Some Thoughts on Aluminum, Steel, China, Carbon and SaaS

I’ve been on a commodity kick since sometime in April. Back then I started talking about the greening of commodities and what that might do to prices. I bought some stocks at the time on that premise.

These picks have been a mixed bag. My investment in Stelco has worked out well, but Legato Merger Corp (Algoma) has not really done much. My copper stock (Atico) has not worked out at all. My tin stocks (Cornish and Alphamin – the latter I forgot to buy for the tracking portfolio so it isn’t there) have done okay but not great.

I think though that my biggest mistake has not been sticking with aluminum.

In May when I was whole hog into the idea that green initiatives were going to drive up metal prices, I targeted steel and aluminum as the two main beneficiaries. I bought two stocks – Stelco for steel and Alcoa for aluminum.

Aluminum was interesting because aluminum is not really the same as other metals. Don Coxe used to call aluminum congealed electricity. Which is to say that aluminum does not feel the scarcities of mining (bauxite is plentiful) and (up until recently) electricity has always been abundant.

Nevertheless I was taken by comments like the following, which comes from Alcoa’s Q1 conference call. I thought that maybe this time would be different:

After I bought both of these stocks subsequently went down. I got a little nervous and decided my conviction lay more in steel than aluminum. In large part I was spooked by aluminum’s history of not really participating in commodity bull markets. So I sold Alcoa.

That was a mistake.

I sold Alcoa at $35 (I bought it at $40). While it did go down further (to around $32 at the bottom), it since has risen right back up to $48.

What is a little frustrating about that move is it has been exactly for the reason I suspected.

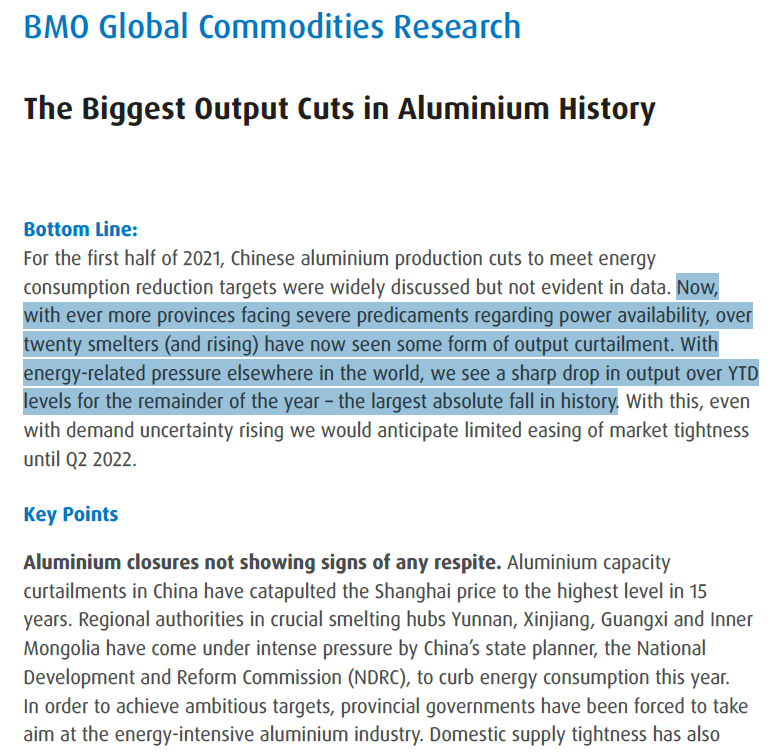

Witness the following BMO report from a couple weeks ago:

Steel has gone up too. In fact here in North America steel has stayed very strong. But steel stocks – not so much. I attribute that to Evergrande.

I have continued to post relevant stories on commodities on the RNO board. There are some pretty mixed to negative signals about China. Chinese real estate is up in the air and then on top of this we are finally seeing the impact of China’s carbon policy.

On the real estate/Evergrande front, as far as steel goes, I am torn. Obviously a slowdown in construction in China is not good for steel demand. But at the same time, I know that steel is 12% of China’s carbon emissions and China wants to cut carbon. So is China just going to use this as an opportunity to close high-carbon emission steel mills? I can’t really see China flooding the world with excess steel if one of their primary goals is to cut emissions.

A lot of the articles and research I post on RNO have to do with China’s carbon initiatives. Back in May these were rumblings – that China meant business and that they would be clamping down on dirty industry.

Now it seems to be happening. I’m reading about the closure of aluminum smelters and steel mills as provinces look to limit energy consumption to meet the green goals the government has put in place.

It is also impacting your run-of-the-mill mom and pop factories that manufacture all the crap you get at the dollar store, Walmart and the like. That is particularly interesting in terms of what it means for inflation in the short-run.

As for Evergrande, I stand by my initial assessment that A. no one really knows how this turns out, and B. Evergrande is more symptom than cause (a phrase that I have now heard from both Hedgeeye and Larry Summers since I wrote it – I don’t think they read the blog).

But what I will say is that everyone that is a generalist observing Evergrande seems to dismiss it as overblown. And everyone who is closely involved with Chinese business and investment says this is complicated and tricky. I’ll go with the latter here.

I didn’t buy Alcoa but I bought some Century Aluminum yesterday at the open. I also added to my position in Spartan Delta, my main natural gas play, yesterday and took a position in Cardinal Energy last week.

But other than that, I’m just sitting pretty cautiously positioned. If it had not been for a big move in Aehr last week I would not have participated in the rally last week at all.

I’ve gone short a few China related stocks (one is NOAH, the other OTIS). I’m still short some China indexes, though that has not worked out so far.

And I am short a few SaaS names.

I looked at SaaS two weeks ago and honestly, even for SaaS it seemed insane to me.

I have a consistent method that uses discounted cash flow to value the basket of SaaS names I follow. I just plug in new numbers and the new estimates and see what I get. While I don’t think DCF is very useful quantitatively with these names (I mean they always trade way above the number I get) it is useful for historical comparison. If I use the same model over and over I can see how the SaaS names are valued compared to how they were before.

What I was blown away with was how most of these companies (TEAM, HUBS, OKTA, PAYC, SQ, etc – all the usual suspects) are more highly valued than I have ever seen them. It is crazy. It was the first time I was getting DCF numbers that were less than half the share price. I mean, I always get numbers that are 20%, 30% or so less, but 50%+?

I shorted some of these last week and by Friday I was wondering if maybe they just won’t ever go down again. But yesterday’s move gave me hope again.

I am reminded of that Super Mugatu Real Vision interview from a few years ago. He was saying you have to know what you own with SaaS. And what you are now owning is largely a levered bet on rates.

These companies are all valued on the terminal value of their business. That means the value of the business years out, once growth is a bit slower and they are making oodles of cash on their customers, is what drives the value of the stock.

The value of earnings that are a long way out depend the discount rate that you use to bring those earnings back to present day value. When interest rates go down, the value of those way-out earnings go up. The argument has been made by others that some or much of the SaaS move is simply because interest rates have fallen so much.

But this also works in reverse. Now we have natural gas prices going up, energy costs of all sorts really going up, China doing things that could send other prices up at the same time SaaS valuations are the highest I have ever seen them. Oh, and rates have almost never been lower.

Hmmm… SaaS is never one to overstay your welcome with on the short side, but every dog has their day.