Week 366: The Wishy Washy Portfolio

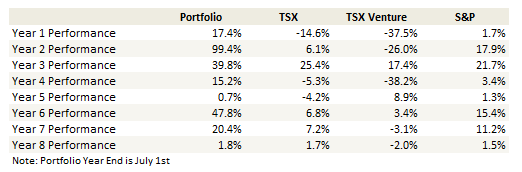

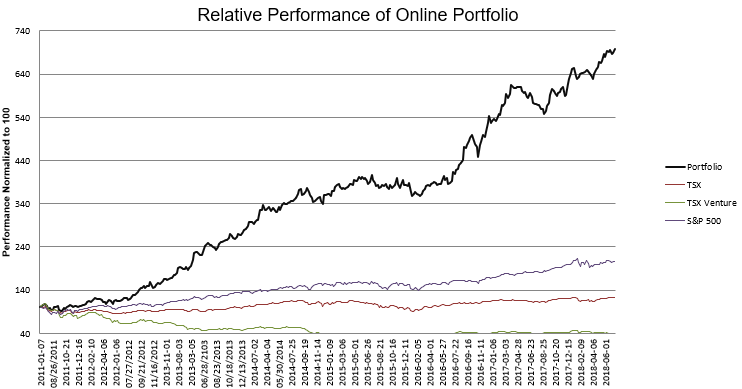

Portfolio Performance

Thoughts and Review

I’ve done a lot of flip-flopping over the last 6 weeks. I couldn’t get comfortable with certain oil producers, I couldn’t get comfortable with oil servicers and I couldn’t get comfortable with the copper stocks. I also owned and then sold Cameco and Energy Fuels before settling on buying the debentures for Energy Fuels.

These transactions weren’t trades. I don’t really trade in my portfolio. But I often buy into ideas that I am not completely committed to. Having a position clarifies my conviction. If I don’t have it, I’ll sell a few days later.

As it turns out it probably wasn’t a bad idea to step away from these ideas. The oil servicers, which I will talk about below, have done little. Copper stocks, which I talked about here, have done even worse. Cameco has floundered.

What I have added and stuck with over the last 6 weeks is RumbleOn and Smith Micro, both of which I have already talked about, GeoPark, which I’ll talk about another time, and Overstock, which I’ll talk about right now.

Overstock

When I first wrote about blockchain I said I found it interesting because: “it’s a way of dis-embodying trust into technology. The middle man disappears. The skim shrinks. Everyone (other then the middle man) benefits.”

Since that time crypto has gone to the moon and crashed again. While its easiest to base an opinion on the latest bitcoin price, I don’t think that is necessarily correct. I still think the premise of what blockchain promises has value. It just has to find ways of being integrated into applications that have broad usage. If I were to bet, I would say that the current lull in sentiment will pass and that blockchain will come back into vogue in some new form relatively soon.

So let’s talk about Overstock.

I bought the stock two weeks ago after tZero announced that they had received a $100 million letter of intent (LOI) from GSR Capital.

Like most things with Overstock, its a fuzzy data point. First, its an LOI, which doesn’t really mean anything is certain. Juniors on the Canadian venture exchange love to use LOI’s to put out big numbers and generate big hype (coincidentally I will talk about a situation like that shortly!). The deals often don’t amount to anything.

Second, GSR Capital looks a bit sketchy. This post from CoBH kind of makes that point. Of course you can dig in the other direction and find less bearish takes on what GSR is doing.

I’ve always thought of Overstock as a stock that has an asset value with a huge standard deviation. You can create a legitimate case that the stock is worth $30 or $80. There is that much uncertainty about outcomes.

It’s all about buying it at the right place within that band.

Being able to buy the stock in the low $30’s (I got a little at $31, more at $32 and the rest at $33), especially after there was incrementally positive news, seemed like a reasonable proposition to me.

The GSR investment, if it is followed through, represents the first time in a while that something Byrnes has hinted at actually happened. So I’m getting it at the bottom of the band and with a positive data point to boot.

When I sold Overstock in January and February it was because the projections Byrne had made a quarter before were not coming to fruition.

