Something pretty big happened on Monday. Intellia, which is a genome editing company that uses CRISPR to slice up, remove and add DNA segments, announced some pretty amazing results from their Phase 1 trial targeting a rare disease called transthyretin (ATTR) amyloidosis.

ATTR amyloidosis happens because of a mutation to the TTR gene. This mutation makes the liver produce misfolded TTR proteins. These misfolded proteins get into other organs and wreak havoc on them.

With CRISPR/Cas9, Intellia’s therapy targets the gene and basically knocks out the mutation from the strand (this is called a “knock-down”). Without the mutation in the gene, the body stops producing the misfolded proteins and all is well.

From FierceBio: David Lebwohl, M.D., Intellia’s chief medical officer said that the the result was “beyond what we expected.”

These results, it seems to me, are a very big deal. Why? Because this is the first time that the CRISPR/Cas9 system has been used in a trial, inside a human being, to change a gene (called in vivo).

Up until now, if you wanted to change a gene with CRISPR, you had to do it in vitro – which means either taking cells out of the body or using someone else’s cells, slicing and dicing the DNA, and then injecting them back in.

Obviously this is not ideal. It really limits the usefulness. It is much better to be able to administer the therapy into the body and let the work happen there.

And now we have evidence you can do that. A one time treatment and boom – a functional cure to an awful disease.

This is the first time I’ve written about gene editing with CRISPR (I think?) but I have been working on this for months. I’ve read three books on the topic (one of the co-founders of Intellia, Jennifer Doudna, is the main character in the book The Code Breaker, which was a good introductory overview of the sector for me), and have been pouring over brokerage reports and papers on it. I’m still a newbie but starting to get the just of it.

Enough to know that this is a pretty big deal.

For some perspective, this is only a Phase 1 trial, so there’s that. And the target that Intellia chose is a gene that is in the liver – the liver, from my understanding, is a relatively easy target because getting therapies delivered to it migrate there easily.

As a final caveat, one of the big problems with CRISPR is something called off-targeted edits, which is exactly what it sounds like, editing genes somewhere else, and Intellia noted 7 of them in this case. These could be bad or they could be nothing. From what I read we often won’t know if they are a problem until they are a problem.

But even with all these caveats, the big picture is that it worked. In fact, the results were far better than anyone expected.

The thing about in vivo CRISPR therapies is that if they work, they can basically knock out problem genes or replace problems genes or add good genes with a single treatment. Instead of treating symptoms or supressing a problem they are really knocking the problem right out of the body. It really is a game changer.

The obvious thing to do after these results would have been to buy Intellia. So of course, because I am an idiot, I did not do that. It was just up so darn much Monday morning – but of course since Monday it has been up even more.

Instead I bought all the others: CRSP, EDIT and GRPH. CRSP has not really moved since Monday, likely because its been so overbought, but the other two have continued to move up.

Even though these stocks have very high market capitalizations and, of course, no real revenue, I felt that I just had to own them. Literally the only thing that had kept me from these stocks in the past few months was that I kept thinking, if this is just a treatment that is only done in vitro, that is going to be pretty limited application.

But that is no longer the case. I feel like it will take some time for the market to truly catch up to that change.

I always struggle with days like Thursday. A sudden about face in the market and you have to figure out what to do.

Two days later, I’m still not sure what to do. I have done stuff, but I may undo them or I may do other things altogether.

Four sectors that I own stocks in took a dump Thursday – steel, shipping, banks and gold.

Gold

So first off – gold. This one is easy. You just sell. I have found that it is already best to sell gold stocks first and ask questions later. If it turns around just buy them back. There is always a chance to buy them back with gold stocks. I have invested in gold stocks for 15 years. I can’t think of one time where they “got away from me”.

I don’t own New Gold any more, I don’t own any Gran Colombia (which I had bought Monday) and I sold most of Wesdome and Fiore.

The only thing that gives me pause is Wesdome – and that simply is that it hardly sold off.

The stock is (relatively) so strong. I don’t know what is going on there but while bigger gold names fell 5-6%, Wesdome was actually flat at one point on Thursday. That is why I kept a bit.

Banks

Second – banks. With the banks I am in a different spot because I have sold a lot of my positions. So this is more about whether to buy them back.

I was really surprised to see both the banks and gold down. They have been a hedge to one another over the last year. When one is up the other is down.

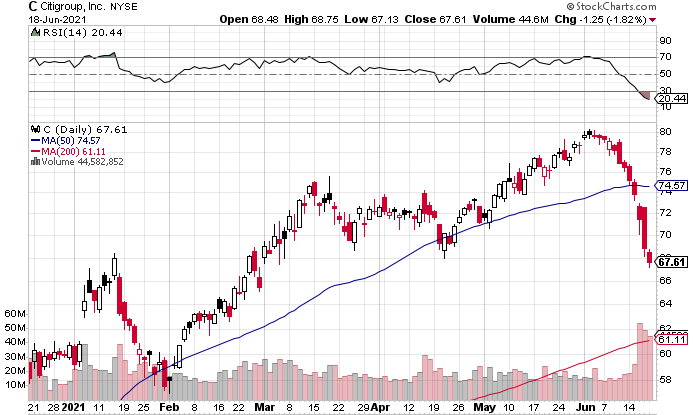

When you look at the big money center banks, they have been down for days. The charts of JP Morgan and Citigroup in particular are really ugly. I mean, what the heck is going on with this:

This large bank move was not Fed induced by the looks of when it started. It just carried over to the small banks on Thursday.Whenever the banks start going down I feel like I have to figure out what it means. This case is no different but I have not figured it out yet. I won’t be adding to my positions until I do.

As for the other two – shipping and steel… I am battling my mindset versus the volatility of these sectors.

