Out with the Old, In with the New: Arcan Resources and Reliable Energy

Updated: I mistakenly stated that Arcan had spent $40M on the Stimsol purchase. It was $24M. I got my original information from a Scotia report, which read: we note ~$40M of the uptick was associated with the purchase of StimSol and for land. I mistakenly read this as $40M for Stimsol. I also sleepily referred to Stimsol as a frac fluid producer when of course they produce acidizing chemicals and solvents for de-waxing.

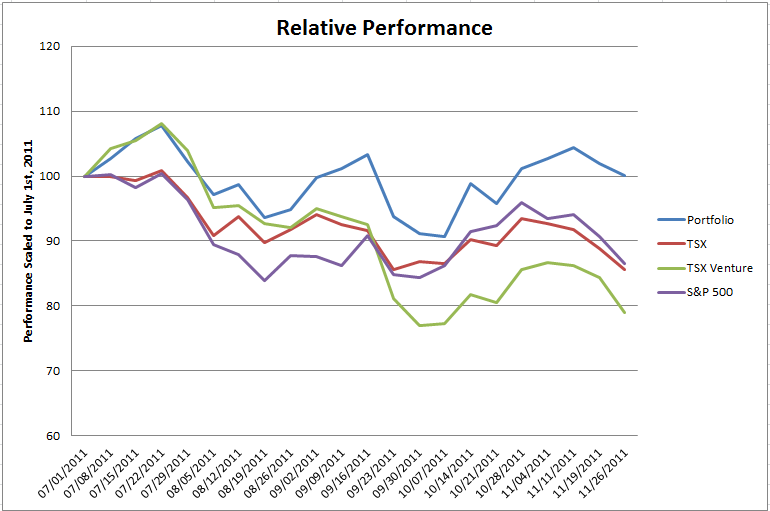

On Monday in the mid afternoon Arcan released third quarter results that I was less than impressed with. I was lucky enough to receive a google alert on the earnings release before the market fully reacted. I quickly halved my stake in Arcan in my on-line portfolio.

As I wrote on the weekend, in my real portfolio I had already substantially sold down my position. With the release of the quarter I sold more, dropping it to a rather miniscule 1% weighting. With the stock is trading in the mid-4’s two days later it appears to have been the right thing to do.

Was the quarter that bad? On the face of it, the production numbers were ok. Arcan produced 3,680boe/d in the third quarter. This was somewhat disappointing since the company had stated as far back as July 20th that they were producing 4,400boe/d. Growth is trending upwards, but the company really needs hit their exit guidance of 6,000boe/d to prove to the market that they have built a solid base to grow off of.

And while the company provided 4th quarter guidance of between 4,600boe/d and 4,800boe/d and exit guidance of 6,000boe/d, they did not give an estimate of current production. I always wonder about this. While it is not necessary for a company to provide a current production number, you have to think that if they don’t it isn’t because they have good news to share.

Overshadowing the production figures were the 3rd quarter capital expenditures by the company. Arcan spent a rather extraordinary $87M in the quarter. This is far and above the already high levels of CAPEX that the company spent in the previous 2 quarters. It is also far and above its cash flow. Now $24M of this capital was spent buying Stimsol, a maker of the acidizing blend that Arcan uses. But even subtracting out that sale, Arcan still spent almost $63M of capital, or 5x its current cash flow.

Given the future capital expenditures alluded to in the quarters report (road building, a pipeline from Ethel, remediation of the existing pipeline at Morse Unit, waterflood at Ethel), one has to expect this trend to continue going forward. To be fair though, the recent debt and equity offering the company made does give them the money to fund these expenditures.

While CAPEX went up, netbacks came down. Netbacks in the quarter were $41.90, versus $55 in the second quarter. Of course much of this can be attributed to the Swan Hills fires in the summer (the company said this amounted to $10-$15/bbl) which was a one-time cost, but in addition at least some of the increase is attributable to Ethel production, which right now is being shipped by truck to the Morse Unit. The situation is explained by the company in the clip below, along with an ETA of the first quarter of 2012.

Arcan estimates a significant reduction in operating expenses in the first quarter of 2012 due to a number of activities which are currently underway. These activities include completion of the construction of a high grade road system that connects the DM2 through Arcan’s Ethel property into Morse River, the commencement of pipeline infrastructure along the new road system backbone that will allow production in Ethel to flow to the DM2 oil facility, and the construction of pipeline infrastructure to facilitate water injection in the Ethel area. Arcan is also working on resolving issues with the clean oil pipeline which flows from the DM2.