- He had said the stock lending platform had billions of inventory and would start making money shortly. But in the tZero disclosures in December there was no mention of the stock platform at all!

- He had talked about partners knocking at the door. But all that materialized was Siebert and a couple of other tiny acquisitions.

- He talked about the mysterious man in the room and one other big opportunity he had. This turned out to be De Soto, a very interesting idea but something that he himself has said that he only “thinks” can make money.

Byrne also talked at length about the Asian money that was interested in tZero. That was another strike out. Until the GSR investment. Now its not. So something actually panned out.

Its clear that the advanced state of tZero that was described at the end of last year was exaggerated. It also seems likely to me that Byrne was not entirely aware of the state of the software. Witness that the CEO of tZERO was replaced by Saum Noursalehi, who was moved over there to add a “Silicon Valley” mindset to tZero:

But I think this is going to become an innovation game. I think that by putting Saum there, I mean he’s extraordinarily able as an executive anyway, but in terms of managing innovation, Saum and I have a decade’s history of working together on [O lab] And other things that have changed our company and I don’t think anyone I’ve met in New York was going to be able to compete with what I know Saum has in mind.

tZero was supposed to offer a stock lending platform and would be on-loading inventory they had accumulated. That didn’t happen and they are now in the business of licensing it out. The software also probably wasn’t all that functional; on the first quarter call Noursalehi said they were (only now) building out the functionality to allow you to carry the digital locate receipts for intra-day periods. That this wasn’t available in the original software is odd.

They are also only in the process of building out the token lending platform, which is to say there is nothing operational yet (one of the first major red flag I mentioned from the tZERO memorandum last December was that the security token trading system was described as something that still needed to be built!).

Of course the sale of the e-commerce platform, which was supposed to be done by February-March, is ongoing and now more of a “souffle”.

So there are lots of negative spins you can make here. On the other hand they are forging ahead with the tZero platforms, they have over $250 million of cash on the balance sheet and another $320 million from the tZero token offering (if you count GSR and all the executed SAFEs), and the sale of e-comm is still ongoing, so there is the potential for a positive resolution there.

There is also the initiatives to transform e-comm into something that is growing. While these are still in the early stages it seems to be working. So that’s just another probability to add to the list.

Most importantly, at a little over $30 buck a lot less of the positive potential is priced into the stock then at $80.

Look, Overstock is what it is: a stock with a lot of optionality, a lot of uncertainty, operating in an brand new industry that I don’t think any of us know how it will play out in the next 5 years.

So speculators pretend that the price of bitcoin is somehow a proxy for the state of blockchain. It’s probably not. I didn’t buy Overstock as a quick trade to capture a short pop on speculation of GSR. I actually think at $33 it represented a fair value for all the risks and rewards. So I’ll see wait for the next data point how and evaluate from there.

Wanting to Buy Oil Services but can’t

I’m not a trader. When I get into a stock its with the intent of sticking with it for 6, 12 or 18 months or however long I need to in order for the idea to play out.

So when you see me in and out of a stock in a short time frame it usually has nothing to do with trading. Its just indecision.

Such has been the case with the oil services stocks where I’ve been in, out, back in and back out again.

What’s going on? I’m being torn between two sides.

The bull side is simply this: oil is up, growth in production needs to come from the US, and oil servicers should benefit. The stocks are extremely cheap if their businesses are on a growth path.

The bear side is that all of the on-shore servicers are exposed to the Permian, Permian capacity constraints are going to kick in this summer, and volume and pricing of drilling and completion services are going to get squeezed.

I should probably just walk away from the idea. The stocks don’t act well. Considering that this should be a bull market, the action is even worse.

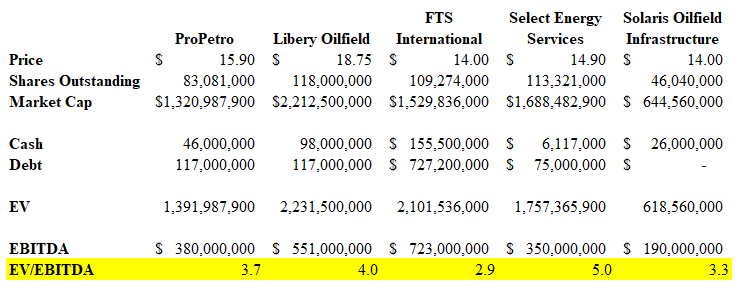

What keeps me interested is just the absolute valuations. Below are 5 companies with average EBITDA multiples for 2018 and 2019 (these prices are from a week or so ago but I don’t think anything has moved much since then so I haven’t updated them).