My mindset is – do not lose money. If I make some great, but more important, don’t lose any. The problem is that shipping and steel are two sectors where you can lose money very quickly if things go against you.

Which is why, even though they do not make up a particularly large part of my portfolio, they are taking an outsized amount of my attention right now.

Shipping

In the case of shipping, the stocks suffered quite a drop on Thursday, which makes the decision more immediate.

But I sold some of the shippers the week before so that played into it as well. I did not go into Thursday’s drop with full positions in these names.

Nevertheless, I did sell some more. For reasons I will explain. But on Friday I added a new container (not containership) idea, Triton International, so that offset those sales some. I still own less of these stocks than I did coming into Thursday but enough to be nervous about them going forward.

Containerships

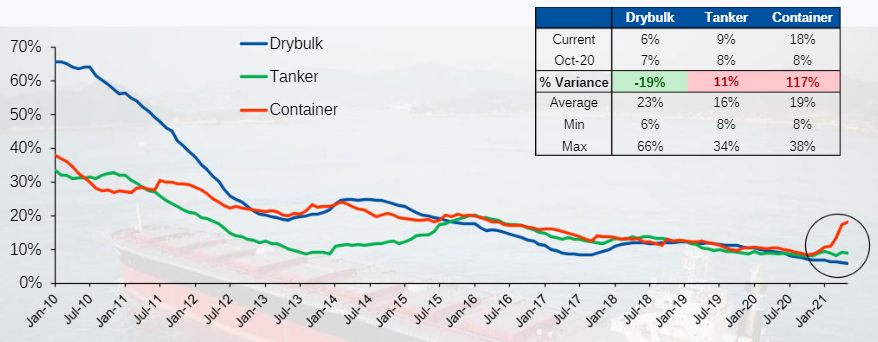

Let’s go back to where the market is. First, containership rates are still at all-time highs and they look to be going higher.

This article, from American Shipper, says that rates are actually “accelerating”. There is a huge backlog of ships (90 of them) just sitting off the coast of China ports because of a Covid outbreak at the very large port of Yantian. While this backlog has come down a bit (from 104 a week previous) that is only because the ships scheduled to dock at Yantian are omitting the port altogether.

Ships omitting the port has consequences because the containers that are supposed to be loaded from the port are stacking up. According to this CNBC article:

Approximately 160,000 40-foot containers, the equivalent of 300,000 TEUs, or 20-foot equivalent units, are waiting to be exported, according to logistics companies with operating knowledge of the port.

300,000 TEUs would be about 10 days of shipping from the port.

Yantian Port now says it will be back to normal by the end of June, but just as it took several weeks for ship schedules and supply chains to recover from the vessel blocking the Suez Canal in March, it may take months for the cargo backlog in southern China to clear while the fallout ripples to ports worldwide.

“The trend is worrying, and unceasing congestion is becoming a global problem,” A.P. Moller-Maersk A/S, the world’s No. 1 container carrier, said in a statement Thursday.

Over 90% of the world’s electronics are exported out of the Port of Yantian.

Another article from Lloyds List says it will take weeks to work through the backlog and that is the best case scenario.

The gcaptain article estimated “the congestion in Yantian will take six to eight weeks to clear. That timetable is a problem because it extends the disruptions into the late-summer period of peak demand from the U.S. and Europe, where retailers and other importers restock warehouses ahead of the year-end holiday shopping rush.”

So the port congestion runs into the holiday rush runs into other economies opening up as they become vaccinated. And no significant new ships builds are coming along for 2 years.

Meanwhile the containership companies are booking 2 or 3 year charters at rates well above $30K/d. Today I saw a 3 year time charter at $42k per day and a 5 year charter at $34k per day.

The much, much hated NMM (just read the post of @the5hippingman on twitter) charted 5 containerships for 36 months on Tuesday. With these charters these ships will bring in $60 million of EBITDA per year.

That is from 5 ships. NMM has 51 dry bulk ships and 38 containerships. NMM has an EV of $1 billion.

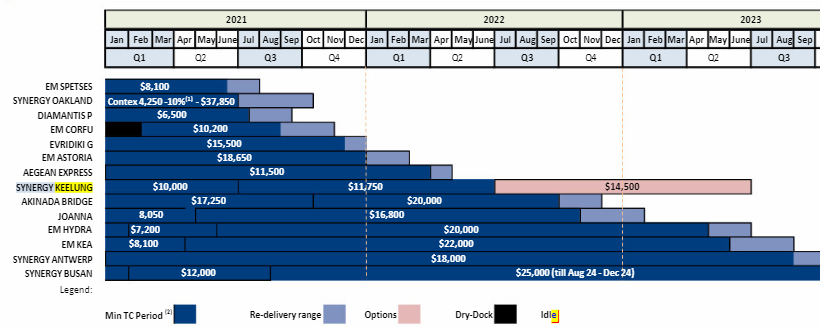

As for Euroseas, which has been my main containership play, they have about half of their vessels opening up for new charters between now and the second quarter of 2022.

Those vessels are going to recharter at much higher rates.

The SPETSES, DIAMANTIS AND CORFU are all currently operating at charter rates of $7k-$8k per day. At current rates they will be able to re-charter at $20k-$25k. The OAKLAND, which is a bigger Panamax ship, was booked out at $4k per day in Q1. In Q2 they will be on a better but very short charter of $38k until July. When that charter ends, these sort of Panamax vessels are getting $40k for years right now.

Analysts have been raising estimates for Euroseas for some time, and we are now at an average of $7.42 EPS for 2022.

So the market looks very positive. What makes me nervous about the containership market is the new build order book. That order book (which I showed last post) has grown a lot in the last 6 months or so. That makes me think that investors will be less likely to bid up containerships on current earnings, as they realize those earnings won’t last.

