These last few days David Portnoy has been given a hard time on my Twitter stream. His various comments about WSB and the GameStop situation are not always accurate and often seem more than a little ironic coming from someone so rich.

But in the above clip I think he is saying something fairly insightful and something quite true.

I don’t think you can underestimate the internet.

When something goes viral, it has a power that supersedes the truth. It can scale far beyond what we think is possible.

This situation reminds me a lot of Trump. Those first few months with Trump. I remember all the people on the left trying to discredit Trump by pointing out the half-truths and the misinformation. By disparaging the people that followed him as misinformed and in need of education.

But they were missing the point. It did not matter what was true.

It is not that truth does not matter on the internet. But for long periods of time, truth can be consumed by momentum. On the internet, momentum matters the most.

I feel like that is what is happening here.

You can argue, as I see many are, that this is all going to end relatively quickly. GameStop, which is obviously a bubble, will crash like all bubbles do. The WSB guys will go away. Everything else will get back to normal.

That was my own opinion until maybe Monday or Tuesday of this week.

But then I started to recognize the momentum. There is a real momentum behind whatever this is. And I am not sure if that momentum can be stopped so easily.

This DOES NOT mean that GameStop is going to keep going up. I am NOT saying that at all. The price of GameStop is still dictated by supply and demand and that will determine where it goes.

What I am saying is that the momentum of this movement, whatever the hell this movement is, is not going to be stopped so easily.

While I still am of the mind that the XBI has broken out of a long consolidation and should have a good run ahead of it, the current rally seems to be getting long in the tooth. There has to be a correction at some point. This makes me wary of new biotech positions.

You could kinda see just how tipsy the sector was with the moves yesterday morning. When whatever happened to Gamestop happened to Gamestop and the market took a sudden nosedive, I saw most of my biotech positions drop 5% or so in what seemed like a split second.

I want to be careful about exposure. No matter how much I like a story. When I take a new position, I have resolved to sell an equal amount of another biotech(s) to keep my overall positions, as a whole, to a similar size.

I was looking at Biomerica at the beginning of last week but I had not taken a position. I thought there was no rush. Then Friday hit and the stock took off. I was like, oh shit. I clicked around trying to figure out if there was news and found out that the stock had been mentioned on RealVision in an interview with a guy named Joe Besecker.

I don’t know who that is but I do have a subscription to RealVision and so I listened to the interview. It really did not say much I did not already know but it did make me think that the stock was more likely to go up than down. In this market a mention by a well-known commentator like that could be enough.

So I added a position on Friday, even though I had to do it like 10-12% higher than it was a few days before. Oh well.

I do not really think that Biomerica has the stuff to take off in one of these crazy squeezes. There is not much in the way of short interest, and I am not sure there is any imminent news (though the FDA is reviewing their COVID antigen test, which may result in something). But it has a very interesting platform (called InFoods) that targets a very large market (IBS) and that is the reason I was digging into the stock in the first place. I don’t know if it will be an immediate winner, but it seems like there is a decent chance of winning over the medium term.

Apart from InFoods, Biomerica has a suite of diagnostic tests that aren’t all that exciting. They seem to generate about $1-$1.5 million a quarter from these tests.

But InFoods is really the story here. It is a diagnostic test that tests for food intolerance. It can determine what specific foods might be causing your IBS. For example, the result might say, no more chickpeas. It is that specific.

IBS is a huge market and the existing treatments in the market are $1 billion+ drugs.

InFoods is enrolling in a clinical endpoint trial. The enrollment is going to finish in April. The trial will finish in early H2.

A clinical endpoint trial is a trial that looks at a number of endpoints to determine which one will be the one used for the actual pivotal trial. The pivotal trial is used by the FDA to approve the test or not. InFoods is already used in Korea.

IBS is a very big market. It affects like 10% of the population. I saw an estimate from B Riley that if approved they think InFoods could rival the existing drugs in terms of revenue. This would be in the $1 billion range.

So this is just another one of those stories where there is a big market and a big upside if the trial goes well and InFoods is approved. The stock is around an $80 million market cap here so it has a long way to go if all goes well.

