When I sold Health Insurance Innovations in the spring their business was under attack from the department of Health and Human Services (HHS). The HHS had decided that short term medical insurance policies (STM) were an end run around the affordable care act (not an unreasonable conclusion) and was proposing a rule change (subsequently implemented) whereby STM policies would be limited to “less than three months, and coverage could not be renewed at the end of the three month period”.

So I sold. It seemed like a broken business model, which was unfortunate as Health Insurance Innovations had just hit their stride.

But then the Republicans swept the election. The Affordable Care Act will likely be spun back into some other form. The headwinds become tailwinds. While it’s not clear what form health care insurance will take going forward, I think it’s reasonable to assume the changes will be positive to Health Insurance Innovations.

While took some time for investors to notice that his tiny sub $100 million market cap company had just had its prospects turn for the better (small caps are not efficient), the stock has been on a tear since the day after the election.

Because I’m not sure exactly what the eventual impact will be, I’ve taken cues from the market, adding as the stock goes up. This has worked out pretty well as I put on a small initial position in the 6’s, then added in the 8’s, the 9’s and then at 10.

But I’m not adding any further. I don’t have a large position, but its enough given that I don’t really have a sense of what will succeed the ACA, and Health Insurance Innovations has some legal and regulatory issues that are yet to be resolved and that lend to some uncertainty. These state regulatory examinations of some of their third-party distributor call centers are described in the latest 10-Q.

My optimism that the eventual outcome of the ACA rework will be positive for Health Insurance Innovations is because their business relies more on a platform than any particular insurance product. Their AgileHealthInsurance.com platform is a comparison and online enrollment tool that can sell any type of health insurance product. The site lists products available from multiple carriers and helps consumers pick a product that meets their needs and is the most affordable option.

The company supplements AgileHealth with a retail channel where they sell through third party call centers and I believe still own one call center (ASIA). They restructuring two others, Secured and ICE in November 2015. They stock theses channels with policies from a wide range of carriers, including HCC Life Insurance Company, Companion Life Insurance Company, Standard Life and Accident Insurance Company, Nationwide Mutual Insurance, and US Health Group.

Health Insurance Innovations engages with the carriers to create new products depending on the current regulation environment and demand. They have primarily sold short term medical and auxiliary health plans because that is all that the ACA has allowed for. On the third quarter call they talked about how they are working with carriers to create product alternatives to STM.

I think that there is a good probability that whatever replaces the ACA will have more choice. This is in the direction Republicans typically lean. More choice should play into the hand of Health Insurance Innovations, their platform and their carrier relationships.

The stock is not expensive. If I gave you the following metrics what would you value the company at?

9 month year over year revenue growth of 30% and policies in force growth of 46%

Adjusted EPS of 33c in the third quarter and full year revenue guidance of between 88c and 95c EPS

2017 topline growth of 20%

Net cash ($5 million of debt and $14 million of cash) on the balance sheet

Note that I am adjusting the company’s 2016 revenue to account for the impact of moving owned call centers to be third party and the associated accounting treatment of this. GAAP revenue growth has been over 70% year over year.

Even after a pretty tremendous move up, at $11 the stock is not really pricing in its earnings and growth.

Of course up until November 8th this made sense. While the company said they could overcome the inevitable revenue decline from STM, I don’t think many believed this. There was already evidence that new applications were flattening from the second to third quarter (see the submitted IFP applications in the third quarter press release). Even as the company showed that Limited Indemnity Medical insurance (LM) made up 45% of Individual and Family Plans in the third quarter, the stock price hardly budged.

Now that the future of the ACA is uncertain, and given that Republicans tend to err on the side of choice, things seem to be setting up much better for the company. While its hard to buy into a stock that has run up as much as Health Insurance Innovations has in as little time as it has, I don’t think you can make the argument that it is unreasonably expensive at this price. I’m willing to hold on here and see if it has further to go.

Hadoop is an open-source data management platform. It allows for easy processing and storage of really big datasets. It is an open-source initiative, meaning the software is free and written by many different companies.

Hadoop consists of a number of applications, but two are key and form the foundation of the platform; a storage system called the Hadoop Distributed File System (HDFS) and the process and an analysis framework called MapReduce.

HDFS is based on a distributed file system originally created by Google called the Google File system (GFS). The first 15 minutes of this Cloudera video provide a good explanation of the history and basic structure of that file system and its evolution into HDFS.

