Week 432: Coal for Christmas!

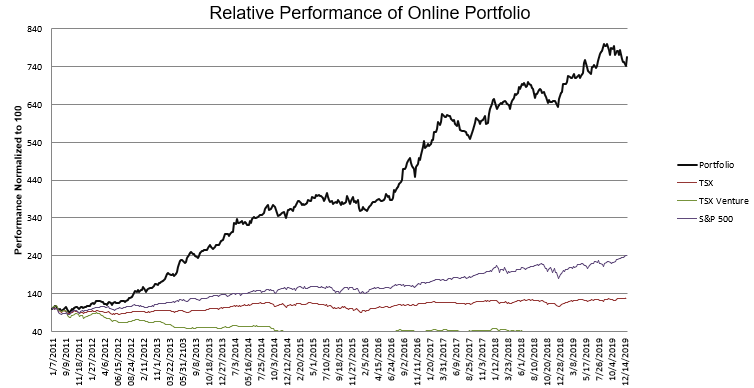

Portfolio Performance

Thoughts and Review

I have been wrong about the market. My cautious approach has turned out to be unjustified and the market has soared to new highs.

As a consequence, my S&P and Russell shorts have performed poorly. That has been a headwind. But quite honestly, it hasn’t been the problem with my portfolio.

Instead, as I wrote about in my last post, the problem with my portfolio has been bad stock picking. I’ve been smacked with 3 events, each of which whacked my portfolio and pulled it back a step.

First Nuvectra. Then Evolent. Then Mission Ready Solutions. Three events that led to under-performance in November and December.

I’ve had dry spells before, and I can only hope that the worst of this one has passed. This last week has helped, and even in these last couple days I’ve popped another couple percent from end of week levels. So maybe the worst has passed. I can hope!

On the topic of hedges, though the market is clearly in a bull run I have decided to keep them. I’ll sleep better knowing that I have some protection to the downside.

This move in the market seems to be all about multiple expansion. The S&P is at 20x this year’s earnings. Earnings growth from 2018 to 2019 was minimal – Bank of America-Merrill Lynch has 2018 S&P earnings at 161 and the 2019 S&P earnings consensus at only 163. That means that growth this year was basically nada.

While next years earnings are forecast to have a big jump (to 173), the trend has been for those estimates to come down so I would take the numbers with a grain of salt.

It is just not an environment where I want to go out on the limb. So I will hold onto my hedges and hope that my stock picking (and luck!) improves.

Evolent Health

After having played out contrary to my expectations early in December, Evolent has since worked out much more favorably – events have been back inline with my original expectations.

The whole process has been a gong show. I don’t like gong shows – they cost me profits as I get whipsawed. That happened here as I did sell the stock after the original decision by former Governor Bevins to not include Passport Health Plan in the new Medicaid awards. Then I bought back my stock somewhat higher after realizing that Bevins may be overturned and this was unlikely the end of the saga.

Newly elected Governor Beshear came into office December 10th. Six days later he pulled the plug on Bevins plan to overhaul Kentucky Medicaid.

The Bevins contracts were awarded on the basis of the Bevins overhaul. Not surprisingly, Beshear followed up with an announcement on the 23rd of December that he would cancel the managed care contracts that Bevins had awarded.

Honestly, if I had a bit more confidence, I would have gone all in on Evolent in anticipation. With the Bevins overhaul scrapped, Beshear had plenty of reason (and cover) to re-award the contracts.

I think it is likely, but not a certainty (after this last debacle I cannot use the word certainty!), that Passport gets awarded the new contract when it is announced some time this spring.

Beshear has been pro-Passport so far. He was the one that approved the Evolent take-over in the first place. I go back to his comments pre-election about wanting to get Passport’s new health campus built. There was also another community voice that was recently speaking in favor of Passport, Steve Trager, president & CEO of Republic Bank & Trust Company.

