Week 197: “Make your money while you can”

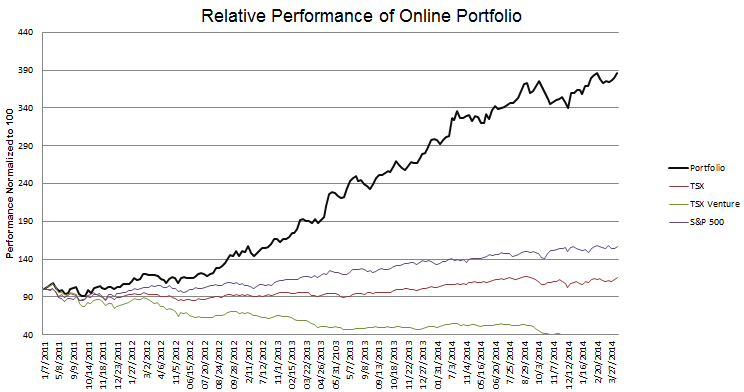

Portfolio Performance

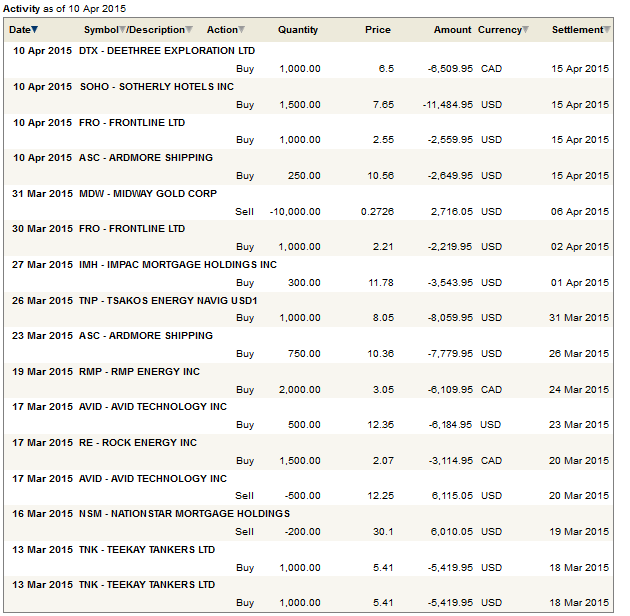

See the end of the post for the current make up of my portfolio and the last four weeks of trades

Monthly Review and Thoughts

On Thursday, while I was surfing around the web over lunch hour trying to figure out what I wanted to write about this month, I stumbled on a YouTube clip of Neil Young being interviewed on Charlie Rose. He describes what he thinks of Bob Dylan’s song writing (the quote in the title of this post is attributable to the Dylan song Rambling, Gambling Willie). Young observes the source of inspiration that leads to a great song.

The argument about whether investing is an art, a science, or just a mundane business is one that depends as much on who is making the argument as it does on an objective reduction of its reality. Investing has elements of all three and it’s essence is whatever one associates with best. I stand firmly in the camp that it is an art, and I think that for the kind of shooting star sort of performance I try to achieve it is that hard to put your finger on source of inspiration that leads to out-performance.

Maybe I am being too bold to analogize the making of a great song and the development of a great investment idea but as I stand back from both I do note some common characteristics. Both tend to be built on their historical predecessors, both stand in deference to the structure they abide in and, when done correctly, both live within the bounds of their genre’s common sense. At the same time each has to extend outside of that imposed limit just enough to see what is not easily seen, but not so far as to drop off the cliff of abstraction or dogma.

Most importantly though is that both are built upon a sensibility, one that is hard to put your finger on but nevertheless is there. Being more of a word guy, I can describe this best with lyrics; when you hear something that is right, you just know it, even though you might not know why. You can try to break it down to the linguistic structures, cultural context and the feelings it invokes, but I don’t think you will ever quite get to understanding. The right phrase in the right spot is right because it just clearly is, and if you happen to be possessed by the inspiration that Neil Young describes you will discern that and act accordingly.

The sensibility on which an investing idea is based is no less complicated, no less abstract, and I would argue no less difficult to reduce down to its essence. But if you are in the groove, you just know that a good idea is good before you even know why.