The analysis framework MapReduce is used to query and process data stored on the HDFS. This video describes the basic principles on which MapReduce works.

Built on top of HDFS and MapReduce are a whole bunch of other tools. These tools let you schedule jobs and manage resources (YARN), run SQL queries (HIVE), provide indexing for searching (SOLR), improve upon the processing techniques of MapReduce (IMPALA and SPARK) or even provide a simpler framework for writing Hadoop programs (PIG). There are others.

The open-source initiative on which HDFS, Mapreduce and the other tools are available is called the Apache Hadoop project. The Apache Software Foundation is the volunteer body that decides the direction of development and manage what tools will be developed and by whom. Individual companies that are member of the Apache Hadoop project propose new applications and then develop those openly for all. For example Hortonworks built YARN and put the code up on Apache and it is free for anyone, including competitors.

So what would you use Hadoop for?

Here are a few examples I came across. Imagine trying to store customer usage data from a pool of ATM’s being used across the country at a large bank. Or collecting information on driving and usage patterns of a connected car fleet. Or storing machine data from a large manufacturing operation. Or an oil and gas firm collecting real time minute by minute drilling, seismic or production data.

Any application where the data set is large, analysis of the data requires that it be stored, and where storage would be unmanageable in traditional database structures is data that would be conducive to Hadoop. Cloudera provides a number of use cases in this paper.

Hadoop is particularly useful for unstructured data sets. An unstructured data set is where the data doesn’t follow a particular table or columnar style. Social media data, mobile data, internet of things data coming straight from the device would all be typical examples of unstructured data. Conversely think of an Excel workbook, where data is laid out in a particular column by column metholology as an example of a structured data set.

Hadoop uses a methodology called schema on read that makes it particularly adept for unstructured data. Schema on read means that data that is read into HDFS does not need to have any particular structure. Instead the schema can be created at the time that the data is accessed and analyzed, at which time it can take on a form most suitable for the analytics being performed.

One feature of the HDFS storage system is that it doesn’t care what format the data is in. You can add data from an Oracle database, from an SQL database, or from an IoT application stream. HDFS doesn’t care, all the data can reside together. When you have a large database of hybrid data, usually somewhere on the cloud, its referred to as a data lake.

Hadoop Implementation

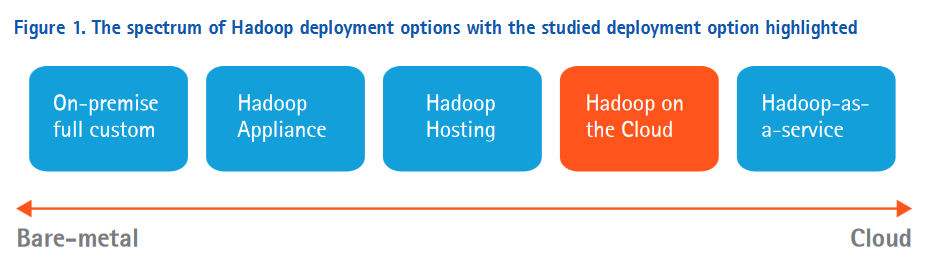

Hadoop implementation began as an on-premise extension of traditional databases. It was a response to the expanding amount of data being gathered and the unstructured nature of some of that data, which had caused requirements to surpass the capabilities of applications like Teradyne appliances.

Today, with the advent of the public cloud some customers are choosing to push data and workloads out into the cloud; to AWS or Azure for example. So far the work has been “ephemeral workloads”, which means that data is pushed out for a particular job, maybe to run analytics or reporting and then it is turned off. But as time goes on the move will likely be towards more data residing permanently on the cloud.

This paper by Accenture describes the deployment options and prices them out against one another. The figure below, taken from the paper, illustrates the range of implementation options.

While a company can implement Hadoop on its own, because of the complicated nature of its implementation (and from what I have read the bugginess of the code) they are more likely to contract support services from a company of experts to help with the integration.

This article lists some of the biggest players in Hadoop integration. Cloudera and MapR are both private start-ups, while Hortonworks is a public company. Each is involved with the development of the open-source applications as members of Apache.

Because Hadoop is open-source they are also limited with what product they can sell. Some, like MapR and Cloudera, have proprietary applications that work with Hadoop. Hortonworks, on the other hand, only distributes open-source software and generates revenue strictly through its implementation, support and maintenance services of the Hadoop infrastructure that they implement.