Seems cheap? That’s what I thought.

Seems cheap? That’s what I thought.

But when I buy any of these stocks, all I do is fret about them.

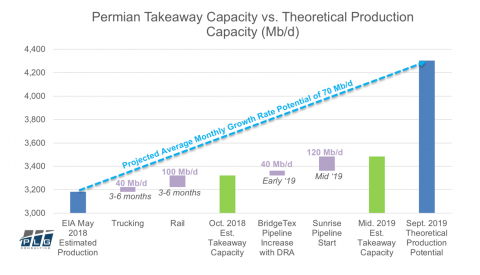

The problem is the Permian. RBN put out a really good piece describing how the infrastructure bottleneck in the Permian is likely to play out, and what the alternatives now. Unfortunately it’s behind a pay wall.

The issue is that there isn’t enough pipeline capacity to get the oil out and new pipeline capacity won’t be finished until the second half of next year. So you have about a year of constrained takeaway.

Source: PLG Consulting

As RBN pointed out the alternatives to pipelines have their own constraints. Rail can only carry as much as the available tankers and loading capacity. This is less than 100 thousand barrels a day.

Trucking is theoretically unlimited but the logistics of bringing in trucks and truckers caps it in reality. A single truck can carry about 180 barrels a day. So for every 10,000 barrels a day of production you need to add 100 to 150 trucks and drivers.

The Permian accounts for about 50% of activity in the United States onshore. As an oil servicing business its hard to avoid the Permian. Exposure of the companies I’ve looked at varies from 30-60%. Solaris has about 60% of their fleet in the Permian.

But just how much of a hit will these companies take? That is the other big question.

According to the company’s themselves, they are insulated. They talk up their long-term contracts, how they are dealing with the stronger operators in the region, and how these operators have secured takeaway capacity and hedged their exposure and thus will be able to keep drilling.

But are they really? I don’t trust them. We won’t really know until the second quarter calls start hitting and they have to fess up about the state of their operation.

So what do you do?

For now I’m back out. I think.

The only exceptions are a couple of non-Permian related servicers that I own. Cathedral Energy, which I don’t believe has as much exposure to the Permian (though they do have some), and Energy Services of America, which is a pipeline builder in the Marcellus/Utica that has a host of their own problems but the Permian is not one of them.

RumbleOn

I was worried that my lead touch was failing me. I am resigned to the fact that I take positions in stocks where I will have to endure months of it doing nothing or going down before it actually begins to move as I suspect it should.

RumbleOn moved as soon as I bought it and before I was even able to get a write-up out.

<sarcasm>Fortunately</sarcasm>, that situation was rectified as the company offered a little over 2 million shares at $6.05.

In retrospect, the entire move to the mid-$7’s and back to $6 was probably bogus. I don’t understand all the in’s and out’s of these share offerings enough to be able to tell you why, but I’ve been held hostage to enough of them to know that this sort of activity seems to be part of the process.

So what do I think of the move to raise cash? I don’t see it as a big deal either way. I had thought they might use their recently created credit facility to bridge the gap to profitability. I figured given the management holdings they’d be reluctant to dilute. But whatever. If the business works the 2 million shares is not going to matter much to where the price goes.

I used the opportunity to add more.

Mission Ready

I have been patiently waiting for 9 months for something to happen with Mission Ready. I haven’t said much (anything?) about the company since I wrote about them last September. That is because essentially nothing has happened.

Nine months with no news (after announcing a massive LOI) is pretty ridiculous. There is a valid argument that I should have walked away. But something about the company made me think its more than just a hyped up press release with nothing behind it. For sure, the stock price has held up incredibly well since September considering that nothing has happened. So I have stuck it out.

Now maybe we get some news? The stock is halted.

