Oneida Financial – Local MHC Continues to Make Good

I got introduced to the idea of buying regional banks stocks about 6 months ago. Two separate catalysts piqued my interest in the idea:

- Last summer I read the David Einhorn book, “You Can Fool Some of the People All of the Time”. In that book, which is about a fraudulent business development company called Allied Capital, Einhorn spends a chapter outlining his investment philosophies. One of the ideas he puts forth is investing in mutual holding companies. Seth Klaman has been another proponent of investing in MHC’s.

- Tim Melvin’s trade of the decade. Melvin, a fairly well known value investor, believes that the small regional bank stocks have been beaten up well beyond what is justified and that their recovery represents the trade of the decade.

After spending a few months getting to understand the banking industry, and scouring the net for cheap MHC’s trading below or at book value, I stuck money into a couple of them, with one of those being Oneida Financial. Now, in the 5 or so months that I’ve owned it the stock has done absolutely nothing. You might want to take that as neither a good or bad thing in this market. Oneida has bounced back and forth between 8.40 and $8.80, but does not seem in any hurry to break out in either direction.

I have already written an extensive write-up on Oneida’s regional banking business and why I picked Oneida as one way to play this trade of the decade. I’m not going to go further into the details of my reasons here. I’m just going to focus on their second quarter results.

Another strong quarter for earnings. Oneida earned 24 cents for the quarter. Stripping out loan loss provisions they earned 25 cents. Over the past 4 quarters their earnings have been 84 cents basic and 91 cents after stripping out loan losses. Below is a chart of their earnings over the last 5 years. There has been a steady upward march over the past two years.

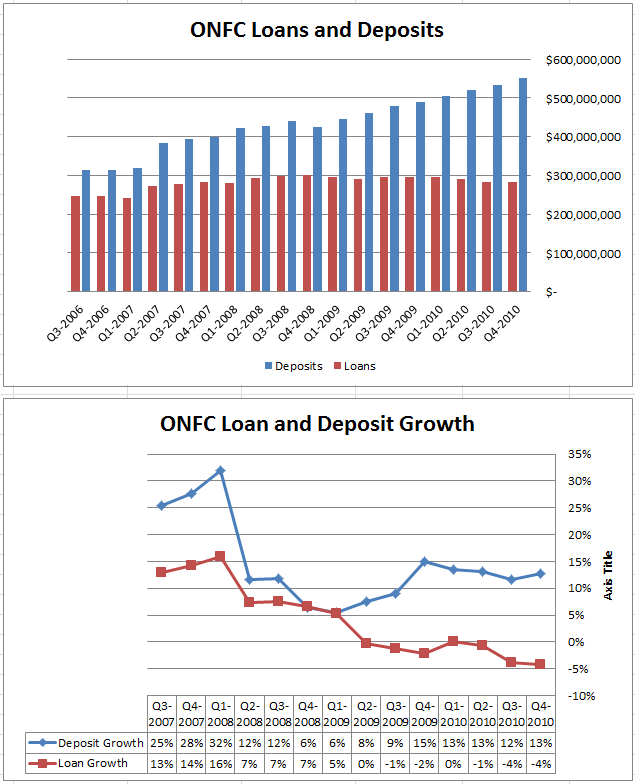

I bought Oneida in part because I thought they were cheap based on earnings power. They should easily be able to earn a $1 next year, meaning they are trading at less than 9x earnings on a forward basis. What I have been waiting for is for Oneida to begin to grow their loan book again. Its been shrinking (albeit at a small rate) since the 2008 debacle. This looks like it might be starting to change.

Oneida’s loan growth is a bit tricky because they sell of much of the fixed rate loans they generate. So to get a true picture of their loan generation, you have to add back the fixed rate loans that are being sold off. Below is a chart of loan growth at Oneida showing both growth before and after accounting for the fixed rate loans sold. Up until this last quarter loan growth has been negative since Q2 2009. That changed this quarter with the uptick.

Deposit growth declined somewhat in Q2 from the last few quarters. Nothing to worry about yet though.

The company continues to sell below book value and tangible book value. More importantly, book value continues to grow at a smart pace.

{kind=link}