Three Community Banks worth keeping an eye on Part II: Shore Bancshares

I owned Shore Bancshares earlier this year but don’t own it now. It was one of four banks that I bought back in January when I jumped into the community bank sector whole heartedly. While the other 3 banks I bought worked out to various degrees, Shore did not, and I sold out shortly after the first quarter results came out for a small loss.

At the moment I’m out, but Shore is not forgotten. I continue to review the company’s results and look for an improvement that would justify an entry point. Looking at the second quarter, while the eventual value proposition is still there, the company doesn’t seem to have quite turned the corner just yet.

Shore operates 10 branches in Maryland and 3 branches in Delaware. The majority of its lending activities revolve around the commercial and residential real estate market in these regions. Shore has a particularly high percentage of commercial real estate loans. Of the company’s $819 million in loans at the end of the first quarter, $315 million were commercial real estate, while $309 million were residential real estate and another $114 million were construction loans.

The loan book has been hit by the downturn in the economy in Maryland. Maryland’s economy is not doing badly, but it is also not doing particularly well. The economy has pretty much mirrored the US as a whole. Below is an Economy.com table of the key economic regions in Maryland. The table denotes each area as either being in recession, being at risk, being in recovery, or expanding.

Another informative research piece on Maryland’s economy was put out by JP Morgan. One point made that I found of particular note (and that is illustrated in the chart below) is that Maryland (not surprisingly) derives a larger than average percentage of economic activity from government.

This would have to be considered a headwind to growth going forward. As one Baltimore economist put it:

We know the decline in federal government outlays has just begun,” said Anirban Basu, a Baltimore economist. “The economic outlook, I think, is pretty grim.”

The article goes on to point out that “because Maryland gets a disproportionate share of federal contracting dollars and other spending, it’s likely to feel a harder hit from any reductions [in government spending]”

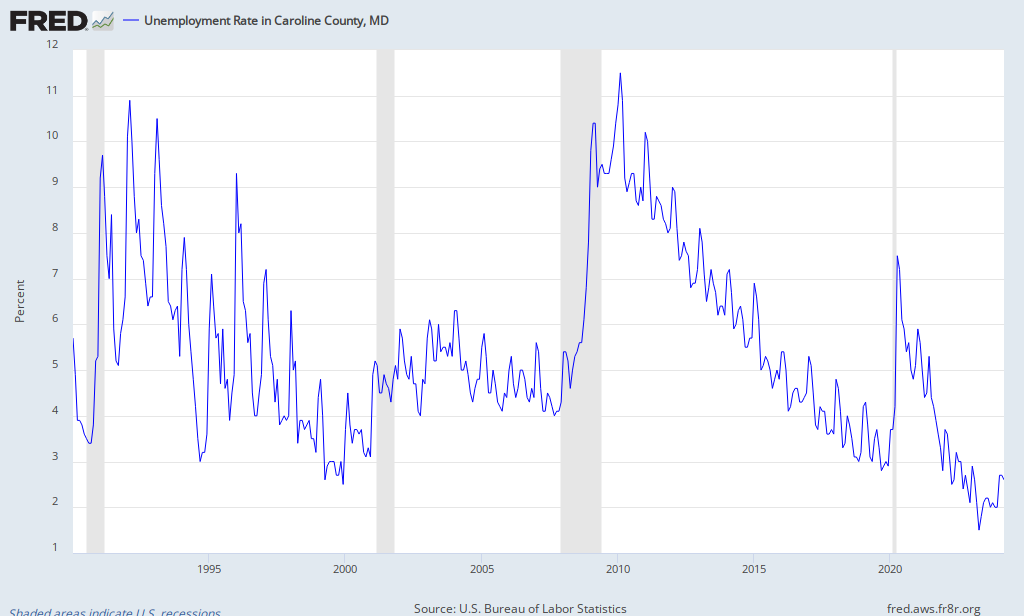

To drill down a bit further to the counties Shore operates, (Talbot, Dorchester, Kent, Caroline, and Queen Anne’s), you can see from the following unemployment charts that each fairly closely mimics the experience of the US, with some improvement from the worst levels of 2009-2010, but still an elevated unemployment level.

The economic malaise shows up in the impaired loan book. Shore has $33 million in impaired construction loans (28.9% of outstanding), $30.9 million in residential real estate loans (9.9% of outstanding) and $30.6 million in impaired commercial real estate loans (9.7% of outstanding).

The problem with Shore remains what it has been for the last few years. How much longer will economy lead to deterioration of the loan book deteriorate?

Company CEO W. Moorhead Vermilye did not paint a terribly encouraging picture in his second quarter comments:

“The operating environment remains tough as we are not yet seeing a meaningful upturn in the real estate related activities that drive the Delmarva economy. We continued to work diligently to resolve and dispose of problem loans, as reflected in a higher level of troubled debt restructurings this quarter,”

So those are the negatives, and why I am not ready to buy Shore just yet. The positives with Shore is its valuation is compelling in the event of a recovery.

The potential when Shore recovers

A great deal of the current problems are priced in the stock. Shore has a tangible book value of over $12 per share. Its trading at less than half of book. The underlying earnings potential of the franchise remains strong; if you ignore the effect of all the onetime charges due to bad loans, the underlying banking business (ex provisions, one time charges, and gains) has been producing earnings at over a $1 per share clip for the last few quarters.

But even this may underestimate the earnings power of a stabilized Shore. Again excluding the onetime charges, ROA and ROE are solidly below where they were before the financial collapse. This suggests to me that once (or I guess if) the bank has its problem loans under control, they can embark on a cost reduction strategy to size the bank to the new level of business.

You can see the same influence if you look at the efficiency ratio, which has been hovering around 100% for the last six quarters.

Not quite there yet

One positive for the second quarter was that Shore did see a significant reduction in charge-offs. Charges were cut to half of what they were in Q1, extending the previous downtrend that had been in place before Q1.

I would be more excited about this reduction in charge-offs if nonperforming assets had shown an improvement. Unfortunately they did not.

Until I begin to see a leveling off and ideally a drop in the non-performing assets, its difficult to make a move into the stock.

Other risks

Apart from the economic risks I already outlined and the presumed impact on the loan book, there really isn’t a lot else to worry about with the business. Reading through the risk factors of the recent 10-K was mostly an exercise in the plagiarisms of the standard banking risk fare:

- Concentrated Commercial real estate loans are being affected by the economic downturn

- Interest Rates falling

- The market value of their investment portfolio declining

- Competition

- Funding Sources

- Key Personnel

The only item of any concern is the one I’ve already highlighted. Their loan portfolio, and in particular their commercial real estate portfolio, needs a strong economy to right itself. Its really just a wait and watch until the bad loan book stabilizes.

Waiting on my hands

The reason I am reluctant to buy Shore is because until they start to see a sustained downward trend on their nonperforming loans, the company remains at risk for panic. We saw that panic back last fall when the stock fell into the mid-$4s. It could happen again with the right confluence of European and US financial worries. Rightly or wrongly, the stock will likely remain range bound until the book turns around, and we won’t begin to see that until at best October, when the next quarterly is released. I, before then, the stock dropped another 15%, which would put it in the $4.50 range, I would be tempted to buy. Absent that, I will wait patiently on my hands.

{kind=link}