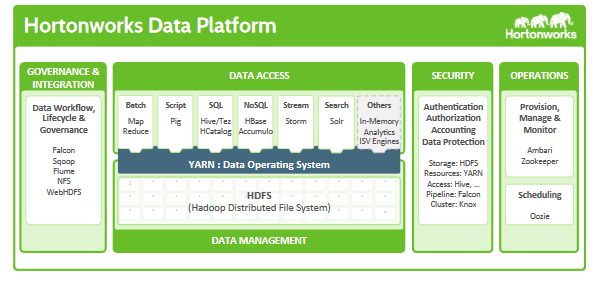

Below is the Hortonworks data platform. It consists of HDFS, a number of data access tools including MapReduce, and then supporting tools that let you manage, govern and support that data. Some of these tools (like YARN) were developed by Hortonworks, while others were developed by other Apache members (like MapR and Cloudera).

Why Invest in this Space?

There are a few trends that are converging that I am looking for ways to capitalize on.

First, the need to analyze large volumes of unstructured data, from social media, from mobile, and soon from Internet of Things devices, is going to continue to grow. Hadoop is the best technology for storing that data. In their Deutsche Bank Technology Conference presentation, Hortonworks said that there are already now 10x as many hadoop nodes as nodes on Teradata.

Second, as the cloud gains more acceptance as a trusted depository for proprietary data I think more of that data is going to find its way to Hadoop databases that exist on the cloud. So moving data to the cloud, and analyzing and managing that data on the cloud, is going to grow in importance.

Third, much of the data coming from unstructured sources is going to be best utilized if it can be analyzed soon after it is received. This sort of data analysis is referred to as “data in motion”, as opposed to “data at rest”, which is data that sits and accumulates over time. The traditional Hadoop systems are designed to store data at rest. However there are other tools, such as the Apache Spark and Kafka projects, that are tweaking Hadoop (in the case of Spark) or building a data in motion platform that can run parallel to Hadoop (in the case of Kafka) to handle data in motion.

Both types of data are going to need to work together. Historical data at rest gives context and provides learning while streaming data delivers timely insights. This very short video from Hortonworks has a good graphic that illustrates how data in motion can be ingested, analyzed and then given persistent storage in Hadoop.

I’ve been looking for ways that I can take advantage of these trends. The two companies that I have found so far are Hortonworks and Attunity.

Hortonworks

I took a small position in Hortonworks after the Goldman downgrade of the stock. I added to the position as it rose after printing a solid third quarter but have kept the position relatively small as I still have some trouble with their open-source model.

The company is growing at a 40%+ top line rate. Even after the recent move to $9 it is not expensive relative to peers growing at a similar rate. The company has an enterprise value of around $400 million and given that it generated a little under $50 million in revenue in the third quarter it is trading at less than 2x forward revenue.

The Hortonworks business model is to sell subscriptions for the integration and maintenance of their Hortonworks Data Platform (HDP) and open-source product. The revenue model is recurring and prices their services on a “per node” basis, which means that as companies scale out their Hadoop infrastructure Hortonworks takes an proportionate piece of the pie.

In addition to it Hadoop platform, Hortonworks acquired a company called Onyara in 2015 that expanded their suite of data analysis and management tools to include data in motion. From this acquisition they have developed a second platform called Hortonworks Data Flow (HDF). The HDF platform is part of another Apache project called Nifi and provides

“an infrastructure to acquire data and store it, taking into account data that has to be processed quickly to have value (low latency), discarding data after it has reached its useful limit, and d provide decision making when the data coming in is coming in faster than speed of storage.”

There is a good youtube video here (it’s a little long but the first 20 minutes is worth watching) that describes how HDF works.

HDF leverages the trend towards analyzing data as close to the point of origin as possible. The vision with HDF was expressed at the Pacific Crest conference as follows:

Now [customers] want to have the ability to manage their data through the entire life cycle. From the point of origination, while its in motion, until it comes to rest and they want to be able to drive that entire life cycle. It fundamentally changes how they architect their data strategy going forward and the kind of applications and engagements they can have with their customers. As they’ve realized this in the last year its changed everything about their thinking about how they are driving their data architecture going forward starting with bringing the data under management for data in motion, landing it for data at rest and consolidating all the other transactional data. So it’s a very big mind shift that’s happening.