The other thing that is tough about containership stocks is there just aren’t that many stocks out there, at least on North American exchanges. It is one of the reasons I bought Triton.

The cheapest of the bunch is NMM, which is one of the basket of 3 that own, but it has a real problem with credibility, and because their CEO, Angelica Frangou, does not always do what is in the best interests of shareholders, there is a chance that some day we wake up to news with NMM that destroy the value of the 2x P/E valuation.

Euroseas and Danaos are both up a lot in the last few weeks. So its really hard not to be trimming those on the least bit of worry.

So I sold some Navios and Danaos Containerships and a little more Euroseas. But I still own all to a lesser degree, as the market is so strong I could easily see it having at least one more leg up.

Dry Bulk

The dry bulk market is a little different than the containership market because rates are just strong, not crazy, insanely strong, while the order book is very, very low (see my last post for this). For this reason, I am a little less trigger happy with my dry bulk stocks.

I did lighten up on Star Bulk earlier this week but I ploughed about half of that into Diana Shipping and Globus Maritime, so my overall exposure to dry bulk is still about 75% of the what it was (with containerships I’ve taken about 1/2 off the table overall).

Together with Grindrod, these moves mean I’m moving down the chain in quality and size, which might be seen as a dumb idea if we are moving towards the end of this move.

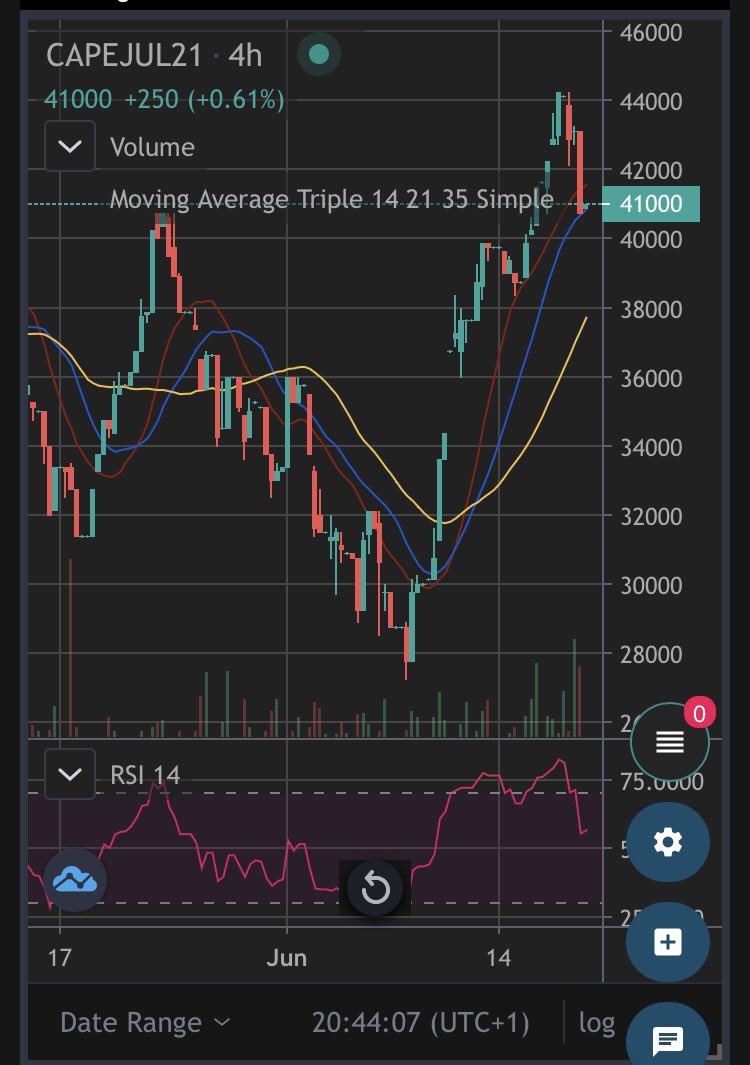

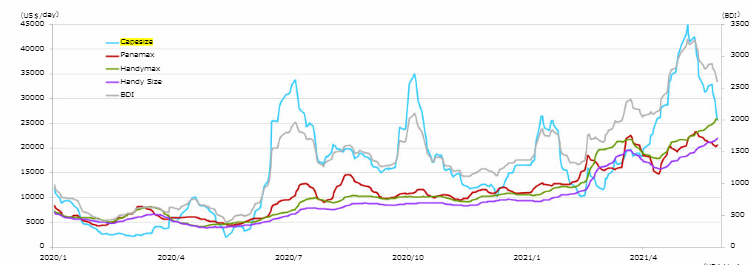

In the dry bulk market, while Capesize FFA’s (that is future freight rate agreements) have pulled back a little the last couple of days, they have had a very good move over the last 2-weeks and they are around $40k, which bodes well for dry bulk shippers.

The smaller size ships, so the Panamax, Supramax and Handysize, are seeing even better rates. Grindrod and Globus Maritime both own these smaller ships. Diana Shipping owns both the larger Capesize and the smaller Panamax/Supramax size.

The crux of my desire to hold dry bulk is that stocks like Grindrod are just so cheap on multiples. I’m going to go through Grindrod as an example.

