfall. its a SaaS/momentum Triple waterfall.

Given that premise, I’m of the mind that this was a little over done for the oil stocks. So I bought back all 3 of the above names. And I bought back PBF Energy as well.

Just to illustrate my thinking here. Crescent Point at its low of $8.50 was, by my calculations, trading at 3x FCF on $100 Canadian dollar oil. That is getting kind of crazy I think.

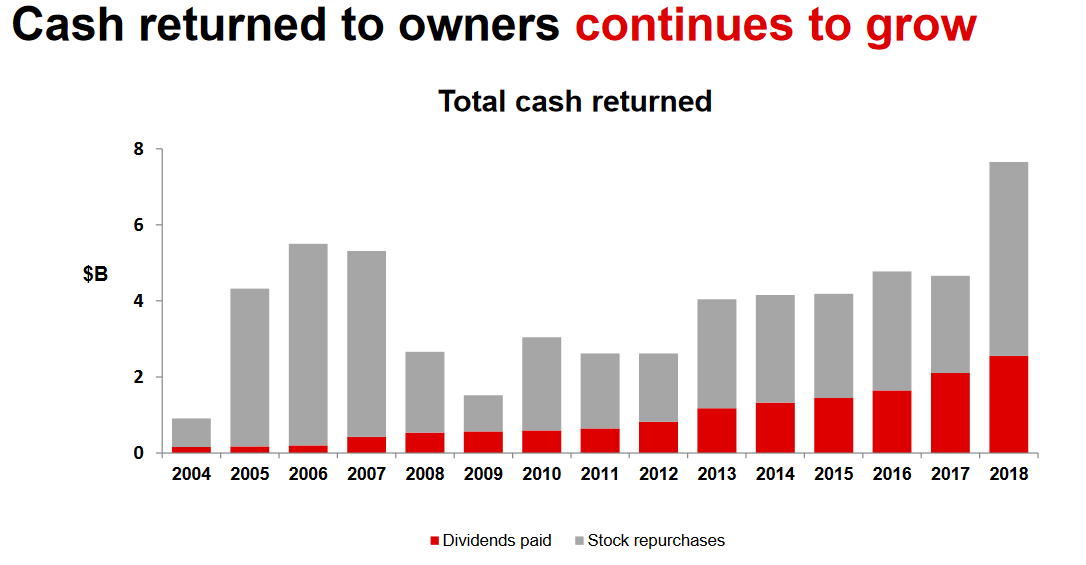

A few years ago I wrote this post where I talked about Texas Instruments and compared it to what I thought with the oil stocks.

Texas Instruments trades at a 4.8% free cash flow yield, so basically 21x free cash flow. They don’t get the valuation because their business is growing at leaps and bounds. In fact, revenue is expected to decline from $15.8 billion to $14.7 billion in 2019. Even looking longer-term, revenue was close to $14 billion back in 2010, which means growth since that time has been minimal. At best this looks like a 5% growth business over the long-run.

But Texas Instruments gets a reasonably strong valuation because the company has been very good at returning cash to shareholders. In particular, Texas Instruments is excellent at repurchasing stock.

I realize that the comparison is far from perfect. Oil is not technology. But see my point. The Canadian oil producers have transitioned to a business model that emphasizes free cash flow. Now they are beginning to return that free cash back to shareholders by buying up their shares.

That kind of sums up my thoughts here again. Crescent Point has a $150 million buyback for the first half of 2022. I betcha that is going to be higher in the second half. Remember that Texas Instruments had a flat to declining revenue business but a great performing stock for years. This was because the company buoyed its stock price by repurchasing shares and investors and traders made this a virtuous circle because they saw the shares were supported.

That is what I expected back in 2019 with the oil stocks and it is what I still expect today. Now that we have the excesses knocked out and all the Fintwit oil bulls back on their heels, I think it is worth taking a position on these stocks again.