Hortonworks has said that they expect HDF to make up one-third of revenue next year. That is significant growth from what is currently a small base. I think one of the most interesting aspects of Hortonworks is the growth it potentially can generate from HDF that does not seem to be adequately reflected in the stock price.

There are decent Seeking Alpha articles on Hortonworks here and here but it’s the comment sections that are particularly useful. Hortonworks also attends a lot of conferences, and their presentations at Deutsche Bank, RBC , and the previously mentioned Pacific Crest are all worth listening to.

Hortonworks reminds me a bit of Apigee. It’s a recent IPO, a fast growing company, and where some of the analyst community have lost faith in their ability to continue that growth. Therefore you have a multiple that is out of sync with the growth rate, and where a stabilization or acceleration of the growth rate (something we saw in the third quarter) should mean the stock gets re-rated to at least its prior level.

Attunity

The other way I am playing the evolution of big data lakes of unstructured data is with Attunity, which provides tools for data transfer and visibility.

Attunity has 3 main products. The main revenue driver, Attunity Replicate, facilitates the transfer of data across databases, data warehouses and Hadoop platforms. A second product, called Attunity Visibility, provides insights into your database by monitoring data usage, identify which databases/tables/columns are being used frequently and identifying who is using the data. A third product, Attunity Compose, automates many of the aspects of designing, building and managing your data warehouse.

Hadoop data lakes fit into Attunity’s product strength because they require large scale, heterogeneous, real time integration. One of the benefits of Replicate is its ability to transfer data from a wide variety of data sources. The company had this to say about the Hadoop opportunity on their first quarter call:

…the Hadoop environment creates huge opportunities for us to be more competitive and serve the markets much better. Customers are asking us basically to automate more and more the activities that are happening with Hadoop. So you really provided an end-to-end automation process and that’s one of the focuses we have.

Attunity has a bunch of case studies on their website that illustrate how Replicate and Visibility are used – most involve transferring data from a main hub (ie. A legal case file database that cannot be queried directly) or from operational databases (ie. Oil sands plant databases or retail location databases) for consolidation, to offload or to run workloads offsite.

There is also a very good SeekingAlpha article here that gives a revenue breakdown between products that is very useful. I would recommend making a copy of the article as I don’t know how long it will remain in front of the pay wall.

I’m less excited about Attunity than Hortonworks. Attunity faces a lot of competition in the extract-transfer-load market, they compete against Informatica, Oracle’s GoldenGate and SAP. Gartner recently named them a “challenger” in the magic quadrant (here is the report ). That means that they are not yet considered a leader in the field. In particular the report said:

While awareness of Attunity is starting to grow in this market, there remains a lack of recognition by buyers seeking data integration tooling as their enterprise standard.

Attunity has been growing Replicate revenues at around 25% but their legacy business has been shrinking and the Visibility product is not selling well so far. Compose remains a small portion of revenues.

So it’s a bit of a show-me story. I like the idea enough to take a starter position, but I would want to see some signs of accelerating adoption by large enterprises before adding. I would add at a higher price if I see that, because the opportunity with it, as with Hortonworks, is large.

I bought Supernus over a month ago and added to that position after the election result. With concerns of political attacks on the biotech industry abating I wanted to increase exposure to biotechs. Supernus seems like a good vehicle for that.

But going into last Friday I was getting a bit worried. The company had not announced its third quarter results or given any indication of when they would announce them. More often than not such silence foretells a negative event.

In this case however, there was no such concern. On Friday Supernus did announce (ominously) that they would have to restate prior results (generally the worry when you have radio silence leading into a quarter) but the reason behind the restatement was benign. A $30 million royalty from 2014 was previously classified as revenue and is to be reclassified as debt. The change came up after their accounting firm was given guidance by the SEC for another company in a similar situation.

I dug into the details a bit and to be honest it doesn’t make much sense to me why a royalty not being paid back has to be classified as debt but whatever, its water under the bridge.

The preliminary third quarter results, announced on Monday, were quite good. The company reported strong growth and raised guidance.

