I decided to make a number of changes to my portfolio today.

I wrote on the weekend that I hadn’t really changed much leading into the invasion of Ukraine, other than adding a bit more on the hedge side. I think that is because the uncertainty of the situation has taken a while to sink in for me.

So today I changed tact. I sold a lot of stocks. And I bought a few others that are tied to the commodities Russia exports.

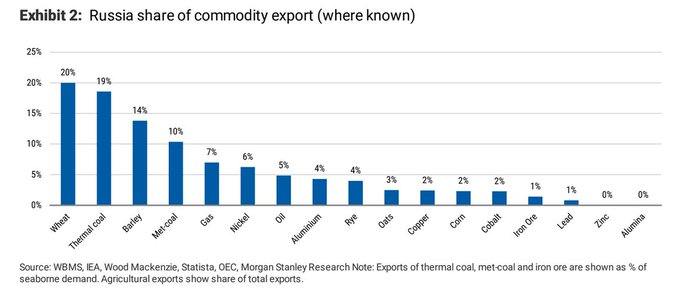

What sparked this was a search through the brokerage document database I have access to. I started searching for the word “Russia”. I quickly came across documents that showed just how large its influence on various commodities was.

I don’t think I realized just how big of a commodity exporter Russia is. And that really got me wondering how this is going to ripple through the world economy.

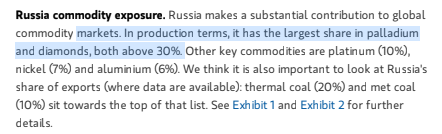

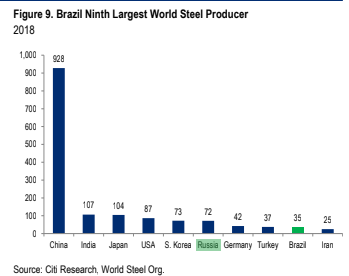

At the end of this post I’ve snipped a bunch of the tables and charts I found. Russia is just such a big player in the export of so many basic commodities. And then on top of that Ukraine is a large grain exporter and they actually export a fair bit of other commodities as well – steel for example.

I was already on edge about market exposure. So when the market almost got to even today, I said to myself that I would be crazy not to take this opportunity to make wholesale changes.

I sold a lot of my bank positions and a lot of my biotech positions. I now only own a little BCBP, a little BSVN, and a bit of a few biotechs trading well below cash. I added to my index short some. And then I added some small-ish commodity stock positions like Stelco, Algoma, Peabody Energy, and Diamcor Mining (Russia is 30% of the diamond industry!).

(Note: I also bought JJG, the grain ETF, and added a little to BIOX. I forgot those ones in the original post).

None of these long positions are very big. I just thought if I’m going to have some long exposure, this seems to be the place to do it.

My basic thought here is that A. I have no idea how events are going to unfold but B. It seems unlikely that something will happen in the near-term to lift the sanctions that are going to impact all these commodities that Russia exports. I guess what I am saying is that while I don’t know what the world will look like tomorrow or next week, it is hard to imagine a fast return to status quo.

That said, let me emphasize – small positions. I tweeted today that the “best advantage a tiny retail investor has is ability to just sit it out”. I did that during COVID and I made a pretty big move in that direction today.

This is all just to hard to figure out. I’d rather stand aside and wait.

I don’t really think the market rally on Thursday and Friday is based on sound footing.

The rally is being led by all the same stocks that are in the middle of a triple waterfall decline. It seems to be being driven by a combination of very over-sold conditions, having some “relief” that the invasion is now upon us and not just a foreboding specter on the horizon (a thought that makes me ill), and the expectation that this will slow the Fed tightening.

It just doesn’t ring true to me, not with this disaster that is unfolding. The only one of the 3 points above could produce a lasting rally is this: if the Fed stopped tightening (though it hasn’t started right?).

Whether or not the war in Ukraine puts the Fed on hold, I don’t see how it is not going to make inflation worse. It is going to make shipping more arduous, make food prices go up, make energy prices stay up. And if the Fed does decide not to act, won’t the bond market eventually do it for them?

So I’m staying very cautious. I’ve avoided the slaughter so far, and this does not seem like a good time to change tact.

That said, I’ve made a few changes to my portfolio since I last wrote. Not too many, but a few.