Notes below:

Biomerica

$5.7mm of cash

no debt

11.8mm shares outstanding at $6.60 – $70mm market cap

Series A Preferred – 571,429 outstanding, look like they are convertible at $3.50, have 5% dividend

CEO has put $300k of his own money into the stock at market prices over last 2 years – but not much of this is recent, most of it was a couple years ago

been around since 1971

develops diagnostic products for early detection of chronic diseases

sold into clinical labs and point of care, also some at home sales

their legacy platform is in vitro testing

they have a 40 product portfolio right now with 20 of those being FDA approved

analyzes blood, urine, fecal samples

looks for specific bacteria, hormones, antibodies, antigens

I think that with their existing kit they are limited in their sales because its not a full suite and NA and European point of care sales will look for a full suite of tests from the vendor

they have big competition on the basic IVD business – Abbott Laboratories, Roche Diagnostics, Becton Dickinson & Co., Siemens Healthcare of Germany, Diagnostica Stago SAS of France,

Meridian, Caliper Life Sciences, Illumina, and Thermo Fisher Scientific

so most of the sales of the existing test kits comes from research/clinical

they can also sell the full suite internationally into areas where they don’t have rigorous FDA-like approvals

but its small sales

so that is why they focus on R&D, specifically on IBS and other inflammatory diseases

are completing testing for FDA clearance of patented InFoods IBS DGT test – diagnose and treat IBS

this test allows physicians to identify specific foods (e.g., pork, milk, onions, sugar, chickpeas, etc.) for each IBS patient

would require a retest 2-3 times a year

IBS is a big market – 45mm in US

825mm people worldwide

estimated to be a $30b market

facts on IBS from twitlonger:

patients visit doctor 3x more

74% more direct healthcare costs vs. non-IBS

most believe certain foods trigger

7th most common diagnosis among patients

Current treatment

Linzess at cost of $450/month

Xifaxan cost of $1760 per month

each has side effects

those two drugs do $2b a year in revenue

Infoods would be fraction of cost of IBS drugs

would see the physician share in the revenue directly

in the 10-Q they say they think if approved, opportunity is similar to any of the major drugs for IBS

this makes it a win-win for doctors and insurers

here is list: gastrointestinal diseases, food intolerances, diabetes and certain esoteric tests

InFoods IBS DGT

designed to diagnose and treat sufferes of IBS

help physicians identify foods for each IBS patient (ie. pork, milk, onions, sugar, chickpeas, etc)

will be sold into clinic and into physician office – not really sure how this works but there are two iterations of the product, one for clinical and one for POC

they had an independent market research firm do a survey and found 90% of POC doctor would use InFoods on their patients

expect patient enrollment to be complete by end of April

this is just a clinical endpoint trial

180 patients

there are 9 endpoints – 1 of the 9 will be chosen for the pivotal trial

will provide proper endpoint for final FDA pivotal trial

endpoint trial commences after pivotal trial

has received “non-significant risk” determination from FDA

also have a diagnostic test for COVID

use blood sample, check for certain antibodies, can detect within 10 minutes

this is an antibody test though – determines if you were infected, not if you are infected

they think it will be good for vaccinations – to determine if it has worked

submitted to FDA an application to sell their ELISA COVID antibody test kit

FDA has assigned an examiner, they are actively working with FDA on this

can sell outside of US with CE Mark – which they got

have patents on InFoods for use in other indications: functional dyspepsia, Crohn’s Disease, ulcerative colitis, gastroesophageal reflux disease (“GERD”), migraine headaches, and osteoarthritis

South Korea

have agreement with Telcon for sales in SA

term is 5-years plus 2 years to obtain Korean FDA clearance

$1.25mm in milestone payments and mid-teens royalties

Telcon had also bought stock (333k shares) at 100% premium to price at the time

InFoods is already been sold here from this agreement

Team

current trial has a bunch of big name participants: Mayo Clinic, Beth Israel Deaconess Medical Center Inc., a Harvard Medical School teaching hospital, University of Texas Health Science Center at Houston, Houston Methodist and the University of Michigan

apparently have IBS expertise on board – Doug Drossman is President of ROME foundation, one of leading not for profits in gastroenterology

Drossman is chair of scientific advisory board

Drossman has ben principal in GI-related drugs with GlaxoSmithKline, Forest labs, Novartis Pharma

Edward Barnholt – chairman at KLA-Tencor, director on Ebay and Adobe

Mark Sirgo is on BoD of Salix Pharma, was instrumental in growing Salix into GI major