There is still lots of reason to be skeptical Evolent. They are only borderline cash flow positive and their position as a service provider to smaller health plan entities like Passport means there is the risk that in the long run these smaller players will be un-competitive with their larger competition. The Passport exclusion was seen by at least one brokerage as evidence of that. In my opinion it is all politics. But with the politics now working as a tailwind, I am inclined to stick with Evolent for now.

Nuvectra

Nuvectra is also playing out in a way that I would interpret as positively, though you would not know it from the stock price.

I’m probably missing something. There is probably some “gotcha” in the bankruptcy process that I simply am not discounting. If so, it will be a learning experience. If I’m not, it would seem that the probabilities are that Nuvectra’s net assets, on liquidation, should exceed its debt by more than $2 million (which is what the equity is currently valued at).

But we’ll see. At the very least this will be a learning experience.

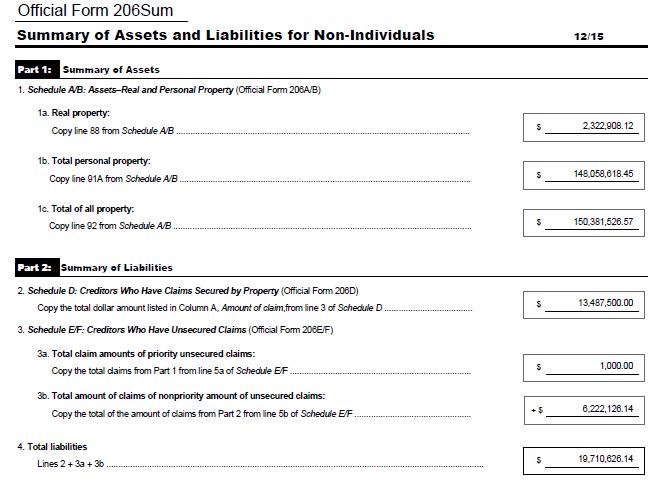

The company produced their November financial statements and a schedule of assets and liabilities. Cash levels are at the expected level. Expenses have dropped to a trickle. Most importantly, the amount that creditors are owned is in line with what I was expecting.

Amounts owned to secured and unsecured creditors total around $20 million. This isn’t too far off of the value of the assets, even before considering the IP.

The definition of what is secured debt and what is unsecured debt seems to vary. I’m not sure I understand exactly why. I’ve seen an amount of $13.5 million, $10 million or $16 million. That part is a little confusing but the overall amount of debt always seems to add up to around $20 million.

As you can see from the balance sheet, on the surface, Nuvectra’s assets far exceed the liabilities. But this is because of net-operating losses (NOLs).

As you can see from the balance sheet, on the surface, Nuvectra’s assets far exceed the liabilities. But this is because of net-operating losses (NOLs).

I have no answer as to whether there is a chance that these net-operating-losses have some value when the company exits bankruptcy.

I did notice that Sears struck a deal whereby their NOLs were preserved upon exit. Maybe it is just wishful thinking to believe that the shell that exits bankruptcy might preserve at least some of them?

