Week 141: Portfolio Allocation

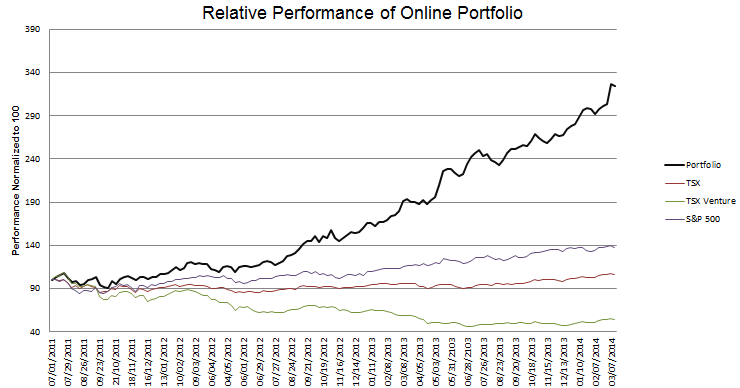

Portfolio Performance

See the end of the post for the current make up of my portfolio and the last four weeks of trades.

Recent Developments

I’ve been on vacation and so am a couple weeks late getting an update out.

My portfolio had a big move up, thanks mostly to the movement of Pacific Ethanol and MagicJack. Pacific Ethanol had a one day gain of 67% last Thursday, and is nearly a 4-bagger since I bought in. MagicJack is nearly a double.

But what has really helped is that even before the run-up Pacific Ethanol was my largest position. MagicJack was my fourth largest position.

One of the ironies of writing about the stocks I own, is that what I write about most is often not what I have the biggest position in. The stocks I have the most to say about are the one’s that are on the cusp, where I am constantly debating whether to hold on to them or not. My biggest positions; Pacific Ethanol, Yellow Media and MagicJack, for example, I have written only a single post about. That post states the thesis, and as long as that thesis is valid I don’t have much else to say.

Yet the stocks in my portfolio are far from being of equal weighting. I usually have a lot of stocks. Unless the market is going down, the stocks number at least 30 and has recently approached 40. But most of the positions are quite small, in the 1-2% range. These as starter positions; enough to keep me interested and following the company, but not enough to hurt me too much. If my thesis for these companies plays out, or if, as I learn more I become more comfortable with the idea, I add. If not, if the company materially lags or sometimes if time simply passes and I lose interest in the idea, I drop the position and move on. Read more