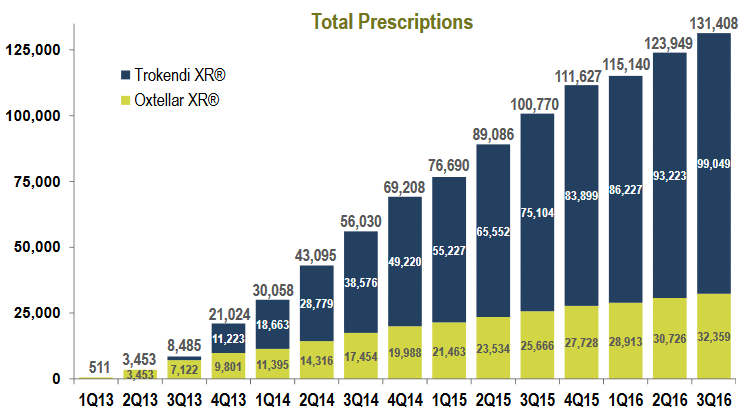

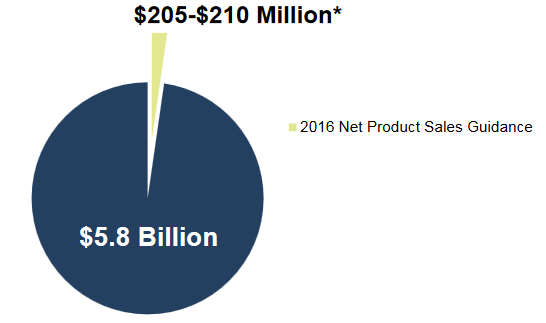

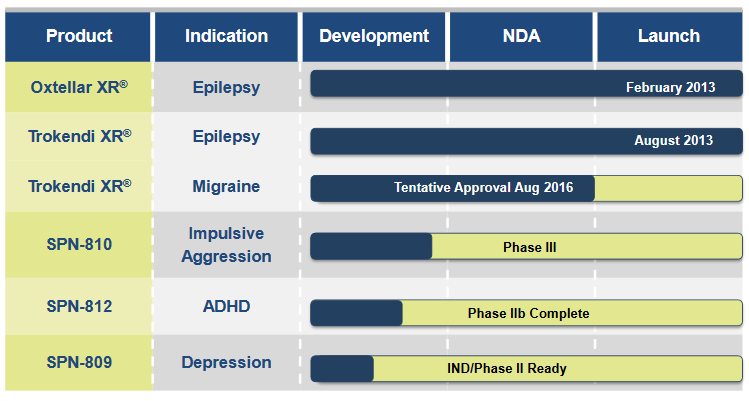

Year to date consolidated sales were $149 million, which is a 48% increase year over year. Total prescriptions for both Troxendi and Oxtellar were 131,000 for the quarter, an increase of 30% year over year. Troxendi prescriptions were up 32% while Oxtellar’s were up 26%.

As had been previously announced, there was a tentative approval from the FDA for Troxendi to be used in the treatment of migraine, which should help continue sales momentum.

The company illustrated the total addressable market for these drugs in their slide presentation. The opportunity for growth remains large.

The drug pipeline consists of two drugs in later stages of development, SPN-810 and SPN-812. Both are being trialed for children, the former for impulsive aggression and the latter for ADHD.

SPN-810 had been struggling with enrollment and in the second quarter the company took steps to address this. In the third quarter update they listed a number of initiatives taken (engagement of an enrollment agency, increasing the patient screening period, giving more education to caregivers on proper diary compliance) and gave color that these had a “positive impact on patient referrals”.

Results of the Phase 2b study for SPN-812 were announced a month ago. Following up on those results, management commented that they would begin discussions with the FDA on a Phase 3 trial. An interesting development is that the trial may include a higher dosage than those used in Phase 2.

Being a non-stimulant gives SPN -812 an advantage with side-effects but stimulants also typically have higher efficacy. That did show through in the results from the Phase IIb trial, where results were “remarkable” for a non-stimulant, but still not quite on par with its stimulant comparatives.

There is a market for SPN-812 as a non-stimulant for patients where stimulant side-effects are too severe. However there is a much bigger opportunity if SPN-812 can show efficacy that is in-line or better than a stimulant. The Phase 2b trial did not take the dosage high enough to test out this possibility. However the benign side effects and the strong efficacy at lower dosage suggest it has a chance.

Both SPN-810 and 812 are a couple of years away from approval. The company would like to fill the gap between now and then with an approved or nearly approved drug. Ideally they would be looking for a drug in neurology, where they could leverage the existing sales staff, or in psychiatry, where they could gain an early foothold before 810 and 812 are launched.