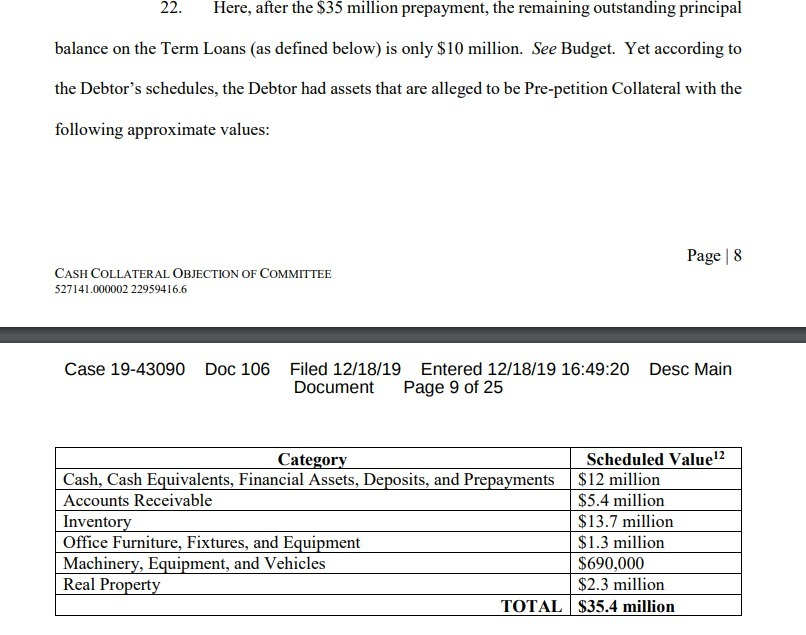

Anyway, that is not the bet here. While I’m sure that in a 363 bankruptcy auction Nuvectra’s assets will fetch less than the book value, I can’t help but think that together with the Agovita and Virtis IP the overall value should be able to exceed $20 million.

In fact, in an argument filed by the unsecured creditors, the idea was pushed that assets far exceeded debt (thanks to @Fbushek for pointing out this excerpt as well as a couple of others):

Now it must be said that the unsecured creditors were making an objection about whether the secured creditors cash collateral lien should include IP. So they were trying to paint a rosy picture.

Another consideration is that a lot of the “value” is inventory. I’m not sure what value that inventory is going to have in the 363 sale – though if the sale is what I expect – that of the Algovita product line in concert with a restructuring of the Integer manufacturing contract – meaning the product supply chain is intact, then it might be worth quite a bit.

The final consideration is that, of course, these numbers assign nothing to Algovita and Virtis, which are the primary assets of the company.

With the stock pricing in so little at this level it seems like a reasonable risk for the potential reward. I only wish I had been more patient and bought my shares here rather than up when the stock was 20c to 25c.

One other interesting point is that Nuvectra came out with their list of executory contracts they wanted to reject. Integer/Greatbatch wasn’t among them. Also, in a separate document intended to list the contracts to be retained, there was no mention of Integer/Greatbatch either.

My guess is that Nuvectra is keeping their options open for the auction. Rather than eliminate the contract, they will leave it up to each bidder to decide if they want to carry on the relationship with Integer/Greatbatch, which I would presume would mean a negotiation of some sort of new agreement (and the proposed cure costs).

Apart from these disclosures, most of the rest of the documents (and there is a lot of them) is a lot of noise. There has been back and forth between the secured and unsecured creditors arguing whether IP should be part of the secured creditors claims, back and forth about conflicts of the law firms hired to represent the parties involved, and amendments to this or that document.

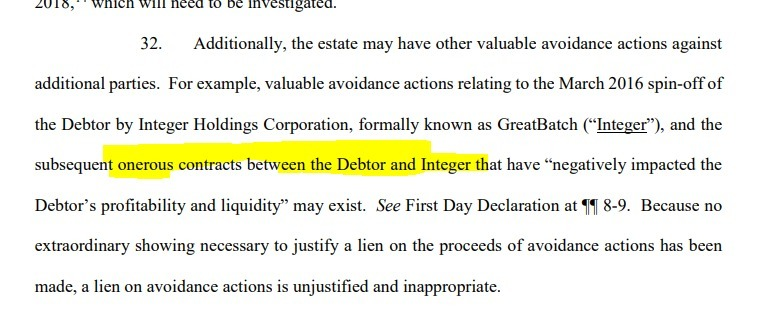

The only other point worth mentioning is something called “avoidance actions” and what that might mean. I’m still fuzzy on how this might work but it appears that avoidance actions could clawback some of the dollars paid in this contract. For example, the unsecured creditors make the following point:

Just by the fact that the assets are in bankruptcy, this contract no longer is a lead weight on the Algovita asset. As a consequence, Algovita may be worth more in bankruptcy than it was pre-bankruptcy.

