It is a little hard to write about the commodity investments I am making. Because I am just not sure yet – about the short term.

The long-term trend to me is clear – and it is all about carbon. But whether this is the right time to be buying some of these names – I have less confidence in that.

Right now I own some copper, some tin, some steel and a few shipping stocks. All of these names have had big runs already, and they have all pulled back. But most are way above their historic levels, and so they could pull back a lot more.

So I am more cautious than bullish right now.

But at the same time, these stocks are trading at extremely cheap multiples if you think that the price of the underlying commodity can hold these levels.

I bought Atico Mining a few weeks ago – it is at around 2x cash flow with copper that this level.

Or take the shipping stocks I own. Euroseas 2022 EPS is projected at $6.50 per share – the stock is ~$15. Navios Maritime Partners 2022 EPS is projected at $11.45 next year. The stock is ~$26.

And yes, I know, commodity stocks are to be sold when the multiple is low. And yes, with respect to shipping, management will inevitably destroy any shareholder value they create during the cycle, so even more buyer-beware there. Nevertheless, as I’ve been posting on IV, there are reasons to see the glass half full.

Steel is another sector with crazy low multiples if you believe in anything close to current prices are sustainable (current prices are a little more than 2x their average over the last 3 years).

On their first quarter call Stelco put the following statement on one of their slides:

On the call Stelco management said that if they generated $2 billion of EBITDA, that will convert to $1.4 billion of free cash. Stelco has an EV of about $2.9 billion right now.

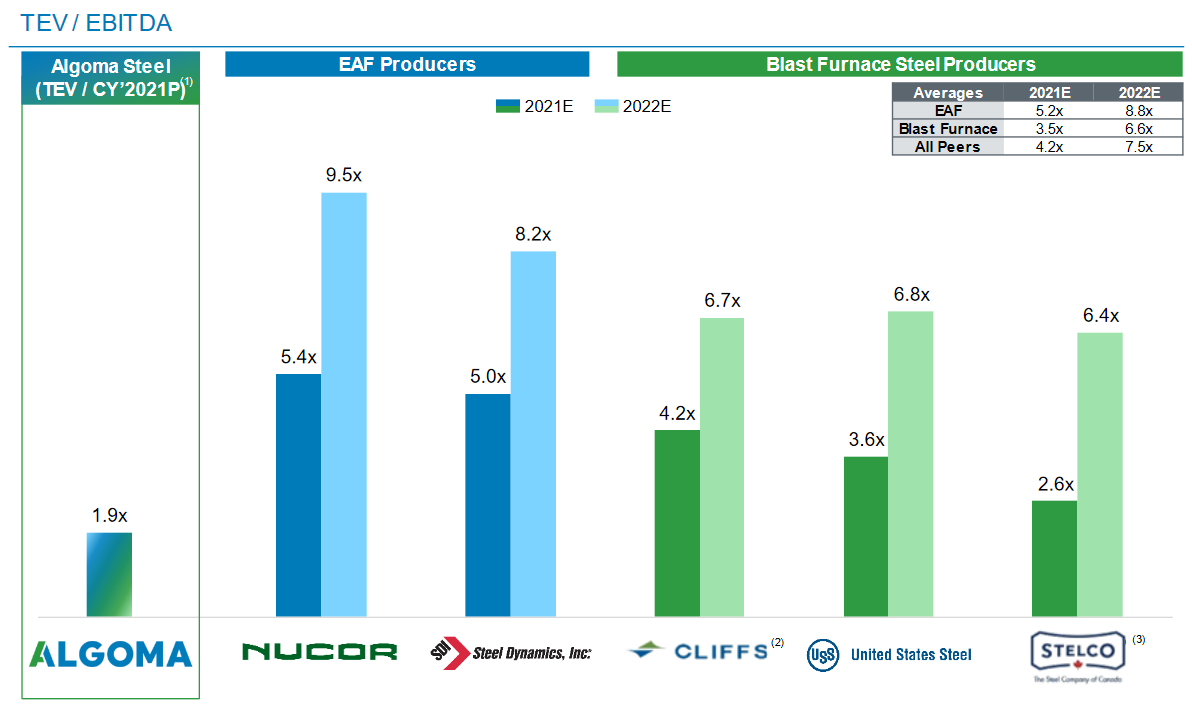

I thought wow, you can’t get much cheaper than that can you? Well, it turns out that you can at least come close. Last week Algoma Steel decided to go public via a SPAC deal with Legato Merger Corp.