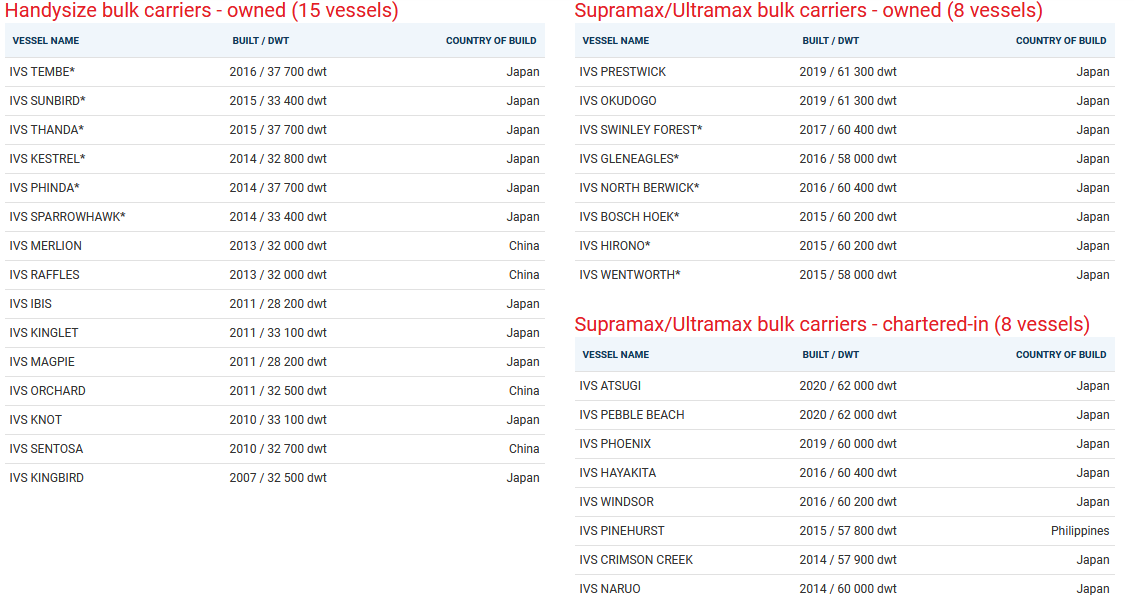

Grindrod has 15 Handysize and 16 Supramax size vessels.

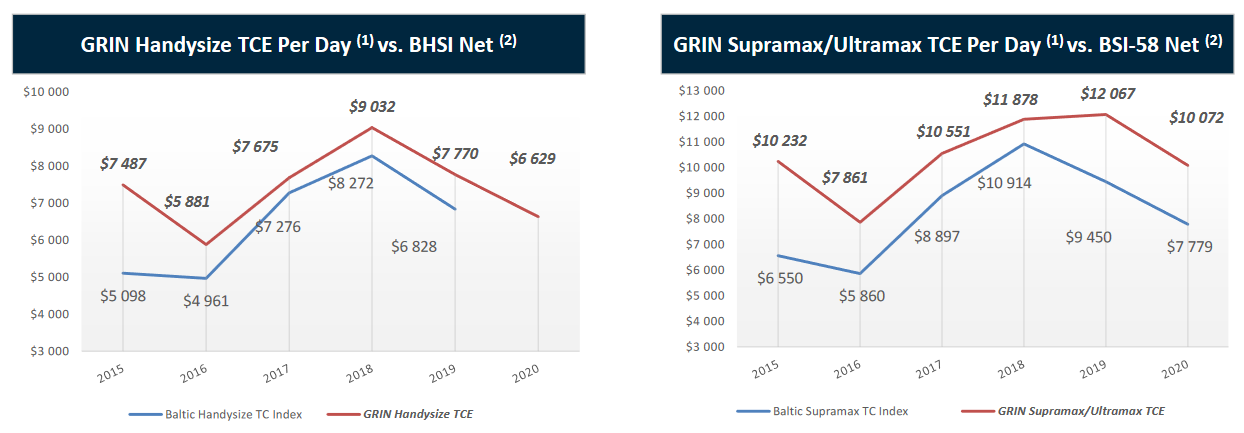

Now let’s look at where rates are versus where they have been. Supramax vessels are contracting out at $32k per day right now. In 2020 Grindrod averaged $10k per day. Handysize vessels are going for $22k per day right now while Grindrod averaged $6.6k per day in 2020.

So Grindrod is experiencing far higher rates now that it has in the past. I mean, we are close to triple the 5-year rates on these ships.

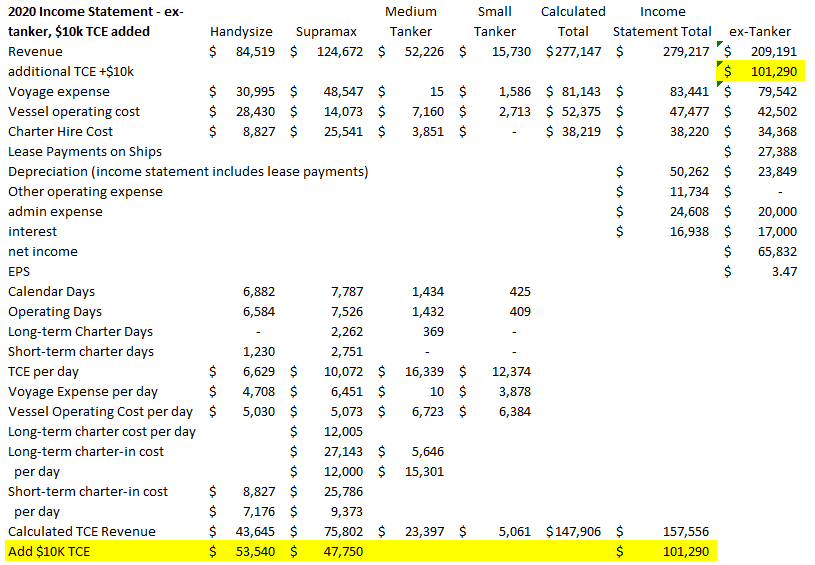

I did a very back-of-the-napkin estimate of what even an extra $10k of TCE means for Grindrod. $3.50 of EPS. You can see the results below.

The spreadsheet is a bit convoluted, but the important column is the last one, where I have taken the 2020 numbers, removed the impact of tankers (they have since been sold) and added revenue from an additional $10k TCE for the owned and long-term charter operating days.