The point the unsecured creditors are making is that this additional “value” that occurred due to the avoidance of the contract with Greatbatch/Integer should not necessarily be the first lien of the secured creditors. Because that value didn’t exist when these creditors signed their debt agreement with Nuvectra.

I’m not sure how meaningful the discussion is for an equity holder. At the end of the day either everyone gets paid and there is something left over for equity, or not. So how the assets are allocated between secured and unsecured creditors is an interesting intellectual exercise but maybe not so relevant to the investment case.

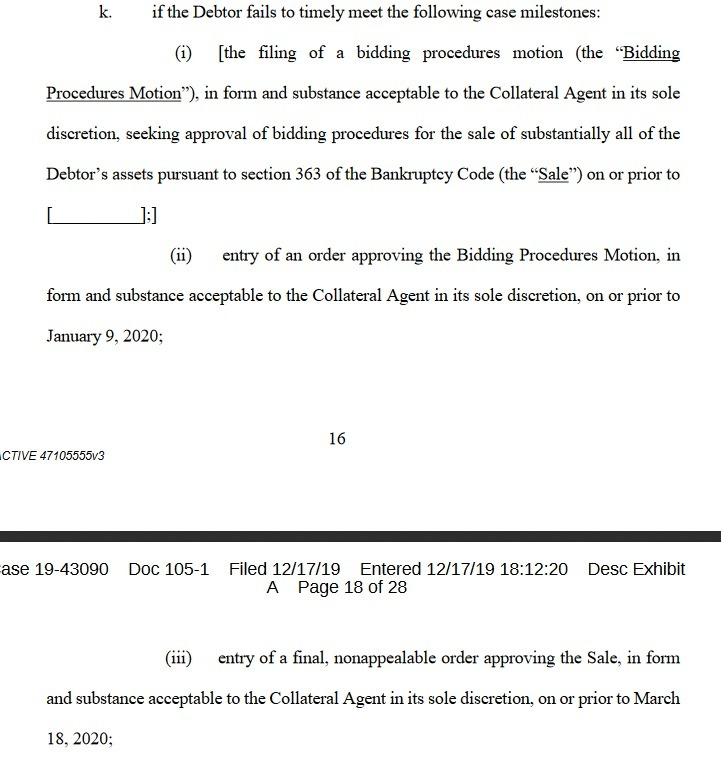

The one other thing relevant thing that has been settled is the schedule. It looks like the process will take place quickly. The plan is to have bidding procedures approved by January 9th. The auction should be complete by March 18th:

Finally, after market close on the 31st, Nuvectra released news (and they do not release much news these days) that Algovita had received full-body magnetic resonance (MR)-conditional approval from the FDA. I’ll need to dig into this a bit more to quantify just how important this is (this is a good paper describing that ~80% of SCS patients will require MRI’s within 5 years, so the approval addresses a significant untapped population), but it is reasonably important, as it means that Algovita can be applied to a wider range of pain issues and therefore the asset is presumably worth more to a buyer today than it was last year.

Finally, after market close on the 31st, Nuvectra released news (and they do not release much news these days) that Algovita had received full-body magnetic resonance (MR)-conditional approval from the FDA. I’ll need to dig into this a bit more to quantify just how important this is (this is a good paper describing that ~80% of SCS patients will require MRI’s within 5 years, so the approval addresses a significant untapped population), but it is reasonably important, as it means that Algovita can be applied to a wider range of pain issues and therefore the asset is presumably worth more to a buyer today than it was last year.