Two Interesting BNN Segments… the first on the market

I listen to a lot of BNN clips. I will have them on in the background as I’m doing research. Most of it is not helpful and I’ve become deft at tuning out the noise. But every so often I hit upon a gem. I came across a couple of those in the last month, with the first being this segment on market performance.

I can’t figure out how to embed a BNN video for the life of me so here is the link to the segment.

The theme is the performance of small cap stocks, and in it Jonathan Golub describes his thoughts on the small cap sector. The really interesting part is in the last minute, where Golub notes that in the average year that the economy is not in a recession you will see 16-18% gains in the stock market. But when we hit a recession you “lose all your chips” and the average loss is 35%.

A couple of points here. First, this exemplifies something I have been saying, that one has to get while the getting is good but be ready to get out when it ends. There is no hiding when the tide goes out.

Second, this is relevant to what we are seeing right now. All of the gnashing of teeth over valuations and the lack of a correction forgets that the stock market rarely makes a sustained move down when the economy is expanding. But once the economy begins to contract the moves down are exaggerated when compared to the amplitude change in growth.

In the mean time there are always ways to justify valuation. Right now the most common one is that with interest rates low, inflation expectations non-existent, so ergo a future dollar is worth more than it has been in the past. Therefore, paying a higher multiple for that future dollar of earnings is justified. This logic, which like all justifications contains both germs of truth and seeds of failure, can be used to rationalize stock prices to these levels and probably a lot further.

… and the second on oil

Over the last couple of months I have picked away at position in oil stocks on weakness and at this point have accumulated positions of a decent size in RMP Energy (RMP), Rock Energy (RE), Canaco (CNE), Jones Energy (JONE) and most recently DeeThree Energy (DTX).

There are still plenty of analysts and much of the twitter universe posturing for a further decline in oil and with it a commensurate drop in the oil stocks. I don’t know about oil, it may fall if the storage concerns are real, or it may not, but I do think that barring some further shock (ie. a demand shock brought on by a recession) we have seen the lows in the stocks.

It doesn’t make sense to me that oil stocks (at least the one’s I own) will fall to new lows even if the price of oil does drop further. I understand there are leveraged companies that can ill afford further whittling of their cash flow and for those names sure I can see further declines. But for well capitalized companies, I just don’t buy the idea that further panic will engulf them and send them down further.

To think that is to embrace the idea that an oil stock price should be based on the current price of oil. That’s crazy. Nothing in the stock market is priced off of current prices. If it was, shipping stocks would be trading at 3-4x what they are, Pacific Ethanol would have gotten to $50 for crashing all the way back down to $5, I could go on. Oil stocks, like everything else, go up and down based on the expectation of future business.

Turning again to a BNN clip, Eric Nuttall was on Market Call last week and he had some interesting observations about the oil market.

The four important data points that Nuttall provides are:

- US company capital expenditures are expected to be down 40-50% in 2015.

- Production has already seen monthly declines in Eagleford and Bakken

- The natural decline in the US is 2mbbl/d per year

- Weatherford was recently quoted of saying that international capital expenditures have fallen by 20-25% and that as a result they expect production ex-US and ex-Canada will fall by 1.5mmbbl/d in 2016

I think there is a growing understanding that prices are too low to support stable production levels worldwide and that we will soon (in the next 9 months) see the impact of this as supply turns down. Without getting into too many details, I have seen enough declines of Eagleford and Bakken wells to know that these fields are not eternal springs of flowing oil. We are already seeing the first signs of declines in these fields. And the natural gas analogy is flawed; there is no such thing as associated oil, so there will be no analogy to the associated gas (and of course the Marcellus) that led to the strong production from natural gas even as rig counts fell.

What I find ironic is that many of the same names who derided oil companies for not producing free cash at $100 are somehow confident that production will remain high at $50. It seems like a rather bizarre confluence of opinion to me.

But most investors are beginning to realize that well financed oil companies will soon be making significantly more cash flow than what is implied by plugging in the current spot. So I don’t think we see new lows in names like those I own, or if we do it is going to be an operational catalyst (see RMP Energy for an unfortunate example), not a general malaise.