Supernus was a bit of a gift in the mid teens but its moved quickly back to $23 in the last couple of weeks. At this level it trades at an enterprise value of 5x revenue. Growth is over 40% and not slowing down. I continue to like Supernus and am happy with my current position size.

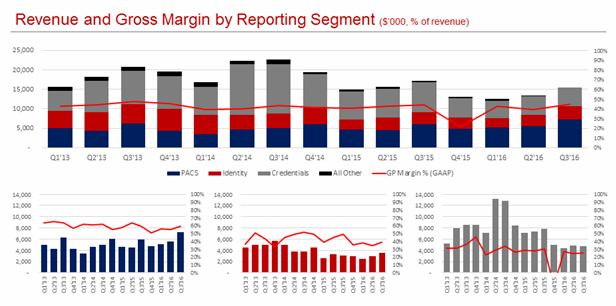

I was pleased with Identiv’s quarter. Revenue was down year over year but that is mostly due to discontinued transponder sales to Disney. Excluding this customer revenues were up 13% year over year. The company appears to be on track.

Sequentially revenue was up 31% for the Physical Access Control Systems (PACS) segment, 21% for Identity (smart card readers) and was down a little in RFID. The third quarter is seasonally strong for PACS because of government customers that have a September year end. But that alone doesn’t explain all of the strength in the results.

The story here remains that a turnaround is occurring on the expense line. Operating costs are down to a $6 million quarterly run rate. Last year they were double that.

The stabilization of the top line and improved expense management has led to positive EBITDA for the first time in a while. They have $1.7 million of adjusted EBITDA (no stock option expense) in the quarter.

Guidance was kept the same at $56-$60 million, which puts the fourth quarter revenue in the $14-$18 million range.

I think there is a good chance they can hit that range. The fourth quarter is seasonally slower than the third quarter

I tweeted a couple of times this morning that I don’t think the stock makes sense at a $20 million market cap. Its moved up since then but even at $2.50 the market capitalization is still less than $30 milion. The company has a $55 million trailing twelve month revenue run rate, they are showing growth, they are EBITDA positive now and its not an insignificant amount of EBITDA. That feels like it should warrant at least 1x sales. We’ll see if it gets there.

Sientra

I wasn’t expecting too much from Sientra in the third quarter. So I was pleasantly surprised to see a couple of positive data points: sales growth of their bioCorneum product and a tuck-in acquisition in the area of tissue expanders.

Sientra continues to progress with their new facility for the breast implant product. Their manufacturing partner, Vesta, has completed the build out of the facility and is producing test product. Sientra will submit a PMA supplement (pre-market approval for a manufacturing site change) in the first quarter and expects to be shipping product by the fourth quarter of 2017, if not earlier.

They also announced on the conference call that they received notice (just that day) that Silimed, who was their prior manufacturer and from whom all of the manufacturing issues arose, had sued the company for contract breach. I have a hard time believing there is much to worry about here since Silimed is under suspension, had their factory burn down under a still undetermined cause and obviously cannot supply product.

All of this was anticipated good news. What makes Sientra more interesting to me are the moves around supporting products.

BioCorneum is a silicon based gel that is used to prevent scarring and also to hide the appearance of scars. Sales of bioCorneum continue to improve. Revenue was $1.32 million in the third quarter. That is 20% of total revenue and up 18% sequentially.

Through the acquisition of bioCorneum Sientra has proven that they can take an under-marketed product in an adjacent vertical and apply their salesforce to increase sales. They made a second foray into this “adjacency model” in the third quarter with the acquisition of Specialty Surgical Products (SSP). SSP has a portfolio of premium tissue expanders, which Sientra said on the call is a $235 million market. They didn’t disclose sales from SSP but I suspect they are small. They did say they made the acquisition for a price in the range of 1.5x to 2x revenue. They also retain “a handful” of sales staff from SSP that will help build-out their own salesforce further. SSP products are manufactured by Vesta so there is overlap there.

Similar to bioCorneum, management said that the SSE portfolio is an “underdeveloped, under-promoted portfolio can expand with their sales staff”. Additionally, because tissue expanders are typically used in a hospital sending, the SSP sales staff is geared towards the “hospital-based reimbursement market” for reconstruction. Sientra has not sold their implants through this vertical, so there are market share gains to be made by leveraging that team.

I added a little to my Sientra position on the news.