The biggest change I made was to sell my gold stocks on Thursday. Pretty much the whole lot – I still own a little Calibre Mining (this was my old Fiore position) and Superior Gold, but that’s it.

Partly, this is sentiment driven. I saw the big red candle developing after the invasion announced and I know enough about gold to realize that big red candles are rarely shrugged off. As gold stocks sold off during the day on Thursday, I sold mine too.

I might buy back but I’m not really sure how this plays out. The thing that worries me is that with the sanctions being announced, the one thing Russia can sell is gold. Gold bugs can argue all they want that this is a good thing, that it justifies gold’s place as a reserve currency, but it seems to me that selling is selling.

Other than that, on the long side I added a small position on Diana Shipping, which so far has worked out, a position in Copper Mountain, and I should have added to Rada but I’m an idiot. Oh, and believe it or not I actually added a SaaS name – Alteryx!

Don’t get me wrong, I am still more short SaaS/momentum than long. Thursday-Friday was a bit painful in that regard. But Alteryx is something foreign to the SaaS world. A company that raised growth guidance to ~30% and has a low (6x) Price/Sales ratio. I might be wrong, Alteryx may just be a bad business. I’m still trying to figure that out so I won’t say much else about it until I do.

One-Hit-Wonders

But the short-SaaS/momentum story feels like it is getting old. Yesterday’s news. I am moving away from those shorts and towards some other, more industrial, shorts instead.

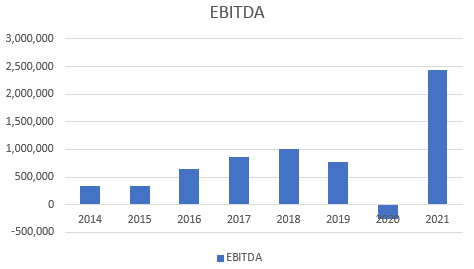

It strikes me that there are a lot of businesses, where if you go back and look at cash flow and EBITDA over a 10 year period, there has just been this massive spike in the last year and a half that is completely unprecedented. And the more I think about it, the more I think this is a bubble itself.

It is not a “valuation” bubble. These stocks tend to trade at less than 10x EBITDA, sometimes well under that. Single digit FCF in some cases. But I think that might be because the bubble is in the business instead.

Consider Olin. I owned the stock for a bit last year. But I got to thinking, in part because the price action seemed so poor, about whether this was really sustainable. Take a look at how Olin’s EBITDA and FCF compare to prior periods.

While I would love to believe that Olin is in a new paradigm, I have my doubts. And Olin is far from the worst in terms of the one-hit-wonder factor. There are far more egregious offenders. All the building material companies, the retailers – particularly the sports stores (remember BGFV?), steel, maybe even aluminum eventually. The list is very long.

While the triple-waterfall SaaS and momentum collapse gets all the headlines, these sorts of names look suspiciously similar to me.

Vidler

With the Ukraine situation so fluid and just so awful, I’m going to go in a completely different direction here and talk (again) about a stock that has a thesis untied to most of this geopolitics.

This is the routine that I have every morning since mid-November:

Get up and go downstairs

Put on the coffee in the coffee maker

Get the coffee and go to my workspace

Open Chrome

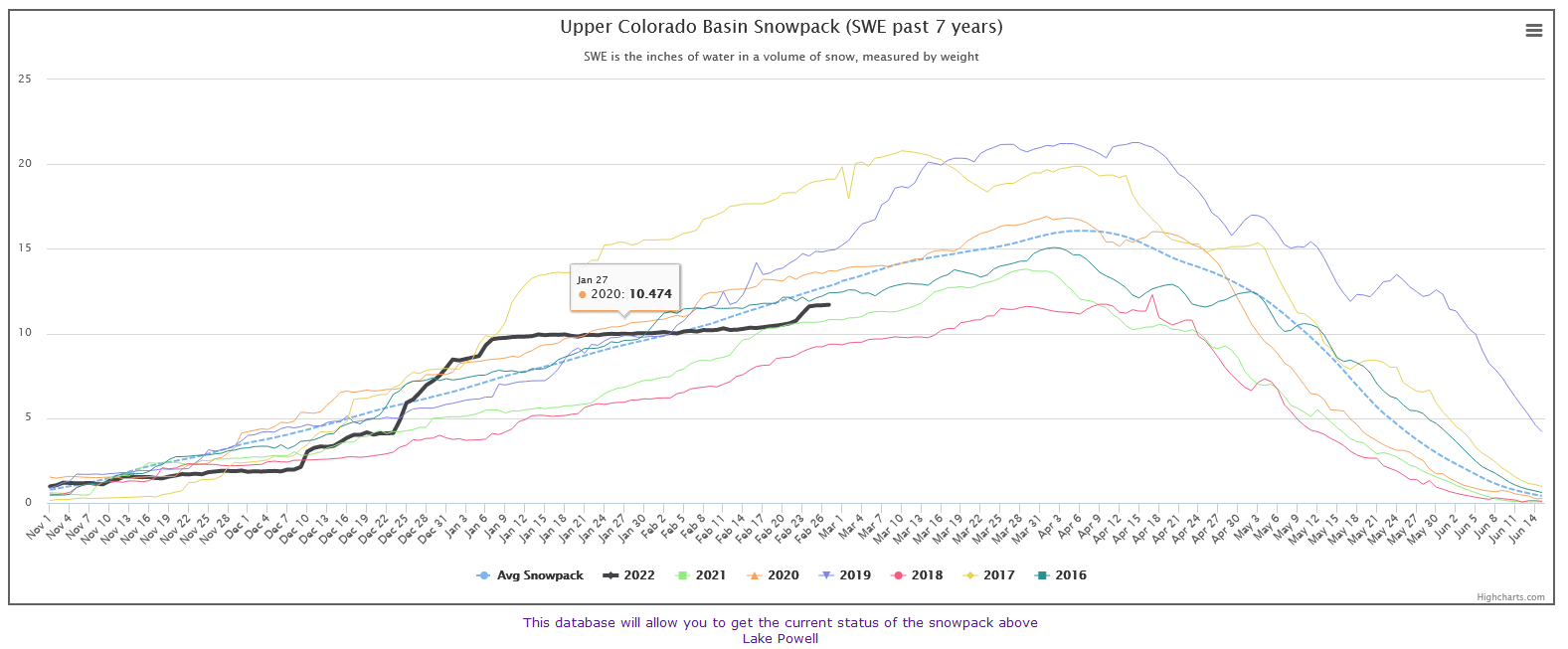

Check the snow pack of the Upper Colorado Basin.

The irony is that I don’t live anywhere near the Upper Colorado Basin. I’ve never been to the Upper Colorado Basin. But for the last 4 months it has been the most important piece of data for me.

I wrote about Vidler back in early December. It was then and is again my largest position. If you follow my portfolio though, you’ll notice that for a few weeks I sold some of the stock, and then bought it back.

That sale and repurchase relates to this chart:

Wouldn’t you know it that about a week after I wrote about Vidler, the Upper Colorado Basin had the biggest snowfall that it has had in years.

Through the Christmas break I was sweating bullets. Every day I’d watch the snowpack rise. And I’d get more nervous.

I’d get nervous because at the end of the day, Vidler’s near-term stock price is all about drought. While the long-game is water shortages accruing over decades, over the short run the stock price is about whether there is a problem right now.

Investors care about what happens next quarter or at most this year, not what is going to happen over the long-run. While Vidler’s sale of water in December is a big positive, at the beginning of January I was not convinced that Vidler’s stock would do well if we saw a record snow pack in the Upper Colorado Basin. If Lake Powell and Lake Mead began to rise significantly, and investors began to look at the story as an “eventually” and not an “emergency”, I feared the stock would be re-rated down.

So I reduced my position in Vidler by about 1/3, to a point where I slept better with that concern. And I waited to see just how much snow would fall.

I waited. And I waited. Just as the amount of snow that fell from Christmas Eve to New Years Day was nearly unprecedented, the lack of snow since then has been equally unprecedented.

We did have a blip of snow last week. But even so, the Upper Colorado Basin snow pack is now below the 5-year average. And that 5-year average is not a good baseline – it is the baseline of a drought.

