Week 349: Company updates, a couple new positions but mostly sitting pat

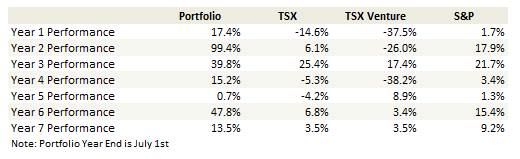

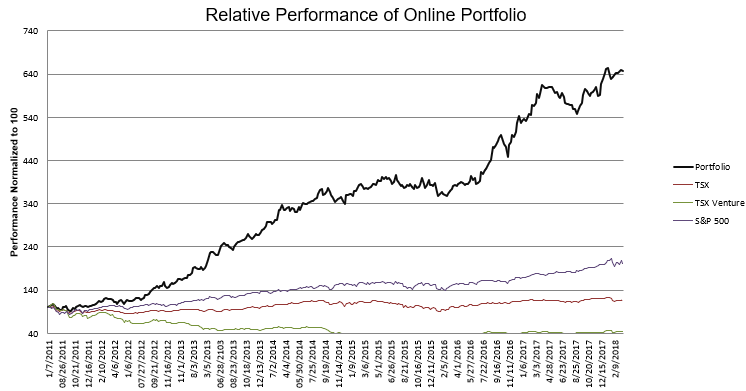

Portfolio Performance

Thoughts and Review

I’ve been slow on the updates. This is the second time in a row that its been 8 weeks between them.

I’m slow because my portfolio has been slow. I still have a high cash level. I took advantage of the stock decline in February, but not enough to have much of an impact on my results. Since then I sold down a few positions and so I’m back to a high cash level.

Portfolio Additions

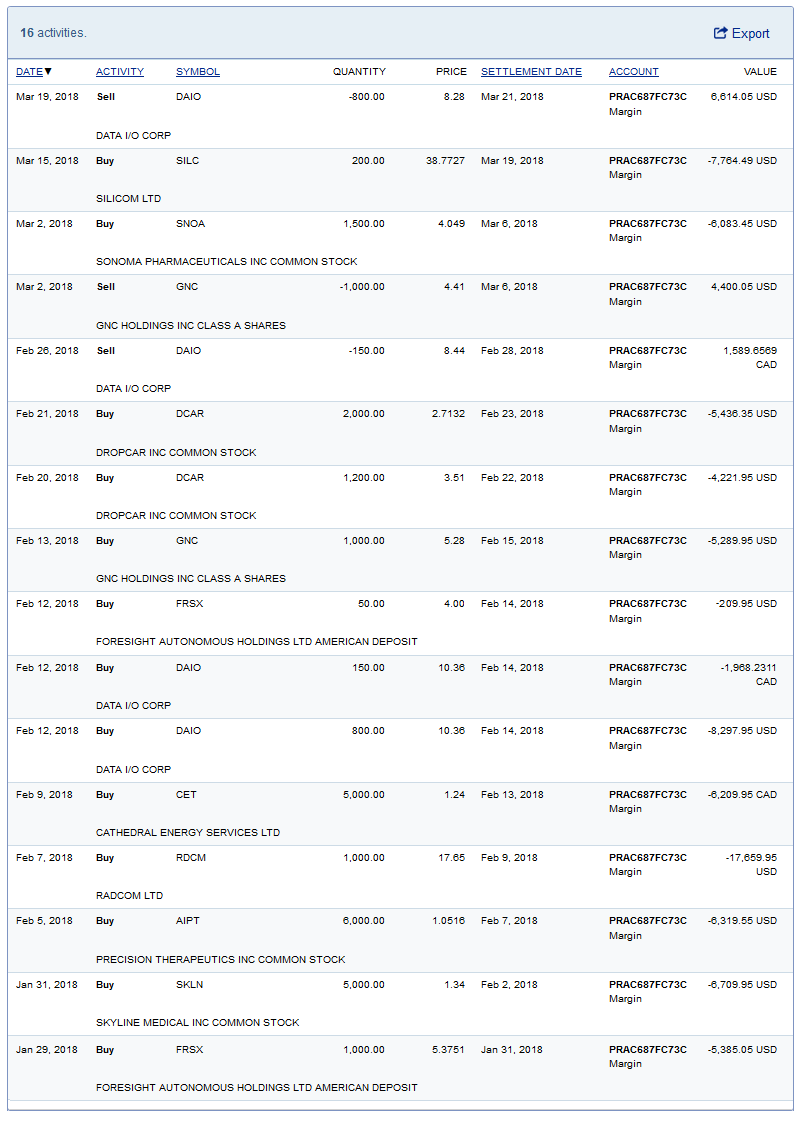

I’ve already written about my new positions in DropCar and Precision Therapeutics, as well as reestablishing a position in Radcom and Silicom.

In addition I took a position in Sonoma Pharmaceuticals and Foresight Autonomous.

I’ve got something written up about Sonoma that I will put out in a couple of days, so I’m not going to talk about them right now.

Foresight Autonomous

My position in Foresight Autonomous is small (less than 1%), so I’ll just mention the thesis briefly.

The company is developing automobile detection systems (called advanced driver automation systems or ADAS). They have had successful trials with Uniti Sweden, and three successful pilots with Chinese companies.

The stock trades at a $110 million market capitalization. That’s not really cheap but I think the potential here is significant if they can land a deal with a large car companies.

Foresight also has a 35% interest in Rail Vision. Rail Vision provides detection systems for rail systems. Rail Vision was looking to IPO last fall at a $100 million valuation.

Worth noting is that this article said that Foresight’s technology has tested better than Mobileye. Mobileye was bought out for $15 billion.

Good News from existing positions

While my portfolio has only benefited at the margins, there were a number of positive news events over the last couple of months that do bode well for the stocks I own.