Q221

Net sales of $1.4mm – nothing to write home about

Burning cash at a $1.5mm per quarter clip

their clinical lab revenue is down, but phys office revenue is up a lot on a smaller base

entered agreement with UK for covid rapid test

but they have an SEC investigation ongoing which isn’t great

attained CE clearance in Europe in Jan 2020

from their 10-Q:

“This nasal swab antigen test received CE clearance on January 8, 2021, and is now available for sale in the EU. The Company has received an initial order for over $1 million of these tests and is in the process of filling this order.”

not sure if that should be $1mm or 1mm?

said they had significant increase in Asian sales in Q321 so far

Announced an ATM for $15mm a few days ago

Helicobacter pylori

they have a test for H. Pylori

called HP Detect

they said at YE 2019 study would be done in 6m

would involve 200 patients

I think it uses stool samples to identify H. Pylori

but there doesn’t seem to be much being done here

planned to utilize a 510(k) pathway clearance of the test

they said they completed patient recruitment in Sept 2020

I’m not sure what happened to this?

they also had some sort of colorectal diagnostic test that seems to have disappeared

company called Meridian has only-FDA cleared test for H. pylori

it looks like revenue from their gastrointestinal product tests, which is off-patent so there could be competition, was around $55mm in total lst year, which was down 20% yoy b/c of the patent, I did find that 2017 revenue from the H. Pylori test specifically was $30mm in 2017

so it’s a decent sized market if BMRA product is approved

I also wanted to talk about VXX for a second. I traded in some of my short index positions for a position in VXX. In this market it feels to me like the best bet against a correction is the VXX. While RWM and PSQ will go up as the market goes down, the VXX is levered to it. When I look at past market corrections, particularly the more violent ones (as I suspect this one, whenver it does come, will be), it is the VXX that has been the best place to be.

72mm shares outstanding at $22/2 for $792mm market cap – or 36mm shares – its actually an ADR where 1 ADR is 2 shares of the common

They hardly seem to be covered by anyone – Stifel and that’s it?

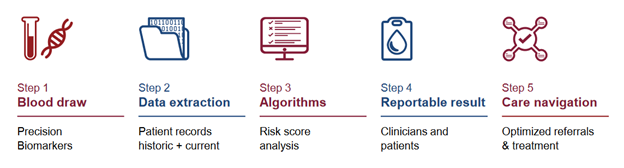

KidneyIntelX is their diagnostic tool/platform

tool for the management of Chronic Kidney Disease

currently rolling-out across the Mount Sinai hospital system

incorporates machine learning algorithm for in vitro diagnostics

early-stage prognosis of kidney disease

tool has been able to identify patients that are at high or low risk of rapid disease progression in the early stages of CKD

that means you can provide better care earlier

here are the basics of how it works:

do a blood draw

look for 3 circulating proteins

incorporate features out of the patients EMR

takes this info and put into ML algorithm and it generates a prognostic

graphically how it works:

pursuing both FDA regulated pathway and reimbursement pathway

they can test in all 50 states

expect FDA clearance in 2021

price for diagnostic set by medicare, $950/result

launch partner is Mount Sinai Disease Network – very large group

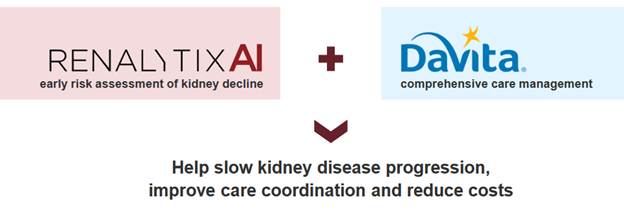

have partnership with Davita

partnership announced Jan 5/21

RNLX KidneyIntelX assay will be used to stratify patients into risk groups

Mid/high risk patients will receive care from Davita

will launch in 3 markets this year

Davita has 200,000 dialysis patients, relationships with 2,800 outpatient dialysis centers

In August they announced partnership with AstraZeneca

AstraZeneca will use the test to optimize the use of multiple therapies for Diabetic Kidney Disease (DKD) and Chronic Kidney Disease (CKD) management

will use KidneyIntelX to help optimize therapeutics under current standard care protocols.