Portfolio changes

I did not make a lot of portfolio changes over the last month. The few things I did do was to add two more shipping companies to my basket of tanker stocks, and a cheap little hotel REIT trading well under net asset value. I will discuss each below:

Ardmore Shipping

As I watch my tanker trade finally start to pay off, in the last month I added three new tanker stocks, Euronav (EURN), Tsakos Energy (TNP) and Ardmore Shipping (ASC). There was a good Seeking Alpha article on Tsakos, which is available here, and I’m still stepping through my research into Euronav, so I will focus my discussion here on Ardmore.

Both Ardmore and Tsakos allowed me to dip my toes into the product tanker market. Up until now I have focused my purchases on crude tanker companies. However, with oil prices low demand for oil products (gasoline, heating oil, jet fuel and the various chemical product inputs) should be strong. While Tsakos Energy has a diversified fleet with 30 crude tankers and 29 product tankers, Ardmore is a pure play on the product tanker market with a fleet consisting of only MR tankers.

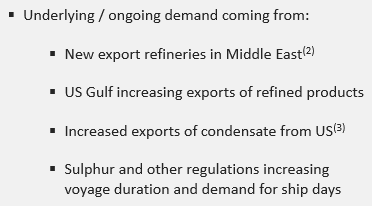

In addition to the demand story, Ardmore listed the following reasons to expect strengthening demand in the product tanker market.

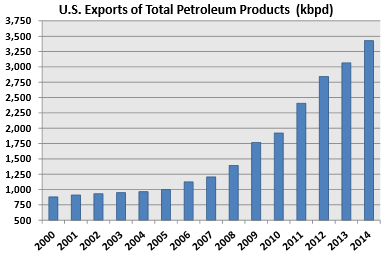

The following chart is from the Capital Product Partners corporate presentation, and it illustrates the extent to which point 2 from above is asserting itself:

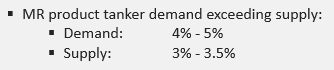

On the supply side, Ardmore sees demand outstripping supply in the medium term:

On the supply side, Ardmore sees demand outstripping supply in the medium term:

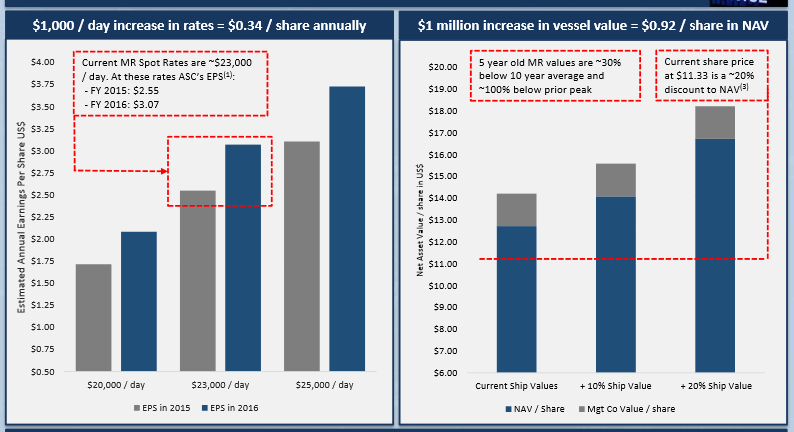

So the supply/demand situation is favorable. But what really drew me to Ardmore is their valuation. The company provided the following charts on Page 7 of their January presentation.

Right now MR spot rates are above $23,000 per day. From the above slide, the company is saying they expect to earn at least $2.55 per share with rates at current level, and the stock trades at a little more than $10.

Ardmore owns and operates exclusively MR2 tankers (mid-range tankers). They have a fleet of 24 tankers including 10 new builds that will delivered throughout this year. The fleets average age is only 4 years. Their operating fleet is almost entirely on spot or short term charter.

While Ardmore looks cheap on an earnings basis they are also reasonable on a net asset value basis. According to their January presentation Ardmore is priced at a 20% discount to net asset value.

While Ardmore looks cheap on an earnings basis they are also reasonable on a net asset value basis. According to their January presentation Ardmore is priced at a 20% discount to net asset value.