Gold and Oil Stocks

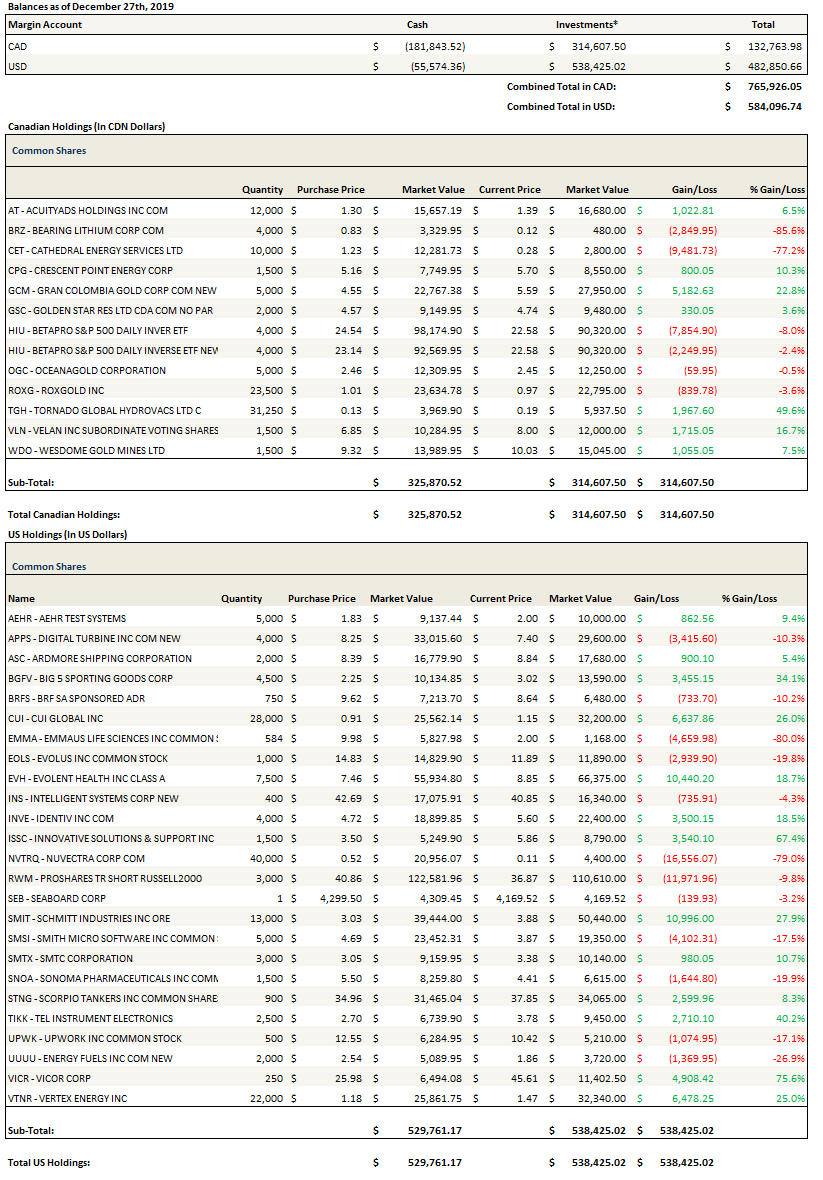

Gold stocks are making a move. I’m holding the same one’s I have been for a while and added a couple of others. I added smaller positions in Golden Star Resources and Leagold as it became more likely that gold was finishing its consolidation. I also bought back Wesdome (which I never should have sold).

My largest gold stock position is Gran Columbia. It still seems to be the cheapest of the bunch if you ask me.

On the topic of oil, I added another name to my basket of Crescent Point and Whitecap this week with Gear Energy. There is nothing fancy here. You can go onto SeekingAlpha and read all the articles about whether or not it is undervalued or overvalued compared to peers. I’m playing this at a dumber level – invest in relatively liquid names that aren’t likely to screw anything up and that therefore will participate if the sector move in Canadian oil stocks continues. I’ll get “cute” with my ideas if the move looks to be sustainable, but for now, if it is, these names will move just fine.

On the topic of oil, I added another name to my basket of Crescent Point and Whitecap this week with Gear Energy. There is nothing fancy here. You can go onto SeekingAlpha and read all the articles about whether or not it is undervalued or overvalued compared to peers. I’m playing this at a dumber level – invest in relatively liquid names that aren’t likely to screw anything up and that therefore will participate if the sector move in Canadian oil stocks continues. I’ll get “cute” with my ideas if the move looks to be sustainable, but for now, if it is, these names will move just fine.