SGLT2 inhibitor Farxiga, anemia drug Roxadustat, Lokelma

This is just first stage

before that, in June, they had announced a partnership with a top-10 global pharma company

their TAM based on diabetic kidney disease is $12b – based on 12-13mm patients with Stage 1-3 diabetic kidney disease

plan then is to expand the label to CKD – another 37mm people in the US

expand outside the US in 2023

Worldwide there is 850mm people (really?) with CKD

Costs the US $120b annually to deal with them

so this is a big TAM and I think that’s the story here, especially since they don’t have a lot of competition

estimate 50-60% of patients have Medicare or Medicare Advantage

doesn’t sound like there is any competition – see a few places that mention there is no one else developing a risk stratification tool for kidney disease

new medicare rules are disruptive – they can get medicare coverage off their FDA clearance, this is significant event, pathway for emerging diagnostic companies

they are going to benefit from this recent change in Medicare because they have received BDD:

Medicare Coverage of Innovative Technology (MCIT), which automatically issues a national coverage determination (NCD) and Medicare coverage for four years for any device or diagnostic test that had received a breakthrough device designation (BDD)

I think* this is why the stock popped early January, before this decision it was mid-2021 till you knew about the medicare reimbursement, but now it’s a done deal

Just need FDA clearance, they submitted for this in August

So they will have commercial rollout in 2021

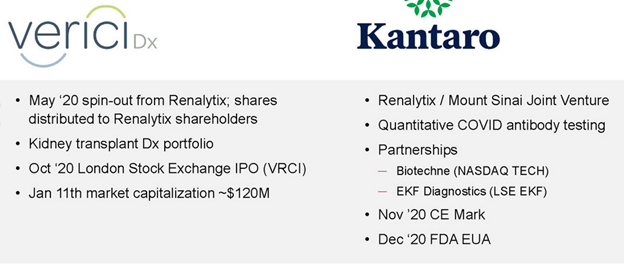

they owned a piece of a company called Verici that they spun-out, still have 25% stake in another company called Kantaro – not sure what this is worth?

This one looks pretty good to me, even in a market that leaves me skittish.

I mentioned a few posts ago that there were a few biotech microcap stocks that I had been looking at. Below I have reproduced my notes on 3 of them (NTEC, ABIO and ETTX).

These are all interesting ideas I think, though with the market where it is I cringe a little to post about them. The XBI has had quite a move. But as I’ve said before, I’m inclined to believe that the XBI is just beginning a new bull market, finally breaking out of a long consolidation. So maybe we have further to go.

More generally though, this has to be a speculative mania right? One that is, in many ways, the opposite of what the Mike Green et al passive is king proponents have professed would happen.

Many of the stocks that are going truly bonkers have very little ETF exposure. The best way to profit lately has been by chasing small individual names in the right sector and actually looking for illiquidity (ie. a low float). Another tactic has been to chase an active ETF manager – ARK. This doesn’t seem like a passive tidal wave to me. It seems like a return to active, albeit active speculation.

But it is crazy. I wrote in the comments of the last post about OEG. The only thing that stock has going for it is that it gets lumped in as “solar”. That is enough for a 4-bagger in 2 months.

I am trying to keep my exposure fairly low (though its hard when you see trains leaving the station and you are compelled to jump on – I did this with FSRV yesterday) but I am purposely leaving some speculative positions in my portfolio because, like it or not, that is what is working.

With that said, the three biotechs below have not participated much in the market run, but I think that each could pop under the right circumstances.

I mentioned in my prior post that I liked NTEC and I still do. But it is far from a perfect stock.

In fact it is mostly a failed stock – they have a drug-delivery platform (called the Accordian Platform) that has failed at pretty much every turn. This was a pick from Marc Cohodes a couple of years ago (as a long). It performed miserably after they failed their Ph3 trial for Parkinsons (though if you read the details it is more complicated than just that – they did not fail completely).

Since then NTEC and their Accordian Platform have had a go with a Novartis compound, a go with a cannabinoid compound and a go with a Merck compound. None of these have stuck.

But what is curious is that the partners keep coming – Merck signed up for another compound in the fall and GW Pharma signed up in December.

So you wonder, what exactly is so promising here? It rings a bit with a story I read about another biotech, the name of which I can’t remember, that toiled in these sort of failures but was eventually bought out at a significant premium – for its platform. So even though every indication it targeted failed, someone realized that the platform was sound, that it would eventually succeed, and that it was worth owning it before that happened.