What is worthwhile pointing out is that A. TCE’s right now are more like $15k-$20k above the 2020 numbers. B. I’m assuming no positive impact from the short-term charter-in days (which were ~1/3 of Supramax days in 2020). C. I did not reduce the debt payments even though Grindrod has paid off about 1/4 of their debt. And D. cash flow is higher – nearly $90 million.

So to sum this up: Grindrod has a market cap of $200 million right now. Cash flow at the +$10K TCE level is close to half their market cap. Every $10k increase in TCE after that is another ~$100 million.

So that is why I am reluctant to sell. Particularly when the order book for new builds is extremely low, it appears that the environmental regulations coming into play on propulsion systems is going to make shipowners wary of ordering new builds, and shipyards are filled with orders of LNG and containerships for the next couple of years anyway.

Whereas with containerships I am wary of how high investors will bid up stocks when the end of the cycle can be seen, I cannot say that for dry bulk.

Steel

In the case of steel, the two stocks I own, Stelco and Algoma, did not really go down much. So the question becomes, do I sell while I still can?

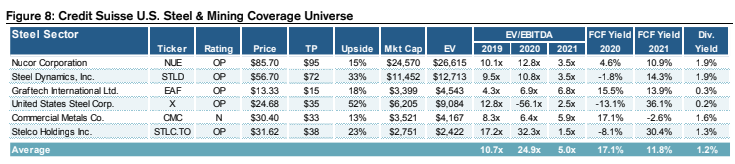

While steel makes me very nervous, I still decided to hold on. As I wrote about previously, both Stelco and Algoma are very cheap compared to their US peers. According to Credit Suisse, Stelco trades at like half of what the US steel companies do. I don’t see any good reason for this discount.

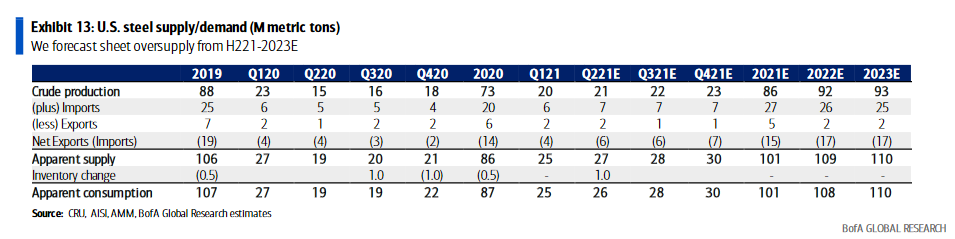

The bear case for steel is summarized by Bank of America, who has been calling for “Steelmaggeddon”. Steelmaggeddon for some time. They are basically saying a bunch of new supply coming on that will wipe out the deficit and bring prices back to $600/t next year. Actually, BofA was saying by H221 but that does not seem likely now, so they have pushed it out to 2022 now.

This is BofA’s US supply/demand forecast for their Steelmaggeddon forecast:

It actually seems pretty balanced to me (the numbers don’t actually add up either). It also depends on steel demand not getting back to 2019 levels until 2022.

On the other side, Morgan Stanley is pretty bullish steel prices. They think steel could stay near the $1,700/t level until Q1 of next year.

They note that: demand strong across all end uses, demand does not appear to be inflated by significant double ordering, inventories are uncomfortably low and some service centers are seeing “unprecedented level of contract demand”.

Average estimates are for Stelco to earn $13.50 this year, followed by $6.50 next year (because no one believes steel is going to stay near this level). Algoma isn’t covered by anyone but its multiples would be about the same.

The reason to keep an eye on steel is China and carbon. If China is serious about their commitments to greening steel, they have to begin to slow down the dirtiest production.

China produces about 1 billion tonnes of steel a year. If China cuts even 1% of its dirtiest steel production, that is more than all the new North American capacity adds next year. And China is talking far, far bigger numbers than 1%.

FT has been the best on reporting this story. They said in an article last week that:

These changes are going to have a big impact on China steel production over the next 4 years:

The Tangshan province, which produces 14% of China’s steel promised big cuts earlier this year:

It is almost unimaginable to me that China could drop that much steel production. The market would go crazy. Chinese steel companies are already trying to build plants outside of China to offset. It is going to be a delicate balance.

And so far this year, we aren’t seeing the cutback. Steel production in China, at least the official numbers, is up.

So it might not be a huge cut overnight. But my point is more on direction. China is not going to be adding steel production like they have, at the margin they are more likely to reduce it, and as a result it is quite possible we could see exports from China decline.

This seems to me to be the sort of thing super cycles are made of.

Going back to that BofA supply/demand balance, they are predicting exports to the United States to increase.

Add it up, and I’m not ready to through in the towel on these two names just yet.

So I am selling. Not completely, but I pared down a bit (because, after all, this is shipping).

But…. even though the move last week was really good (especially for Euroseas) I am reluctant to take all my money and run after one big week.

My reason? The set-up just seems so darn bullish. Everything I read points to a tighter market in the months ahead. There are 300 containerships trying to dock around the world that are just sitting there waiting. There is an orderbook of containerships and bulkers that won’t deliver material new ships for 2 years minimum. The drybulk order book seems particularly thin. There are environmental regulations on the horizon that are making shipowners think twice about ordering multi-million dollar fossil fueled propulsioned ships that could be deemed obsolete in a few years. There are sky-high rates going into seasonal strength. And now there is COVID at a big Chinese port that has backed things up in China to even worse conditions than the already bad ones they were in. I mean, yeesh.

I subscribed to J. Mintzmyers SeekingAlpha platform a couple months ago, when I thought there might be something to this whole shipping trade. I’m not going to share all of what he says or the research he provides because the subscription is a lot and I don’t want to get into trouble.