The combined company will have at EV of $1.7 billion, which includes cash of about $300 million and net debt of $200 million.

Algoma expect $900 million of EBITDA this year with the assumption of $1,250/t steel. Stelco’s was based on the H2 forward curve, which was at $1,500/t. So I think that Algoma is actually a little cheaper than Stelco if you were using apples to apples pricing.

Algoma is also getting a cash injection that they plan to use to build out an EAF furnace. EAF steel makers use scrap instead of iron pellets and coking coal to make steel. They trade at larger multiples – Nucor, the biggest EAF steel producer in North America, gets a crazy 8x PE multiple!

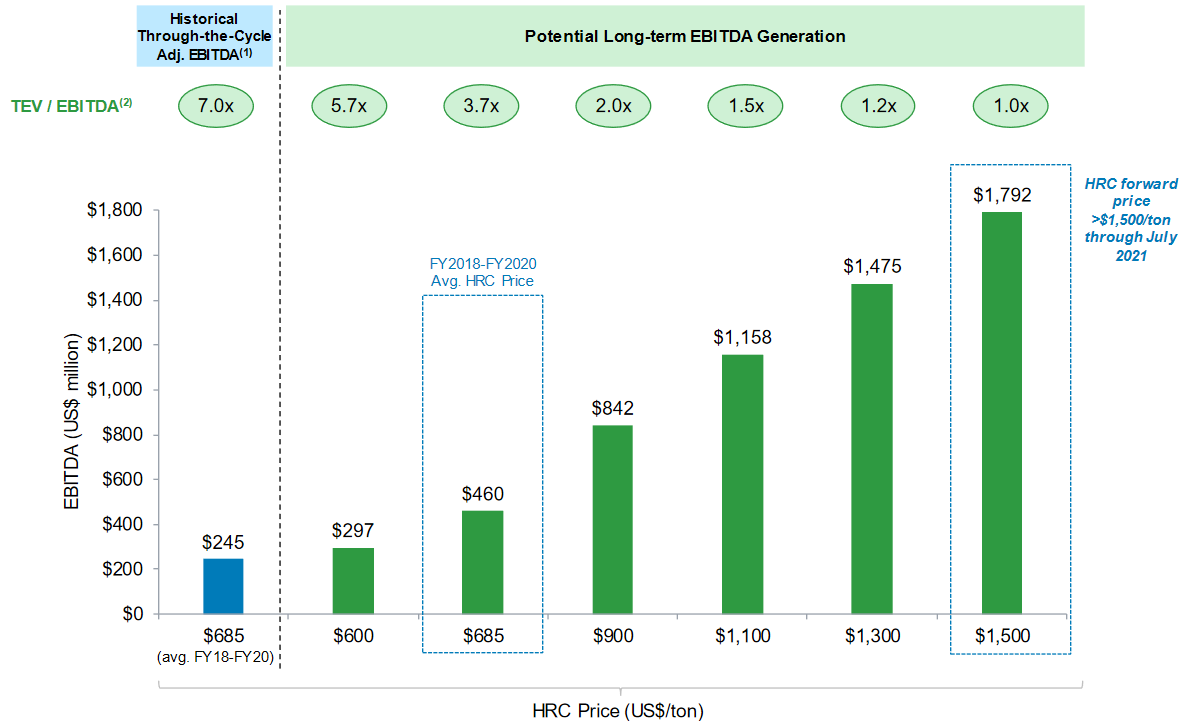

When Algoma finishes their EAF conversion they will be producing 3 million tonnes of steel (versus ~2.4 million tonnes now) and they will be doing it more cheaply. Algoma gave estimates of what their EBITDA multiple post-EAF conversion would look like at various steel prices:

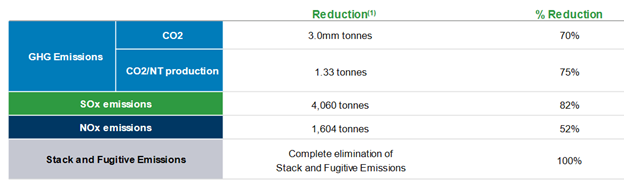

But Algoma told us something else about their EAF conversion that in my opinion is even more important than how profitable they could be was it is done.

They told us how much carbon will be reduced.