I still like the crude tanker story more than the product tanker story, and indeed my bet on tankers is severly skewed to the crude tanker side (I know, DHT, TNK, EURN, FRO, and NAT on the curde side). Nevertheless I do think there is upside in both and that Ardmore is a solid way to play the product tanker side.

Capital Product Partners

While Capital Products Partners was one of the first tanker stocks I bought, but I haven’t written much about them and so, since I’m talking about the product tanker market in this post, I wanted to give them a bit of space here.

Capital Product Partners differs from the other tanker plays that I own in that it is not a direct play on the spot market. Every vessel that the company owns is chartered out for the long term, with some of those charters lasting upwards of 10 years. Capital Product Partners also differs from the other positions in that it is a dividend play. The company distributes virtually all of its available cash flow in dividends and markets itself to dividend investors.

Yet even though the company has very little exposure to the spot rate, I still look at this as a play on nearterm tanker market fundamentals. The idea here is that as rates prove themselves durable, investors will become more comfortable with the dividend sustainability of the company and perhaps anticipate increases to the dividend. The shift in sentiment should lead to capital appreciation, which when combined with the 10% dividend that the company pays will need to a nice overall return.

Capital Product Partners is primarily levered to the product market. In all they have 18 product tankers, 4 suezmax tankers, 7 containers and 1 capesize dry bulk vessel all with period employment. Their fleet is fairly young with an average age of 6.5 years (their MR fleet is on average 8.3 years old). In addition they have 3 container vessels and 2 MR tankers being delivered in 2015, all of which will be on long term contract:

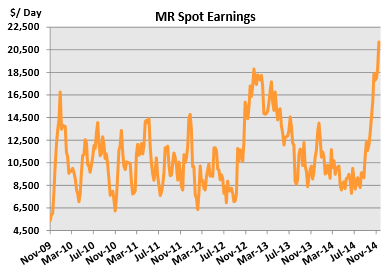

In their corporate presentation, the company provides a chart giving some historical perspective to current MR rates. As you can see, MR spot rates are higher now than they have been in some time, and since the chart was published, rates have gone higher still and are now in the $25,000 per day range:

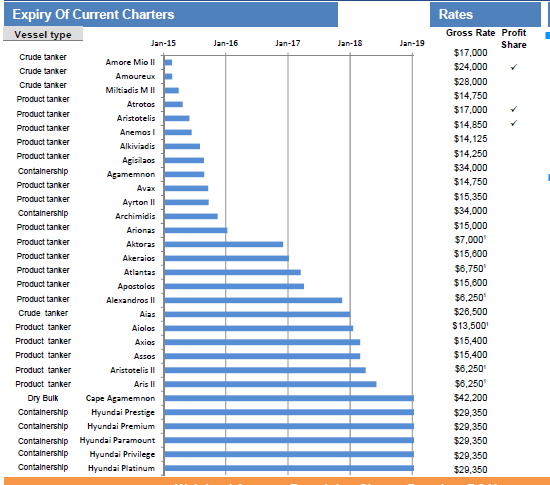

Below is a table illustrating the expiry of charters for Capital Product Partners. Notice how the expiry of most of the product tankers occurs in 2015, which should result in rate hikes to the majority of the renewals, whereas the containerships and the dry bulk vessel, for which the market is currently in excess and rates very soft, are chartered for years in advance.

Below is a table illustrating the expiry of charters for Capital Product Partners. Notice how the expiry of most of the product tankers occurs in 2015, which should result in rate hikes to the majority of the renewals, whereas the containerships and the dry bulk vessel, for which the market is currently in excess and rates very soft, are chartered for years in advance.

I have some questions about the long-term sustainability of the dividend, but I don’t think I will be sticking around long enough in the stock to warrant too much consternation over them. They’ve been paying a dividend for a while, so from that perspective things look good, but I still am uneasy over the long term in the same way that I am around many of these capital intensive businesses: Asset purchases are lumpy and large and so free cash generation follows suit which makes it really difficult to discern exactly what the average free cash is over the long term.