But I think I can safely give my conclusions. I have listened to all the post-Q1 interviews that Mintzmyer has done with shipping companies and they are unequivocally bullish. There is just so much running in favor of containerships and dry bulk right now. And I said this in my last post: that even though it is the containership market that is strongest right now, I have a feeling that it will be the dry bulk market that actually does the best in the longer run.

So I am going to stick this one for a while yet. These markets seem destined to get tighter, which could make the stocks go up even more.

Flip-flop on Biotechs

A little over a month ago I sold pretty much all of my biotechs. It was like a mini biotech-centric version of one the portfolio purges that I do from time to time. I stayed out of all my biotech names for about a week or so. And then I bought them back and then some – at pretty much the same prices I sold them at. You can see this in the portfolio page – Lyra’s average cost, for example, went from $10 to $7. That wasn’t magic, it was just me selling, and then thinking better of it.

Why I sold is clear – it was not working. But why did I buy back? During that week I held no biotechs, the stocks did nothing. But they also did nothing. Which is to say, they stopped going down.

I watched Lyra for 5 days, without any skin in the game. Those days are circled in green.

During that time the stock felt like it just did not want to go down any more. I had been watching the stock since December and the intraday action was different than it was during the March to May period when the stock fell and fell and fell.

But it was not just Lyra. A number of the Biotech stocks that I track were following the same pattern. It made me go hmmm. And that led me to buy back Lyra, and add two other names.

I added Zosana Pharma and Clearpoint Neuro. I am not going to talk about Clearpoint because everyone talks about Clearpoint and I am just renting here, not owning.

As for Zosana, I owned Zosana briefly in February when biotech stocks were doing those crazy pre-market gap-ups. For whatever reason, Zosana is one of those 2nd or 3rd tier momentum stocks – not with the consistent momo of a GameStop or AMC, but a stock that every so often catches fire and runs up. If you can catch that, you can do okay on it.

But Zosana is not just a do-nothing shitco. Well, I guess it kind of is, but not completely. They do have something that may be worth something someday. Maybe.

Zosana has been going through clinical trial for a transdermal microneedle form of a drug called zomitriptan.

Zolmitriptan is used in acute migraines. Zolmitriptan is one of most potent triptans. The triptan market is big – $4.8b market overall. The standard delivery for zolmitrptan is oral, injectable, or nasal. Non-orals represent $650mm of the market. Zosana is offering a different delivery, through a patch. Indications from the trials are that it works better than the existing alternatives.

So Zosana has potentially a better vehicle. It is called Qtrypta. You put this little patch on and the drug is administered through your arm.

I got interested in Zosana a few months ago because the stock is very reasonable (the stock has a $100 million market cap and $17 million of cash), and the brokerage reports that I read seemed quite positive on the outlook.

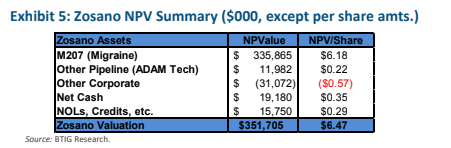

While I never know whether I can trust the research of HC Wainwright or BTIG, they at least paint a compelling upside if all goes according to plan. For example, BTIG gave the stock a $6.47 NAV in their initiation report:

Zosana’s problem is that the FDA did not approve the drug after Zosana completed their Phase 3 study. They gave them a complete response letter, or CRL, which is usually a letter saying no dice.

But in this case the letter just outlined a few issues that Zosana had to rectify before the FDA would approve the drug. They wanted clarification on safety data, and they wanted Zosana to repeat the bioequivalence study. It seems there are concerns that the drug levels administered to all the patients were not consistent.

While none of this is ideal, it is also not a death knell. In April, Zosana announced that they had met with the FDA and come up with an acceptable study to satisfy the concerns. They said “we believe that this study can be executed quickly and will address the last remaining clinical request from FDA regarding the resubmission of our NDA for Qtrypta”.

Ok, so great. They do the study, maybe they get approved, maybe they are successful at marketing their alternative delivery system, maybe the stock gets to the BTIG NAV. Maybe not.

I am not smart enough to be able to tell you how this all plays out in the next 1-3 years. But I can say that: A. the bad news is baked in, B. the news flow seems to have gone positive, C. the stock is one of these “jumpy” meme-esque kind on names in a market that is going meme-me again, and D. the stock chart is a lot like Lyra.

So…. worth a punt.

Eastside

Eastside Distilling has been a frustrating laggard up until just recently. I wrote about Eastside a couple of times last year. I took what is for me a pretty large position and watched the stock drastically underperform other microcaps through the end of last year and the beginning of this year.

It was painful. Apart from one short-lived run up at the beginning of February, Eastside languished at about the price that I bought it.

What was confounding was that Eastside seemed like such a perfect play for reopening. The stock was well below its pre-pandemic level (it was in the $1.50 range vs $3 per share a year before). Eastside had clearly suffered from restaurant and bar closures and that would be changing shortly. And… at a corporate level the company was in far better condition that it was a year earlier. The new management team had a plan, they were clearly focused on driving cash and not just running up revenue and losses.

Yet the stock did pretty much nothing.

That has changed in the last few weeks.

The stock began to rise shortly after the company announced Q1 results. While those results were nothing particularly amazing, they were another step in the right direction. So who knows, maybe management talked to some fund, maybe there is a brokerage report that I don’t know about? Someone is buying the stock.

What I do know is that the new management at Eastside has done an admirable job of reducing costs, selling off unprofitable product lines, monetizing inventory, reducing cash burn and just generally turning the business around.

The two numbers that highlight the turnaround are that. year-over-year, gross profit was up 25% and opEx was down 17%. Management has really focused on selling spirits that have better gross margins while dialing back their marketing and G&A expense. No surprise that leads to a more profitable business.