Is this the big one? And is the big one a rocket or a bomb? No idea. But I am excited to find out.

Gold Stocks

Back in May when I last talked about the gold stocks I own I wrote:

…these stocks are more of a play on sentiment. I think all I really need on the commodity side is for gold not to crash.

I should have knocked on wood.

That said, the gold stocks I own have held up pretty well. Wesdome is up a lot. Gran Colombia is up a little (albeit it was up a lot and has given back most of those gains). Roxgold is roughly flat, as is Golden Star. Jaguar Mining is down a bit. Overall I’m up even as the price of gold is down over $100.

I still like all of these names. But whereas my original thesis on each name was based on the micro – I simply thought each stock was cheap given its cash flow and exploration prospects, I am actually getting more bullish on the macro. Even as gold has fallen.

This tariff thing is becoming the shit show I thought it would be. I expect further escalation before any agreement.

There are a lot of US based commentators that think other countries will be rational and give in to their demands. I really don’t buy that. I think its got to get worse before that happens.

I’m Canadian. So I am on the other side of the tariffs being introduced. My visceral reaction when I hear of a new tariff being introduced against Canada or I hear Trump make some inaccurate or at least unbalanced comment about Canadian subsidies, is “screw them – I would rather go into a recession than give in to that BS”.

Now you might say that is an irrational response, that it is not reasonable, and point out all the reasons it is wrong. Sure is. Doesn’t matter.

If that’s my response, I bet that is also the response of a lot of other Canadians, and of a lot of other citizens of other countries. We would rather see our government’s stand up for us then be pushed around.

You don’t think that all the other foreign leaders don’t realize that? Look at what Harper just said: that Trudeau is manipulating the NAFTA negotiations because he can gain political points. Maybe, maybe not. It wouldn’t be that surprising. Does Trudeau get more votes next year if he can say he stood up for Canadians or if he says he buckled under because it was the right thing to do? You think the European leaders look stronger if they give into US demands? Same thing for China.

My point is we are all going to stand up for ourselves. It won’t be until we all see (including the US) what it feels like to be sinking in the boat that we reconsider. Right now this is a matter of principle and what is rational is irrelevant.

I expect the trade war to escalate. And gold to eventually start going up.

DropCar, Sonoma

I sold out of both DropCar and Sonoma Pharmaceuticals.

DropCar has been a disaster. When I wrote the stock up I said it was highly speculative, even for me. But I have to admit I didn’t expect it to crash and burn so quickly.

I don’t like selling a stock just because its just dropping. If there is a negative data point that comes out, then sure I’ll dump it in a heart beat. But random drops are frustrating and I often will hold through them.

But the DropCar collapse was too much and I reduced my position in April. That turned out to be a good idea. I sold the rest of the stock after the first quarter conference call. It was just such a bad call.

During the Q&A they were asked about gross margins. They could have provided a long-term speculative answer, talking about how margins are being pressured because of their growth and the drivers they are hiring, and how long term they expect margins to settle in the mid-teens or low twenties.

They didn’t have to be specific, they just had to spin it positively. Instead they basically deferred the question. We aren’t going to talk about that. You can maybe get away with that answer when things are going well, but when you just announced a negative gross margin quarter you just can’t.

Anyways, I sold.

The other stock I sold was Sonoma Pharmaceuticals. Sonoma had what was just a really bad quarter. Sonoma had been growing consistently for a number of quarters and much of my thesis here was simply a continuation of that trend. That didn’t happen.

The problem is if they don’t grow they are going to have to raise cash again. They have a limited run way. The company kind of implied on the call that this was a blip, but it wasn’t enough to convince me with certainty. So I figured I better sell and wait to see what the next quarter brings. If they are back on track, I will add it back. There is still a lot I like about the story.

Portfolio Composition

Click here for the last six weeks of trades. Note that I added Energy Fuel stock to the practice portfolio because I couldn’t add the debentures (a limitation of using the RBC practice portfolio). Also note that Atlantic Coast Financial was taken over and my shares converted but this didn’t happen in the practice portfolio (they just stay halted in the RBC practice portfolio). That’s another change I will have to manually make before the next update.

{kind=link}