For example cash flow from operations over the last 3 years has been $125mm, $129mm and $85mm respectively. Vessel acquisition and advances less proceeds has been: $30mm, $331mm and -$20mm (in this year dispositions exceeded acquisitions and thus resulting in negative overall expenditures). Clearly the company’s free cash has whipped wildly over this time. Taking the three year period fas a whole, free cash (before dividend) has been essentially nil at -$2 million.

Now some might look at this as a red flag and something to be avoided, but I think it fits quite well into the thesis (which is short enough in duration to not worry too much about the long-term sustainability). No doubt investors are assigning the 10% dividend in part because they are evaluating the same free cash flow numbers I am and questioning the sustainability of that dividend. If however charter rates do show themselves to stay high for the short-term (lets say the next 12 months), this concern will be alleviated and backward looking free cash flow models will be thought to be inadequately pricing in what will come to be viewed (by some at least) as a secular change in rates.

Whether the rate change will be truly secular is up for debate; I really have no idea what rates will be in 2 years let alone the 10 or 20 years relevant for modeling Capital Product Partners sustainability and I think that anyone who does better have called the downturn in the oil price 2 years in advance to have credibility in that prediction.

What I do know is that when the price of a commodity changes, even if turns out to be for a short time, there consensus perception of that commodity shifts at the margins, and that shift in perception can make very large differences in the valuations of those equities priced off of the commodity. Such is the nature of the world we live in and rather than gnashing one’s teeth at the uncertainty, better to take advantage of it and make a few bucks on the euphoria.

Sotherly Hotels

I have been on the look-out for some safer investments. As much as I enjoy speculating in tankers and airlines and oils, these remain short-term plays. I doubt I will have investment in more than one or two of these stocks in a years time.

I came across Sotherly from a SeekingAlpha article available here. Its written by Philip Mause, whom I have been following for a while and of whom I have gotten a number of solid income oriented investment ideas from.

The income angle of Sotherly is modest, the company pays about a 3.5% dividend, but they have a exemplary habit of increasing that dividend on a quarterly basis. I’m also pretty sure they could pay out a significantly higher dividend if they chose to. The dividend amounts to about 25% of AFFO, and they expect AFFO to grow from $1.09 per share in 2014 to $1.21 in 2015.

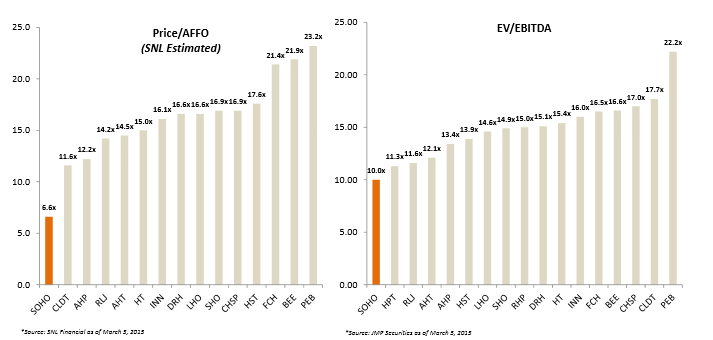

The stock trades at a significant discount to other hotel operators as the chart below illustrates.

I think that the reason the stock trades at such a discount is its size; with 10.5 million shares outstanding and another 2.55 million units, at $7.74 the market cap of Sotherly’s is only about $101 million. Volume is typically light and so its too small and too illiquid for most institutions. But the smallish dividend likely limits its attractiveness to the retail contingent. It is in this no-mans land that there is the opportunity.

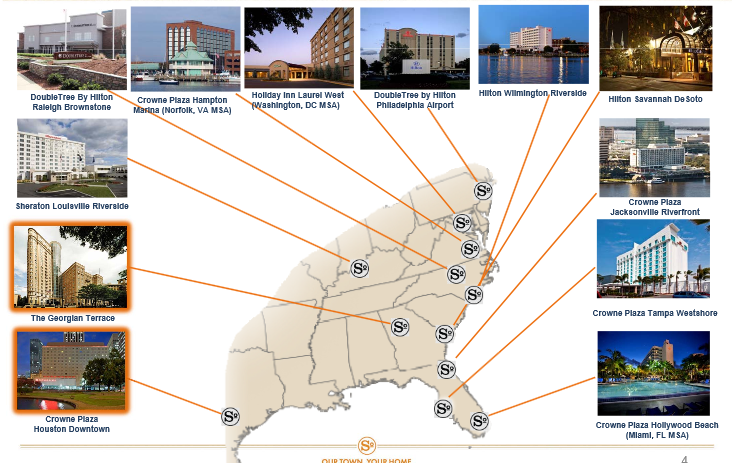

The company’s stable of hotels is situated across the south east United States:

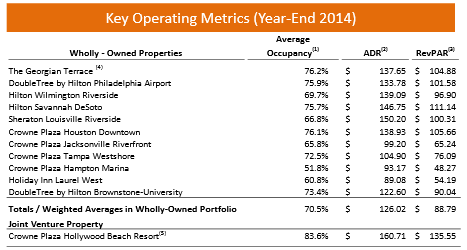

In total these hotels have a total of 3,009 rooms. Looking at this on a standard EV/room basis, rooms are priced at $112,662 per room, which isn’t particularly cheap. However this is mitigated by fact that these are mostly high-end hotels – ADR and RevPAR are quite high:

On an EV/EBITDA the stock trades at 11.7x and on FFO basis they trade at 5.7x. The company guided AFFO for 2015 of $1.24 per share and on the conference call when confronted with some discrepancy in the high and low estimates for their AFFO guidance they were forced to admit that they were being conservative on the high end. Again turning the the company presentation, they put the “inherent value of assets” at over $17 per share:

On the last conference call management was adament that they would not issue equity at these prices and that they would need to see at least $10 before reconsidering that position. While they have some exposure to Texas, thus far occupancy does not seem too impacted by oil and many of their larger corporate customers are not oil related. I’m not sure what else to write about this one. Its a solid hotel operator trading at a discount to peers for not a very good reason. As long as the economy remains sound I think the stock slowly walks up to the double digits over the rest of the year.

Impac Mortgage

I’ve gotten a bunch of questions in emails about Impac Mortgage. So yes, I have bought back Impac, I took a tiny position around $9 and added to it at $11. But its a small position and I haven’t talked about it on the blog or on twitter. The reason? I really don’t know how this plays out, so my thesis is pretty weak.

The company is doing some interesting things. They have a deal with Macqaurie for the purchase of their non-QM originations and they bought out a fairly large online origination business called CashCall. So they are doing something, and the share price is reacting. Still, I find it hard to quantify what it all means for the fair value of the stock. So I really dont know what I’m buying.

If you look at the recent financials and they aren’t great, so the bet I’m making here is kind of a bet that Impac is going to use these pieces and become a big non-compliant originator but while that qualitatively seems like a sound thesis, I don’t really know what numbers they will be able to churn out. To put it another way I probably wouldn’t have bought the stock if I didn’t have a history of it and some comfort that Tomkinson seems pretty experienced and can put something together. So I own the stock but probably won’t talk about it any more unless something happens to clarify the situation.

What I sold

Midway Gold

My Midway Gold sale wasn’t quite as bad as it looks. I forgot to sell my holdings in the practice portfolio account and by the time I realized this the stock had tanked to under 30 cents. So my sale looks particularly ill timed.

Nevertheless I sold Midway at a loss after the company announced delays with Pan, a potential cash shortfall and some early problems with grade. The company realized news in its March update that one of the water wells malfunctioned so it has taken them longer to fill up the tailings pond and that Pan would not see the first gold pour until the end of the month, delayed from early March estimates. Worryingly the company had drawn $47.5 million of its $53 million lending facility and was under negotiations with its lenders to fund working capital requirements. To make matters worse early results showed some grade discrepancies with their model as grades were coming in lower.

Of all the news, it was the grade discrepancies that led me to sell. If it hadn’t been for that I would have chalked it up to early days mining hiccups that they would eventually struggle through. But until the grade issue is resolved you just don’t know what you are getting. So I had to sell.

Nationstar Mortgage

As I wrote in my comment section last month, I didn’t talk about Nationstar because the stock was a trade that I didn’t expect to hold very long. As it turned out, I held it hardly any time at all, selling the stock in the day following the posting of my last post. Nationstar was down below $26 when I bought it and I sold it at around $30, so I made a little profit on the transaction.

