Love the Illiquidity: Blue Ridge Mountain Resources

Back in June I got an old stink bid filled on Blue Ridge Mountain Resources. It took a while to fill. The stock trades on the grey markets, meaning there is no active bid and ask (at least none that I can see), the security is extremely illiquid and can go for days without trading. You can’t even access the website with their financials and presentations without getting a password from the company, which is why I haven’t written about my position until now. Recently the company uploaded a recent presentation onto their public site, which gives me the opportunity to talk about my position and refer to that.

Blue Ridge Mountain is the post-bankruptcy resurrection of Magnum Hunter Resources. I have had pretty good luck with these sort of post-bankruptcy, grey market situations. Here’s the pattern: I wait patiently to get an order filled at a good price, I wait patiently for the stock to get listed on an exchange where it can get some volume, and then I wait patientlu for it to be revalued accordingly. It doesn’t happen overnight, but more often then not it happens. Most recently, this was a successful strategy with R1 RCM (formerly Accretive Health).

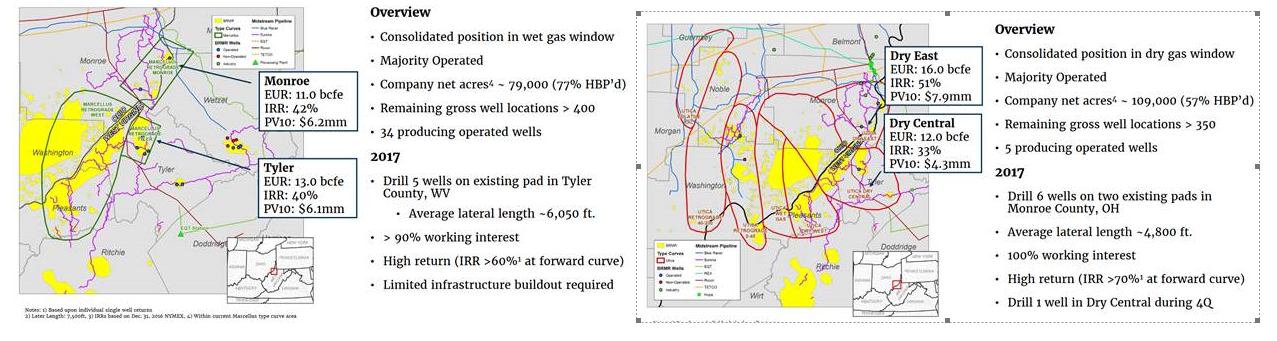

Blue Ridge owns significant assets in the Marcellus/Utica basins in Ohio and West Virginia. They own 77,000 acres in the Marcellus and 109,000 acres in the Utica. Much of this acreage is in the dry gas and gas-condensate sweet spots. Below are maps of their acreage in each basin (Marcellus on the left and Utica on the right):

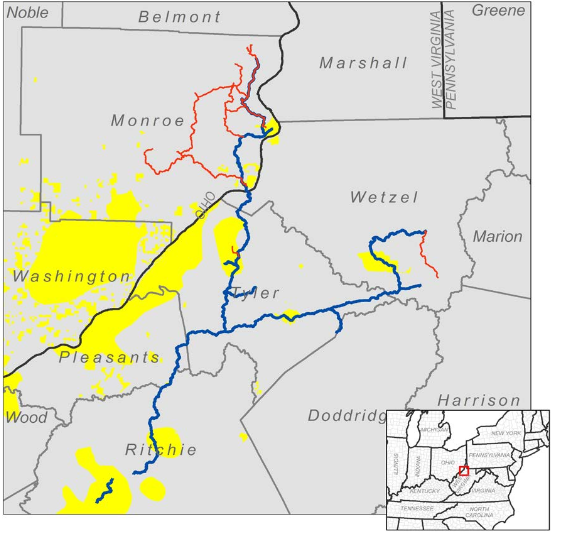

The company also has a 44.5% ownership in the Eureka pipeline, which is a gas gathering pipeline in Ohio and West Virginia that snakes through the Blue Ridge Mountain acreage.

The company also has a 44.5% ownership in the Eureka pipeline, which is a gas gathering pipeline in Ohio and West Virginia that snakes through the Blue Ridge Mountain acreage.

Blue Ridge has a market capitalization of $450 million at $9/share. At the end of second quarter, as they continue to sell off non-core assets (Magnum Hunter was a bit of a serial acquirer, so Blue Ridge Mountain has a range of assets outside on the Marcellus/Utica that are considered non-core, including some Bakken acreage, some Kentucky acreage, and other real estate holdings), they had almost $100 million in cash. They have no debt.

The Marcellus/Utica Acreage

Forgetting for a second about Eureka, lets just take the Blue Ridge gas assets on their own. Assuming a value on acreage alone, and assuming that about half of that has overlap between the Utica and Marcellus (I have not found any public information that delineates just how much of the Utica and Marcellus acres overlie each other) the stock is trading at around $2,500/acre. Recent transactions in the Marcellus/Utica have taken place anywhere between $5,000/acre and $9,000/acre. Here is a list of recent Marcellus/Utica transactions that I compiled:

![]()

The most recent transaction was when EQT Corp acquired Rice Energy for $8 billion. Here are comments on the acreage valuation of the deal and in the area:

Analysts with The Williams Capital Group LP estimated an average price per undeveloped acre for the transaction of $9,900, “which is roughly in line with core acreage valuations over the past year.” Analysts with Bernstein similarly calculated a per-acre price of around $9,000.