Having said all these positives, I am starting to take some of my position off here. It has been a good run and while I can envision how this could be a $5 or $10 stock some day, it is going to take time I think and god only knows what the bumps in the road will be.

But beware! This has been my Achilles heel. Over the last 9 or so months I have been burnt by taking profits. I have taken profits on soooo many stocks that have gone much higher. Kopin, Silvergate, Inspired Entertainment, Identiv, Beam Global, Prothena, Bionano, Foresight and on and on – it’s ridiculous when you think of all the stocks that have been doubles or even multi-baggers after I sold out.

I have treated all these tiny little microcap speculations the same way I always do – when they go up enough, start selling (while you can). In the past, that has been the prudent strategy. Over the last 12 months, it has meant leaving a lot of money on the table.

But what can you do? You gotta stick to your playbook.

Tornado

Speaking of moonshots, and one that I have not sold: I have no idea why Tornado Hydrovacs is going up.

This is one of those stocks that I have owned forever. It was a spinout of Empire Industries, and while I gave up on Empire (now Dynamic Technologies) a while ago, I have stuck with Tornado.

Tornado makes hydrovacs. They operate out of Alberta. Right before Covid they bought a large facility in Red Deer to expand their production. Everything seemed to be on-track. But…

Obviously, since Covid the results have been pretty meh. As of Q1, they had not turned around just yet. In the press release of their Q1 report Tornado said “production at the facility located in Stettler, Alberta was reduced by approximately 60% for the second half of 2020 and 20% for Q1/2021. As at March 31, 2021, approximately 25% of the Company’s employees had been permanently laid off.”

Tornado did make a reasonably positive outlook statement in their Q1 MD&A:

I can kinda get that this stock should do well over the next couple of years. It should benefit from the increased infrastructure spending and such. And that is really why I have held it. But based on the available information, I am not quite sure why its run up like this over the last couple weeks.

Two more thoughts/ideas and then I will be done.

Vertex and Vidler

First, I bought Vertex Energy, a stock I have owned previously, when they announced the acquisition of a refinery from Shell. Hat tip to Glen who compelled me to look at the news after I was so skeptical about it that I ignored it for a day even as the stock went up 100%. I don’t really have much more to say about this one because honestly, I just don’t know. Vertex made a very cheap refinery purchase that they say they can transform them into a biodiesel powerhouse. If they can make good on this, the stock is only getting started. But because I don’t really know, I already sold half. I would probably sell the rest on a move to $12+.

Second, I bought a company called Vidler Water Resources. Vidler owns and develops water assets. I am still pretty early into the name and so I’m still trying to figure out all the details, but the big picture looks good.

Vidler owns water rights and water credits in Nevada, Arizona and Colorado. There is a big water problem brewing in these states. Lake Mead, which is the Hoover Dam lake, is drying up. If you google search Lake Mead you can read about a dozen articles describing how bad its getting and how rationing will be in store this year.

So Vidler is in the right place at the right time. What I haven’t yet worked out is how much they will benefit from the increasingly desperate search for water, it seems pretty clear that they will benefit and the stock does not appear that expensive.

I got the Vidler idea from mrmojorisinX on twitter. He is a smart hedge fund guy that makes very hard to understand tweets that never name names but where if you are enterprising enough to decode what he is saying you can sometimes get very good ideas from. This looks like one of them to me so far.

Gold Stocks

Finally, last thing, gold. So… I’m doing pretty well on my gold names, but that doesn’t really have much to do with gold. It is really to say that I am doing pretty well on Wesdome. Wesdome has been great because the results at Kiena have been tremendous and the stock is going up even as gold is going nowhere.

But that brings me to my larger point. I’m not quite sure what to make of gold stocks right now. They are… strong. That is not a word you associate with gold stocks 95% of the time. But gold stocks are surprisingly strong given that gold is not.

I’ve woken up about a half dozen mornings in the last 3 weeks, looked at the price of gold, looked at the sentiment on gold-twitter, and thought, “yup, this is the day the gold stocks are going to get creamed”.

And then it didn’t happen.

Even today, gold stocks opened down. But they haven’t stayed there.

If this was any other sector I would be saying, THIS IS A SIGN!. But with gold stocks, with whom I have battled with for years with which I am perennially disappointed when I overstay my welcome, I have zero trust in even the strongest signals and therefore I will say nothing except for – it is interesting.

I have been in the shipping trade for about 4 weeks now. Up until today it has not really worked.

The stocks have bounced around. I have made a little on ESEA and GRIN, lost a little on NMM and SBLK and done nothing at all with DAC. Overall, I have been flat.

I was beginning to doubt the idea. It was the usual doubt – sure the stocks seem very cheap, but maybe the market just won’t care?

There are plenty of reason for the market not to care. For one, these stocks are well off their lows of last year. For two, the shipping business is terrible, self-serving and full of management teams that have a history of incinerating cash. For three, rates are at decade highs and why get in at the top?

FWIW there are really two separate ideas here. There is a containership trade and a dry bulk trade. They have pretty different dynamics, so you need to talk about them separately.

The containership trade is the more immediate of the two. The shortages in containerships is happening now.

Containership rates are off the chart. They are at (I believe) all-time highs.

The first question that comes up when you see this chart is whether this is just a blip due to the pandemic.

To some extent that seems to be true. We have the restocking of inventory at the same time as post-pandemic demand in the United States is sky-high. There are also shutdowns at at least one very large port in China because of a COVID outbreak.

But if this was just a blip, what you would expect to see are very high spot rates and much lower two, three and four year charters.

But that is not what is happening. Containership owners are booking long-dated charters at huge rates.