NTEC trades at just under cash.

ABIO is another biotech laggard. This one is even more straight forward.

They have a COVID drug, which drove a crazy spike in the summer when they announced a trial. But the COVID drug angle is not really important going forward IMO.

More interesting is that before COVID, ABIO had another drug, called Gencaro, that was about to go into a Ph3 trial against chronic heart failure (HF).

HF is a huge market ($10 billion+) and ABIO is trading at less than cash.

Now this is not a perfect story. Because of COVID the Gencaro Ph3 trial, called Precision-AF, has been postponed. And you could argue, quite rightly, that Gencaro didn’t actually work that well in the Ph2 trial.

So what was the point of doing a Ph3 study on a drug that didn’t work in Ph2? Well ABIO is adept at genetically targeting their therapies, and the Ph2 study did not do that kind of targeting. But those patients who did have a specific genetic biomarker, which are a subset of high-risk patients, performed very well in Ph2. So those patients will be targeted in Ph3.

Those patients are as much as ~1/10th the market. While not as large as the whole HF market, that is still very large for a company trading at less than cash. What’s more, there is no approved alternative right now.

So those are their stories. In both cases, and to a lessor extent with CLBS and ETTX (the other two names I’ve added over the last few weeks), these are names that could have a speculative pop. Take a look at the charts. They seem quite bullish and we’ve had a couple false starts already (including yesterday). Each has a fairly low float. For NTEC in particular there is only about 4 million shares outstanding and there seems to be a couple of institutions that hold a fair number of those.

I don’t like to think that way. About spikes and floats and silly moves. But that is what this market is. You have to take what you can get.

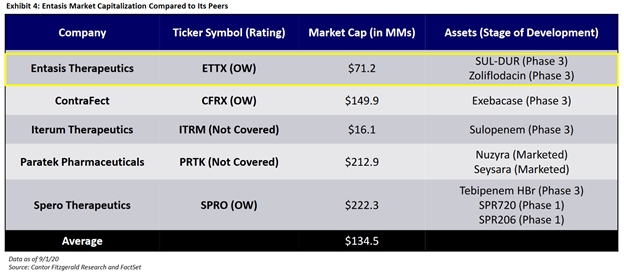

Entasis Therapeutics

this was a $5 stock back in March

$61mm of cash

35.5mm shares so $75mm market cap at $2.10

was a 2015 spinoff of AZN

focus is on precision antibiotics

they go after infections caused by multidrug resistance Gram-negative bacteria

it’s a platform! Has produced a pipeline of product candidates

has 2 ph3 trials against high-priority pathogens

SUL-DUR – sulbactum-durlobactum

will have Ph3 readout on SUL-DUR in 20201 – targets Acinetobacter – also called CRAB

resistant CRAB rates in US are 40-50% and 90% in parts of Europe/Asia

really high mortality of 50%

SUL-DUR is a beta-lactamase inhibitor

has broad Class D beta-lactamase coverage, essential for CRAB

well tolerated in Ph2 and in three Ph1 trials

Ph3 trial ongoing – called ATTACK

can market SUL-DUR with 15-20 rep salesforce because CRAB is found in targeted settings:

300 large ICUs, 200 transplant/burn/cancer centers, outpatient LTACSs and Infusion centers

would replace colistin and polypharmacy in CRAB

can point to better efficacy, lower cost, safety

CRAB TAM is $1b

also have royalty and milestones that offset cost – so they don’t own 100%?

Ph3 data on zoliflodacin in 2022 – targets N. gonorrhoeae

oral application

is resistance to existing drug called Intramuscular ceftriaxone

87mm cases a year, grows at 10%

Ph2 showed efficacy in 47/47 patients

they started Ph3 in Sept 2019

two other early stage programs – ETX0282CPDP against MDR UTIs and ETX0462 against pseudomonas aeruginosa

cheap compared to competition:

iterum has actually come up a lot since this – it trades at $1.23 for $60mm market cap, $90mm EV

Intec Pharma

$17mm of cash

4mm shares at $4 for $16mm market cap

seems to be burning $3-4mm of cash a quarter

its a platform!