New Positions

I took a few new positions in the last couple months that are worth mentioning.

One of them is Velan. I started writing this up for this post but it quickly became a post in and of itself so I will be posting a write-up on the name shortly.

Two others are past names I am revisiting – Digital Turbine and Intelligent Systems (da-dum!).

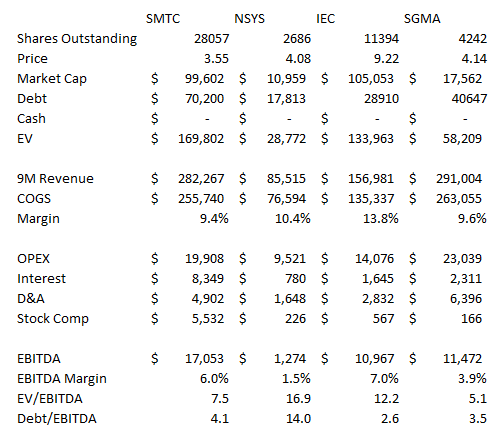

The fourth is SMTC, which I bought in December. I have been watching the company for a while and the stock briefly fell below $3, which is where I took my position.

SMTC provides contract manufacturing for semi-conductors. These are typical EMS tasks like PCB assembly, enclosure fabrication, system integration and testing. They operate out of Mexico and the United States.

SMTC competes against companies like Keytronics, Sigmatron, Benchmark, as well as the larger, well known names like Flex, and Plexis.

SMTC made a major acquisition last November. They acquired MC Assembly for $65 million. The acquisition doubled the size of SMTC. The company said they expected to realize $6 million of cost synergies once the acquisition was complete. But honestly, I do not see those synergies in this year’s financials so far. Costs appear to be up in the aggregate. I’m wondering whether this is related to integration of the two companies and 2020 will show the synergies materialize.

Their business tends to be higher end, lower run rate manufacturing where quality, flexibility and a willingness to handle lower volume orders is important.

To compensate them, SMTC gets margins that are double of what tier 1 guys are getting – 12% while industry margins are in the 6-7% range.

SMTC has a large footprint in Mexico. They had a far smaller one in China, but they exited China completely as of year-end.

The stock got hit in September after they guided down their 2019 numbers.

“In addition to the China closure, we are seeing softness in certain end-markets across semiconductor and data center expansions. Accordingly, we are updating full year 2019 revenue to range between $354 and $362 million, which excludes $16 million of revenues in 2019 attributable to SMTC’s operations in China, and Adjusted EBITDA to $25.0 and $26.0 million,” said Smith.

Admittedly, I’m not convinced about this one. My bet here was partly on valuation and partly on a bottoming of the business. If a trade truce does market a manufacturing bottom and 2020 is better than 2019, then SMTC looked like a cheap bet in an expensive market.

FWIW, SMTC guided to decent topline and bottom line growth in 2020:

We expect our 2020 revenue and Adjusted EBITDA, which will exclude any operations in China, to range between $390 and $410 million and $29.0 to $31.0 million, respectively

The midpoint of guidance puts the company at 5x EBITDA on next years numbers. This compares favorably to their closest competitors but since I bought the stock I looked at larger competitors like Flex and Sanmina and they trade at similar or even lower multiples (Flex trades at 4.2x EV/EBITDA on 2019 numbers and 5.5x on 2020 estimates).

I might have been too quick to pull the trigger on this one. It is not as cheap as I originally thought and the benefits of the acquisition have yet to materialize. Nevertheless I’m sticking with my small position for the moment. It seems like the company should have economic tailwinds if trade is bottoming and they should be past any acquisition integration hiccups. 2020 might be a better year for the stock.

Portfolio Composition

Click here for the last ten weeks of trades.

{kind=link}