Vicor gave a very positive outlook on their fourth quarter conference call. They are making progress on the 48V servers, automotive and high end power on package applications. It seems very likely that they are working with a large FPGA producer (maybe Nvidia?) for high end power converters on the the chips.

Gran Colombia is doing very well at both of their mines. They provided a February update on Tuesday. They are on track to do more than 200,000 ounces if they can keep up the mining rate from the first two months of the year.

The next day the company amended terms to the debt exchange deal. The 2018 debentures will be redeemed, not refinanced. It means more shares and less debt.

The amendment doesn’t change my opinion on the stock. With the new terms they will have about $95 million of debt and 54 million shares outstanding. It doesn’t really impact the enterprise value much, with less debt there is somewhat less leverage to the price of gold but also less interest charges.

DropCar announced they are going to be doing maintenance and cleaning on the Zipcar fleet (transport,prep, cleaning, maintenance) in New York City.

The stock only moved a little on the news but it seems pretty significant to me. Zip Car has 3,000 cars in NYC according to their website.

While I’m not sure how b2b revenues on a per car basis compare to the consumer business, 3,000 cars is a lot of cars. Compare this to the 1,500 consumer clients they have right now.

The only question is what sort of revenues do they get on a per car basis for the B2B business? I need a bit more detail from the company on this. I suspect there are a lot of investors feeling the same way.

I wasn’t thrilled to see the $6 million private placement. It conveniently gets Alpha Capital Anstalt their position back without breaching the 10% rule (its a convertible preferred sale). But I still think the business could have legs. The recent Zipcar deal suggests that is the case. So I’ll hold on.

Precision Therapeutics (formerly Skyline Medical) has been announcing all sorts of news with respect to its Helomics joint venture.

I honestly don’t know what to make of this. I bought the stock because it looked like Streamway sales were going to launch, but all the news is about precision medicine, which is maybe (??) a bigger deal, but I don’t really know.

Some have pointed to Helomics revenue being in the $8 million range (which I’m not sure if it is), and that Helomics has spent over $50 million in research over the past 5 years (which appears to be the case based on the past capital raises). If either of these points are accurate then Helomics is potentially more valuable than the single digit million valuation that Precision paid for the first 25%.

But I’m not going to lie, I don’t really understand the precision medicine area very well.

If anything, the company seems to be prioritizing the precision medicine business and I would think, given that the Streamway business is not profitable, that would put Streamway on the block. If I’m right about the value in Streamway, then my original reason for buying the stock will work out, and maybe even sooner than I had hoped.

R1 RCM reported fourth quarter results at the beginning of March. They see revenue at $850-$900 million in 2018 versus $375 million of revenue in 2017. They are expecting adjusted EBITDA of $50-$55 million this coming year.

EBITDA is going to be depressed by the continuing onboarding of Ascension, new customers Intermountain Health and Presence Health, and the Intermedix acquisition.

In 2020 once the onboarding of Ascension is complete the company expects $200 million to $250 million of EBITDA. At $7.70, which is after the big move over the last month, that puts them at a little under 7x EBITDA. That’s still not super expensive and the path to get there seems straightforward so I’m holding on for now.

Gold stocks suck right now but I am adding. In addition to Gran Colombia, I’ve added positions in Roxgold and Golden Star Resources this week. Neither is reflected in my portfolio below, which is as of the end of last week. Taken collectively, gold is my largest position right now.

My thought is simply that this trade war stuff seems to be real and and getting more so, and how is that not bullish gold and gold stocks? Meanwhile I am picking these stocks up at discounts to where they were 6-12 months ago. And we just had the takeover of Klondex at a pretty fair valuation. It seems like a decent set-up.

I sold Essential Energy this week (this was after the portfolio date so its still in the list of stocks below). I listened to their fourth quarter conference call. Its hard to get excited about their prospects. Drilling activity in Canada just isn’t coming back. I’m going to stick with names like Cathedral and Aveda that have more US exposure.

I also sold Medicure this week after the news that Prexarrtan won’t be launching on the original time line. I may be jumping the gun, after all Medicure has 3 other drug launches in the next year or so. But Prexarrtan was the first and without it I don’t see much of a catalyst for the stock in the near term.

Portfolio Composition

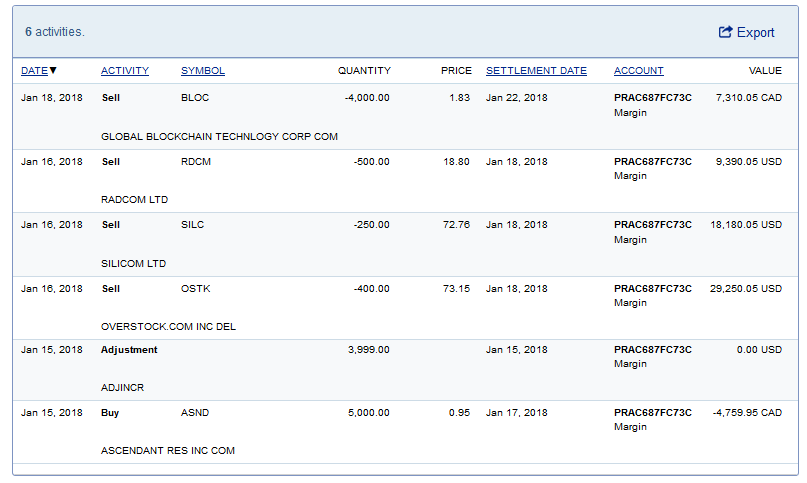

Click here for the last eight weeks of trades. NOTE: I didn’t go back far enough in my trade search. These are the trades from Jan 15th to Jan 29th that I had previously missed.

Prices below are as of Friday, March 16th.

{kind=link}

{kind=link}