Arcan is still on the right path, they are just moving more slowly down it than I would like to see. The problem with moving more slowly is that Arcan is valued quite highly compared to its peers, so slower than expected growth leaves lots of room for downside questioning.

All flowing boe numbers are based on the latest production estimate provided by the company.

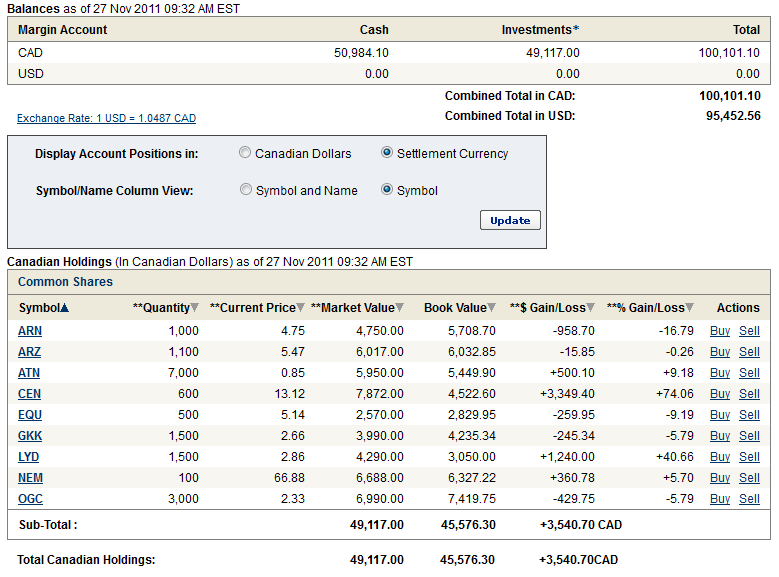

With some of the proceeds of Arcan I bought a position in Reliable Energy.

Reliable Energy released their 3rd quarter results on Tuesday morning. While Arcan produced a decent production increase while spending a lot of capital, Reliable showed similar production increases (production has almost doubled since the 3rd quarter), while spending more closely in line with their means.

Moreover, a look at cash flow shows that Reliable will be more able to spend within their means in the coming quarters. Reliable generated $3.8M of cash flow in the 3rd quarter with a netback of $65/bbl. As of their latest production estimate they are now producing about 500bbl/d more than they averaged in Q3. At $60/bbl netback that would work out to about $3M additional per quarter in cash flow. That puts the yearly cash flow somewhere around (maybe slightly above) the $25M per year range. The capex budget for 2011 is $25M.

Midway, Arcan and others have had to spend well beyond their means to grow production. In some environments that is not a deterrent. In our current liquidity strained environment, it is. Reliable looks to be in a better position to do that, at least in the short term.

The other important consideration with Reliable is that they are beginning to ramp up into the 2nd of 3 consecutive quarters of drilling. Reliable basically moves to the sidelines during spring break up, and so they tend to see decent production gains through the winter months as they spend a disporportionate amount of their yearly CAPEX budget during that time. The drilling and completions in Q3 is responsible for the production increases so far in the 4th quarter. With a little luck it will continue going forward.

The company trades at about half of what Arcan does on a flowing basis. At $47,000/flowing boe (see the above chart where I compared flowing boe numbers for a number of juniors) the company is reasonably cheap compared to its peers, especially considering they are producing high netback light oil. On a reserves basis the company trades at close to its 2010 NPV10 of $0.19.

I suspect when their 2011 reserves report comes out (likely not until late in the first quarter) it will show a significant increase over the 2010 reserves. The 2010 reserve report (available on Sedar) gave them 800,000bbl of undeveloped reserves and 400,000 of developed producing reserves. The 400,000bbl was likely entirely vertical drills. The undeveloped works out to the equivalent of about 8-10 horizontal locations depending on the evaluators productivity per well guess. In the next report that number should go up pretty substantially. Up to the end of the 3rd quarter Reliable had drilled 10 successful hz wells this year so offsets alone should double that number.

In all, Reliable Energy looks to me like a better bet for near term price appreciation than Arcan does.