Now I don’t think that all of the acreage is worth $9,000/acre. I think that some of the acreage might be worth that though, or at least close to it. The Tyler, Wetzel and Monroe county acreage is all in the same counties as prior transactions, so I would expect it to go in the $4,000 to $8,000 per acre range and some of the Northern most acres might be worth $9,000 or more. Blue Ridge Mountain announced on their first quarter call that they divested a small number of acres (350) in West Virginia for about $4,500/acre.

I’m less sure about the acreage in Washington county, because I haven’t seen any transactions in that area of late. Of course this could be simply because Blue Ridge Mountain owns most of the prospective acres in Washington county (if you study their map you will note their leases cover most of the NE quadrant of the state). They said on the first quarter call that they planned to market the sale of 23,000 non-core acres in the southern part of Washington county in the second quarter. So it will be interesting to get more details on what they can sell that acreage for. They also said they would be drilling a well in Washington county in the third quarter of 2017 and the way they worded it gave the impression this is the first well they’ve drilled there in some time. All of this acreage is within the Marcellus and/or Utica windows, so I doubt that very much of it is going to be worth less than $2,500 per acre. Some of it is clearly worth much more.

Production for the Marcellus/Utica assets was 74MMscfepd in the first quarter. In the second quarter, because of asset sales, natural declines, and the fact that Blue Ridge hasn’t drilled any wells in a year, production had declined to 65 MMscfd.

The company expects to drill 4 Utica wells in the second half of 2017. With production from those wells, exit guidance is to get production back to 100 MMscfd. They described their base rate at between 51-59MMscfepd at year end, meaning that these four wells will add between 30-40MMscfepd. Their base decline is between 12-15%, which is quite low (this is the one benefit you get when you don’t drill any wells for a while). Given the low decline of the base production and the high impact of new wells, its not hard to see how Blue Ridge Mountain can grow production once they start drilling.

On a flowing boe basis, the current market capitalization (ignoring Eureka completely) values them at $32,000 per flowing boe net of cash. That number is much lower if you use exit production guidance. It is also not reflecting what is really valuable; the sizable undrilled land position with no wells on it throughout West Virginia and Ohio.

Eureka Midstream

While a case can be made that the natural gas acreage exceeds the current value of Blue Ridge on its own, there is also the Eureka pipeline to consider. Eureka has been underutilized for the last number of years because of limited takeaway capacity from West Virginia and Ohio. It currently operates at about 30% capacity. Nevertheless, the midstream operation is expected to generate $66 million of EBITDA in 2017. This guidance was reiterated in the second quarter.

Pipeline assets can go for up to 20x EBITDA. At 15x EBITDA Eureka would be worth about $300 million to Blue Ridge.

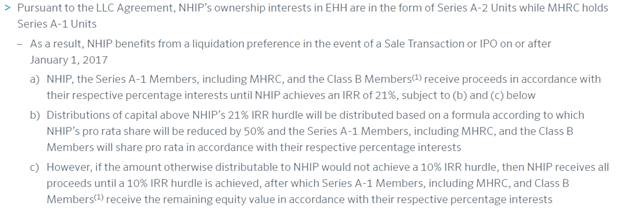

But there’s a catch. Morgan Stanley has a majority ownership (54%) in the pipeline. But Morgan Stanley also has a preferential return clause for their ownership: the return on their original capital investment is guaranteed a minimum of a 10% IRR in the event of sale. This works out to a preferential return of $672 million if a sale was completed this year. Below I clipped the relevant clause from the bankruptcy documents:

The preferential return clause makes me a little uncomfortable valuing Eureka. Its not clear to me what incentive Morgan Stanley has, as majority owner of the pipeline, to initiate a sale if they can watch their investment grow at 10% annually.

Nevertheless, the pipeline ownership is worth something. In its 2016 year end financials, Blue Ridge Mountain recorded their equity interest at $185 million. This is after a write-down of $180 million that the company took in November 2015.

Obviously, Eureka’s value could increase substantially as new takeaway capacity is brought on to take gas out of the Marcellus/Utica basins, which will allow midstream assets like Eureka to operate closer to full capacity. Blue Ridge Mountain said in the first quarter that they expected Eureka to exit the year with 1.1bcfpd of gas flowing through Eureka, up from 850mmscfpd currently. This 30% increase in throughput should help Eureka get closer to the 10% IRR that is consistent with the Morgan Stanley clause. Assuming a corresponding bump to EBITDA, Eureka would generate $85 million of EBITDA in 2018, which at a 15 multiple would value Eureka at $573 million for Blue Ridge Mountain.

The company has said that they are exploring options with Eureka.

Summing it up

So what’s it all worth? Well there is a lot of uncertainty with the numbers. With Eureka I can get anywhere from $150 million to $600 million. With the Marcellus and Utica assets it could be between $400 million and a billion depending on what you value the acreage at. So its a pretty big range.

But what I feel pretty comfortable saying is that together these assets should be worth more than the current stock price. Maybe significantly more. The hard thing is accumulating the stock. I think you have to just put in a reasonable bid with a long date and wait for it to come to you.