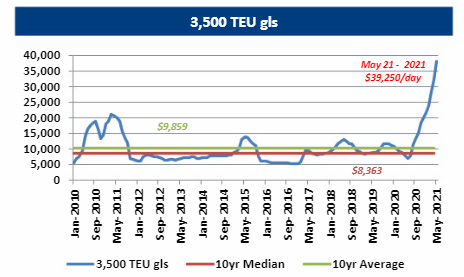

Just to give one example. A 3.8k TEU containership (a TEU is one of those big cargo containers that stuff gets shipped in) was booked last week for 5 years at $35,000 per day to CMA CGM.

A 3.8K TEU is a Panamax size (Panamax is between 3-5k TEU). This chart is from the Euroseas Investor Presentation:

3,500 TEU shipping rates have not been above $10K per day for years. And yet now there are customers willing to book them out for 5-years at $35K per day?

This makes me stand up and take notice. It does not look like a blip to me.

Yet the market is trading these stocks at levels that is saying it is just a blip.

I mentioned the Euroseas analyst estimates in my last post. Average estimates (albeit this is from the only two brokerages that cover them) are $6.50 per share EPS for 2022. That means the stock has been trading at a little over 2x earnings. This would make some sense (but not a lot in my opinion) if spot rates were sky high but long-term rates were much lower. But it makes no sense when ships are booking 5 years at $35K.

The only gotcha in the idea is that the order book has ticked up. And we know we can’t trust containership owners to make sensible decisions. These new orders won’t begin to be delivered until 2023 at the earliest, and I have read a few opinions that explain how the market will easily absorb them. But still…

The other thing about the containerships is that there is a real dearth of names, at least on the North American exchanges. There are only a handful of stocks with meaningful containership exposure. And a bunch of those have already chartered most of their ships out for the long-term. While this was a prudent move in the past (after 10+ years of a bear market in containership rates) it is not right now.

ESEA, DAC and ZIM are the only pure plays I see that have meaningful spot/short term exposure. NMM does as well, but it is not a pure play, because it owns dry bulk ships, and its management is basically a shit show (though I do own it anyway).

I have been posting a lot of articles on containerships on the RNO board. I am not going to go through all the details of these articles but suffice to say, the situation for shipping containers appears to be getting tighter, not looser. It reminds me a little of the wacky situation that developed in 2007 with the dry bulk market.

Just sayin….

On to dry bulk.

The dry bulk trade is a bit of a different beast. The dry bulk trade is a longer-term trade. Rates did spike, particularly for capesize vessels, but it seems to me they could go much higher for longer because the supply side is not responding.

In the short term though, the dry bulk rates are not as strong as containerships. In the case of Capesize ships, rates have pulled back quite a bit.

Q1 spot Capesize rates averaged $17,000, one of the best performances in several years while Q2 was tracking close to $30,000, a very high level only comparable to the 2000s bull market. But in the last couple of weeks capesize rates have pulled back to around $20,000 now.

But while Capesize rates have taken a breather, as you can see in the chart the smaller size ships have remained quite strong.

Capesize rates are very volatile/seasonal and so you can’t get too worked up over the volatility.

The big picture here is two-fold. First, dry bulk rates are going to depend on demand for bulk goods like iron ore, grain, coal, and metals. In this sense, the dry bulk sector actually fits a lot better with the commodity bull market thesis that I have been grappling with.

But dry bulk also has some negatives that come from that same thesis. For one, if China reduces steel production and switches away from dirtier steel production that will hurt iron ore and metallurgical coal imports. For two, over the longer term thermal coal transportation is bound to decline with stiffer carbon limits.

On the other hand, the dry bulk supply situation has not seen any increase in ships (see the above mentioned order book chart). The combination of shipyards that are full and the carbon requirements of new dry bulk vessels make placing new dry bulk orders a bit tricky. Star Bulk described it like this at the Capital Link conference:

The order book has decreased to a record low 5.7 percent of the fleet, with just5.8 million dead weight reported as firm orders between January and April. Upcoming environmental regulations and uncertainty about future propulsion has helped keep new orders under control, while shipyard capacity is quickly filling up with containership and other orders.

This is what Golden Ocean said about dry bulk on their last conference call:

It is clear that fleet growth is slowing down dramatically. In fact, we are looking at the lowest fleet growth in 30 years. At the moment, the order book is likely to stay muted. There’s a very limited amount of slots available before 2024. We see increasing prices for the assets, mainly due to steel, but also due to increased demand. And of course, availability of finance and new emissions are also keeping the order book in check.

We have a potential further catalyst as we will see the new IMO 2023 regulations enter into force. It is assessed by some that upwards 80% of the dry bulk fleet is not in compliance with the new regulations, and the easiest and cheapest way to get in compliance is by slow steaming. Therefore, we expect quite a lot of slow steaming from 2023 at a time where we are already seeing very, very few additions to the fleet.

For the next 2 to 3 years, we expect this situation to tighten even further. Demand is simply going to outpace supply until 2024

Finally, Stifel pointed out the following in a piece they did on dry bulk, titled “How High can you Go? Looking at Upside Potential in Dry Bulk Shipping”. They described how until ship owners know what the carbon rules are for their ships, they will be less likely to book new builds of dry bulk carriers than other types of large ships (like containerships and crude oil ships) because retrofitting a dry bulk ship is far harder:

Outfitting a large containership or VLCC with LNG capacity would only increase the cost of the ship by 5-10%, whereas the incremental cost for a Capesize vessel would be an extra 20% and for a Supramax it would be an extra 35%

The other nice thing about dry bulk is that, unlike containerships, there are a number of little shitco-like companies that operate in the sector and that will run up if rates are higher for longer. Grindrod is the one I bought so far, but there are others.

After today I am again cautiously optimistic that this idea is going to work out. But this is shipping so who really knows.