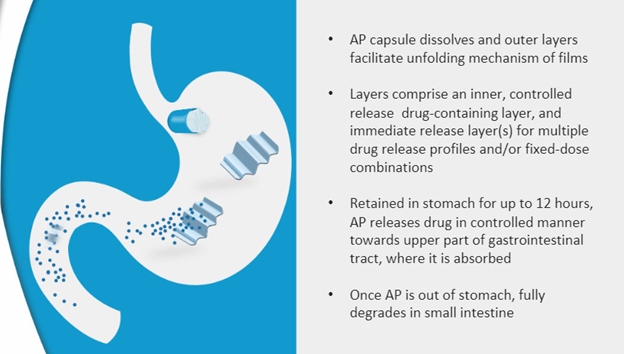

they develop drugs based on their accordian pill platform

this is an oral drug delivery system

they expect it to A. improve efficacy, B. improve safety of existing drugs via “efficient gastric retention” – so it is digested better, gets in the system better

it uses a sort of folding structure that lets the drug be released as the accordian structure unfolds:

then the accordian goes into small intestine and degrades

AP-CD/LD:

most advanced drug is Carbidopa/Levodopa – developed for Parkinsons

so this is where the shit hit the fan

announced Ph3 results in July 2019 – Accordance Study

did not meet endpoints

they call it numerically superior but not statistically superior – “not a statistically significant reduction of OFF time)

they also say this, which I’m not sure what to make of:

In preliminary review, AP-CD/LD provided meaningful reduction in OFF time for those patients who were dosed at 1.6 to 2.0X IR-CD/LD dose

I believe though that they are attributing it to sub-optimal dosing, but sounds like they are saying dosing comp has to be close to 2:1

did provide treatment, did not demonstrate statistical significance over the existing CD/LD formulation – an immediate release pill

also wasn’t any better tolerated

so it basically didn’t work any better

it did meet endpoint in Ph2 trial back in Feb 2019

they are looking for a partner here to redo (??) the ph3

Cannabinoids

initiated 2 clinical development programs

formulating and testing THC and CBD for various pain indications

their AP-cannabinoids should A. extend absoroption phase, give more consistent level of cannabinoid

will address problems with cannabinoid delivery such as: A. short duration, delayed onset, variable dose

did Ph1 trial in March 2017 – showed that it was safe and did show better exposure

but follow-up in Dec 2018 did not meet their expectations

Novartis

developed AP version of proprietary Novartis compound

they went thru invitro with this, then a human PK study

In Dec 2019 Novartis dropped them

Merck

in May they announced collaboration with Merck – this one went thru in vitro, met endpoint but is not going further

in Oct entered second research agreement with Merck for new compound

GW Pharma

entered into agreement in Dec

explore AP with undisclosed partner

basically no details disclosed here

Arca Biopharma

$51mm of cash

no debt

9.3mm shares outstanding at $4.50 for market cap of $42mm

they aren’t burning much cash, $1.5mm a quarter

develops genetically targeted therapies for cardiovascular disease

its a platform!

they have a COVID treatment called AB201

initiating Ph2 trial in Q420

is an inhibitor of something called tissue factor

tissue factor is a receptor, it is a coagulation pathway

in COVID you get overactivation of coagulation and immune response

the idea is that this is related to the TF pathways, so if you can restrict those you can stop the response

not just COVID – it has shown to prevent coagulation disorder from Ebola and Marburg virus

could be used with other antivirals

they think it would have a broader spectrum for other coronoaviruses and RNA viruses beyond just COVID

the Ph2 will be on 100 patients, then do a Ph3 with 450 patients (if there are that many by that time?)

was originally developed as a anticoagulant

they did a Ph1 and Ph2 study using it in thrombosis and it was safe and had efficacy

also have a molecule called Gencaro, used for chronic heart failure

have a trial on hold because of COVID – called Precision-AF

they had Gencaro in a Ph3 with HF patients – say that it improved mortality, hospitalization

published the Ph2b trial, called Genetic-AF in Journal of American Cardiology in May 2019

the result of the Ph2b was for them to target a subset of patients with high “left ventricular ejection fraction” and specific genotype in the Ph3, would enroll 400 patients

it seems like what happened is the drug didn’t really work any better over the broad population, but it did over a subset with genetically-defined HF and a severe case of it

so they can move forward with Ph3 targeting those patients

HF is a huge market – $12.5b in total, while for the subset for Gencaro would be $500mm to $800mm

third drug is AB171, genetically targeted treatment of chronic heart failure and peripheral arterial disease