I bought the stock because I thought there were some tailwinds here in Q1: the company said on their fourth quarter conference call that so far in first quarter originations were strong. They also expected amortization to be lower in the first quarter, which will boost earnings. Nationstar also has a reasonable non-HARP business so they don’t face quite the pressure Walter Asset Management does at that winds down and that, combined with the evolving travails at Ocwen, might bring marginal dollars into the stock from investors looking for the one remaining non-bank servicer without significant regulatory risk (or at least so it appears). Nevertheless I figured the move from $26 to $30 was probably too far too fast so I took my quick profit. I have been thinking about buying back in for another run now that is again languishing in the mid-$20’s.

Final Thoughts

I waited three months for it but the tanker trade is upon us.

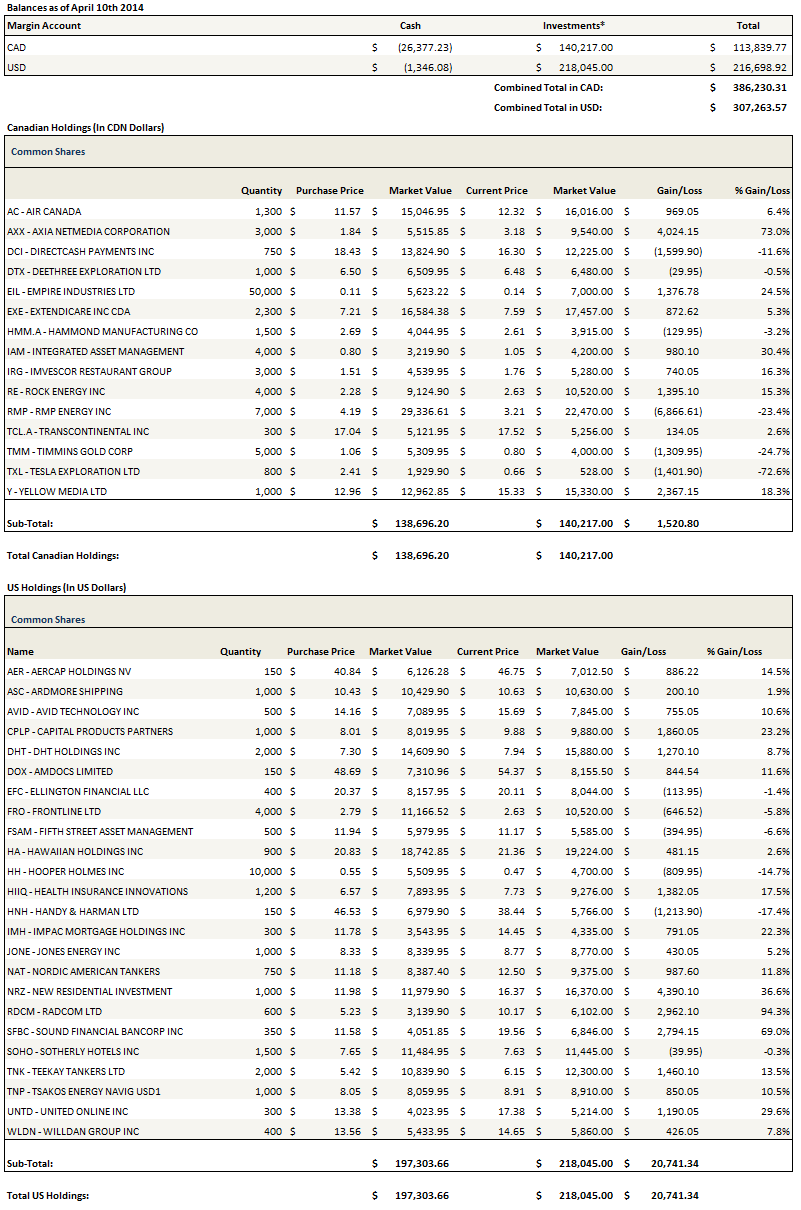

Portfolio Composition

Click here for the last four weeks of trades.

{kind=link}