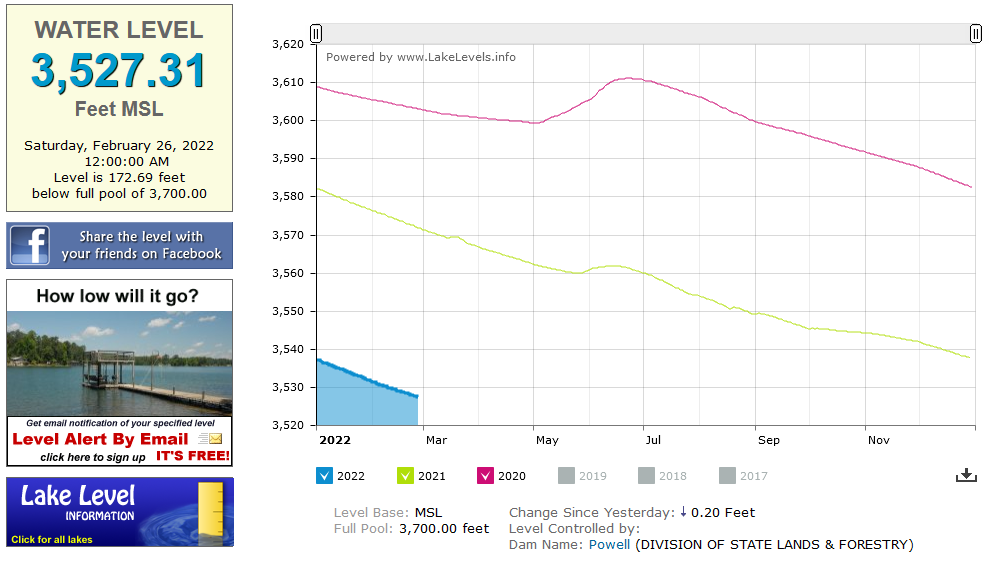

We are starting to see the articles pop up again. This article from the Colorado Sun says that projections for Lake Powell are too rosy.

In the article, they point out that “Ten or 20 feet can make a big difference at Lake Powell these days. Water managers are closely watching whether the water level will drop below 3,525 feet above sea level. If it does, it threatens the ability of Glen Canyon Dam to generate power.”

Lake Powell is 2 feet away from that level right now. And it is going down every day.

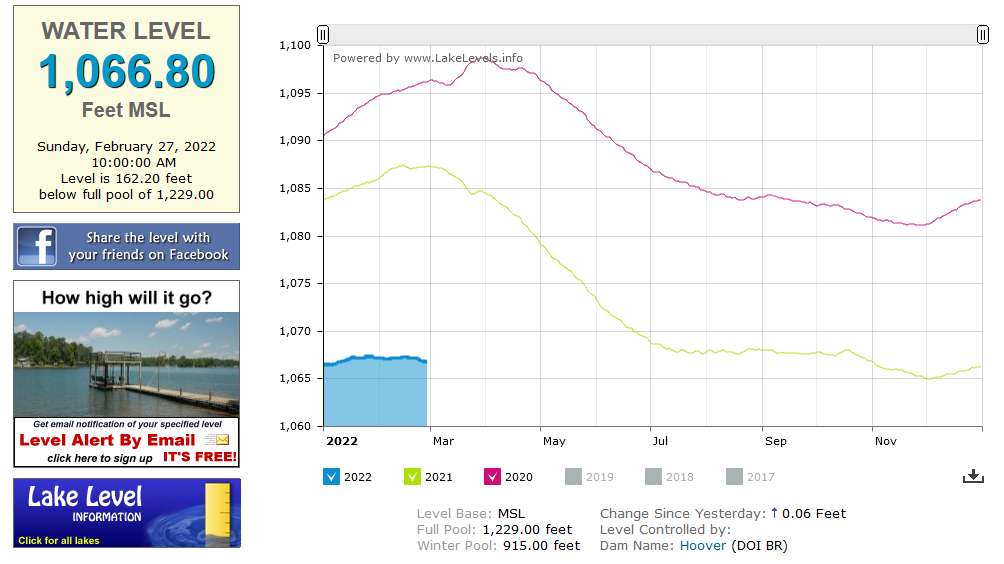

Lake Mead is no better. The usual winter bump has basically not happened this year.

The other thing about this article is that it is about the models, and how the models aren’t predicting accurately. I find that interesting. This is a case where the models are painting the picture that everyone wants to hear. So it kind of makes sense that no one (up until now) is questioning them. This isn’t the first time I’ve read that the models are too optimistic. It has come up here and there. And I really wonder if the problem here could be much bigger than anyone has admitted, because the consequences are so severe.