Yet another airline stock: Transat AT

I made a number of portfolio changes today, reducing positions in a few stocks that haven’t been working out as I had hoped. I sold the last of Pacific Ethanol, sold out of Syncora and reduced my position in Chipmos. In part I made these changes to raise cash because I have been adding to my position in Transat A.T.

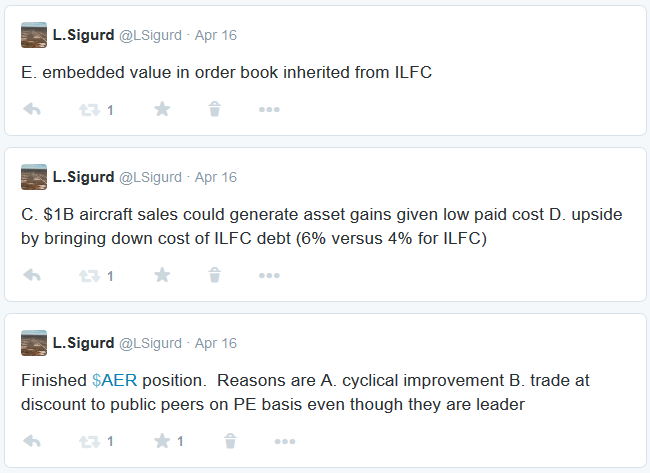

I first bought Transat A.T (TRZ.B) on March 19th and have added to it a few times since then. I made the following tweets at the time (read from bottom to top):

What they do

Transat provides both chartered and scheduled flights originating in Canada and France. They operate three main service routes.

- Charter flights to Sun destinations for Canadian vacationers

- Transatlantic flights from Canada to Europe

- Vacation destination flights in France