Biotechs are Awful and Caribou Biosciences Looks Reasonable

My foray into gene editing has been more miss than hit so far. I bought a few of these stocks four or so weeks ago and have subsequently watched them crumble along with the rest of biotech.

As of Friday I had positions in CRISPR Therapeutics and Intellia Therapeutics. These positions are both underwater now, by 15% and 10% respectively.

More generally, it has been a tough market to buy biotech stocks. This is definitely the pain trade right now. A pain trade is buying something that is clearly out of favor and has zero love with the expectation that this will change and it may change quickly. Energy has been the best example of a pain trade over the last few years. You buy energy stocks because they are hated and then every once in a while they have a barn-burning rally and you make a killing.

Biotechs are definitely loading up on the pain right now. That pain is accentuated by the fact that the market keeps going up as they go down. The only biotechs that are not going down are… is Moderna. I own some Moderna, so that is a nice respite from the others.

But back to gene editing. I lightened up a little on a few of my gene editing names Friday afternoon once I realized that there was a new name that I think looks better than the others.

Caribou Biosciences went public on Friday about 2 hours after the market opened.

I did not realize Caribou was about to go public. I have been on vacation and missed the news. So about 30 minutes before the market closed Friday after seeing a tweet on Caribou, I was scrambling to see if I wanted to own the stock.

One thing about spending the last month or so trying to understand gene editing is that while it has not translated into making me a good picker of these stocks, it has at least given me a decent understanding of the landscape.

And if I am right, Caribou is mispriced compared to its more established (as stocks, not as a company) peers.

At its closing price on Friday Caribou traded at a market cap of $950mm. They have $425mm of cash on hand. That compares to CRSP and NTLA at around $10 billion, BEAM at $6.5 billion, EDIT at $2.7 billion, VERV at $2.4 billion and GRPH at $1.5 billion.

Now CRSP and NTLA have programs that have already had some positive Ph1 results. That is why they have the highest valuations. BEAM does a newer version of gene editing called base editing that may turn out to be superior to Cas9 editing, and that is why BEAM gets the relatively high valuation given that they are pretty early on (they don’t have a therapy in human trials just yet). The rest have points for and against but all are very early stage.

In general, at least a ~$2 billion valuation seems to be the norm for these gene editing CRISPR stocks. You could certainly argue they are all overvalued – in fact what I see is most traditional biotech investors are pretty put-off by the valuations these stocks get given the point where their therapies are in development (either Ph1 or pre-clinical) – but I think its tougher to argue why Caribou should be at $500 million net of cash while these others all trade at multiples of that.

Why? Well for one, Caribou holds a lot of the CRISPR IP. If you read the Intellia 10-K, they say they license much of their IP from Caribou. In fact, if I am understanding the disclosure correctly, Caribou will get a mid-single digit royalty on any product Intellia markets that uses the Caribou IP.

Caribou has the IP because this is Jennifer Doudna’s original company. Caribou was created shortly after Doudna and Emmanuelle Charpentier discovered CRISPR Cas-9. Doudna is still with the company heading up their scientific advisory committee. Their CEO, Rachel Haurwitz, was with Doudna as a research assistant since the beginning and has been CEO since Caribou was established.

It seems like a pretty all-star-like team here. They are full of the original discoverers and they own the underlying IP (though there are ongoing patent battles with the IP so that is something that could change, for the better or the worse).

The biggest knock that I have seen made against Caribou is that they are going after different indications than the rest of the group. Pretty much all the CRISPR names I’ve mentioned are going after the kinda “lowest-hanging fruit”. That would be stuff like sickle cell disease and other genetic blood disorders, liver diseases, and eye diseases. There are a bunch of reasons why CRISPR editing is most conducive to these targets, but they are.

Caribou is going for the big kahuna. They are going after cancer.

There are a couple things about targeting cancer that could be construed as negative.

First of all, its a tough nut to crack. Something like sickle cell disease is relatively simple because we know that it is caused by a particular gene mutation and we know that CRISPR techniques can knock-out gene mutations. So its a fairly low bar (I mean intuitively, not in practice) to conclude that if you can get the process down right, you can knock out the genes causing the mutation and prevent the disease.

Cancer is of course very complicated. What’s more, Caribou is not doing something totally unique with their approach. Caribou is using Cas9 and their own, proprietary (I think) Cas12a editing techniques to edit CAR-T cells that are used in cancer therapies.

(Note: I don’t believe that Cas12a editing is done by any of the other public gene editing companies. I am trying to learn more about Cas12a editing. FWIW Caribou says that its more precise edits than Cas9.)

Using CAR-T cells isn’t at all new. But editing them in the way Caribou is doing is new. The specific edits Caribou is making to the CAR-T cells are new, including the “first clinical-stage allogeneic anti-CD19 CAR-T cell therapy withPD-1 removed from the CAR-T cell surface by a genome-edited knockout”.

Planning to use allogeneic cells is also new. Allogeneic means using cells from a healthy donor, rather than harvesting cells of the patient. This has the potential to make the manufacturing of a therapy a much easier and consistent process. From what I have read, the limitation of using patient cells has been a stumbling block in getting CAR-T therapies used so far.

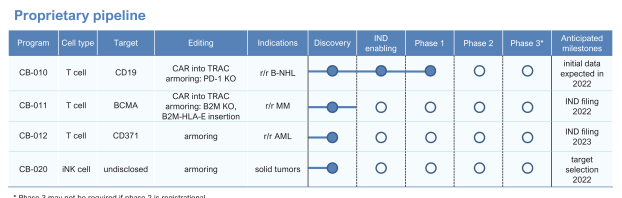

Caribou’s lead therapy candidate, CB-010, has just started its Ph1 trial. They recently dosed their first patient in the trial and expect results in early 2022.

CB-010 will be followed up by 3 other therapy candidates:

Worth noting is that the CB-010 CAR-T edits are being done by Cas9 editing. The following 3 candidates will use Cas12a.

So anyway, going after cancer is maybe a reason that Caribou is not valued like the other gene-editing names. But you could also argue the opposite. Cancer is a huge TAM and if Caribou shows some success with CB-010 the market is going to flip on its head and look at Caribou as the leader in new gene edited therapies against cancer. Which would obviously be massive.

My point in this very quickly written post is not to try to parse the positives and negatives with a fine tooth comb. It is simply to look at the positives and negatives and conclude (tentatively at least) that Caribou is probably as well positioned as most of these other gene editing companies, and yet the stock price is less than half of their valuation.

PS –

In addition to the gene editing pain, I have taken on additional pain by buying or adding to a number of biotech positions in the last couple days. I bought some BIOC on my expectation that their COVID testing business may last longer than many have anticipated. I bought some Lyra because it is again trading close to cash. And I bought back my EIGR position because it again has dropped below $8 and they have a Ph3 Covid trial that should readout soon and that could be more relevant with the Delta variant gaining steam.

On the other hand, if biotechs go from bad to worse to off the charts then I am going to feel pain this upcoming week.