I am not sure of very much yet with this commodity cycle but the one thing I am convinced of is that it is going to be driven by carbon. The changes we are going to make over the next 10 years are going to be massive. And they are going to have an equally massive impacts on commodities, both good and bad.

Look at what Algoma is saying. They plan to reduce their carbon emissions by 70%, by 3 million tonnes, by converting to an EAF.

But you might say – so what? Well, in 2030 we are likely in a world of $150 per tonne carbon. $100 per tonne is guaranteed. Those 3 million tonnes are worth $300 million to $450 million a year.

So what happens to those Chinese steel producers, those that are far higher carbon emitters than Algoma? I am convinced that the EU is going to put up carbon tariffs at some point. The US and the rest of the west will eventually follow. They won’t have a market.

The Chinese are not making overtures about shutting down steel mills by the end of this year because they are altruistic. They see the writing on the wall. Those mills are going down one way or another. They go from low-cost producer to uncompetitive in a world where carbon is priced accordingly.

So I’m not sure what the price of steel is going to be next year. Probably lower than it is now. Same with copper, same with container ship pricing. But I am getting more sure that in the long run some of these commodities are going maintain the levels that we are seeing and maybe even go higher. In fact its possible that the market, which has run up these commodities to heights that I don’t think anyone expected, is telling us just that. Because pricing carbon changes everything.

I am losing money. And I couldn’t be more excited about it.

I say that tongue in cheek. But both statements are, in fact, true.

First, I am losing money. I have had a rough couple of months.

The culprit? That damn Canadian dollar.

The Canadian dollar has risen ~5% in the last month and a half. Depending on the account, I had between 1/3 to 2/3 of my cash in USDs. So I have taken a 3%+ hit on currency. In the tracking portfolio I use for the blog, I am over 80% USD. That puts me down over 4% on CAD!

Losing money sharpens the mind. On Monday I said enough. I sold all my large-cap USD stocks and moved the money back to Canadian dollars. I sold Amazon, Facebook, Eli Lilly, Bristol Myers, and Ford (which I had bought but never got a chance to talk about).

Why? If the CAD keeps going up, it is too big a headwind. If the Canadian dollar goes to 90c then these US listed stocks need a 10% gain just to break even. If it goes to par, they need 20%. That is a bad risk/reward.

But what if this is the top? I mean we have had a relentless move in the USD/CAD from 1.45 to 1.20c, including this blow-off 5c move over last 6 weeks. Maybe that is the end of it?

I am just not convinced this is going to end.

For the last couple of weeks I have been watching the Canadian dollar and thinking that something bigger was going on.

It does not want to go down. You can just feel it from the way it trades. It has had plenty of opportunities to correct. It has chosen not to. We had a bad employment number, we have had announcements of lockdowns, we had so-so economic numbers. The CAD kept saying – “I don’t care”. Even on days when oil is down big, usually these are days where the CAD follows with big down moves, but lately I’ve noticed a more lethargic response.

So I keep asking myself what is going on? And of course there is only one thing it could be. The only reason that the Canadian dollar ever goes on a sustained uptrend.

A commodity boom.

Yes I know what you are saying – well duh – corn is $6, copper is $4.50, steel is $1,500, iron ore is $200.

But those prices do not necessarily mean a boom. They could be transitory. Like the Fed (and Cathie Wood) say – a blip as we replenish inventory after the pandemic.

That is what I thought was happening. I didn’t really give much consideration to rising commodity prices in March and April. I was like “Sure, whatever. This is just another manifestation of the same speculative fever that is driving up Gamestop and ARK.”

But then Gamestop fell. ARK fell. All the high flyers fell. Commodities didn’t. Moreover, neither did the Canadian dollar.

So I started to capitulate to the idea that maybe there was something to this. I just didn’t know what. The charts were telling me that something was happening that was bigger than just speculation. I waded in a few weeks ago and bought the Ag stocks.

Last week I followed it up by buying into a few base metal stocks (copper and tin). Then this week I bought two steel stocks.

Steel stocks? I must be crazy right? Steel is forever a horrible business. These stocks are just off multi-year highs. I mean this is going to be a disaster right?

It could be. I have to admit that even though these stocks have moved significantly, we are only a few months into the move. The “signal is weak” as Hugh Hendry says. It could just be a blip.

But it feels like a signal. One which compelled me to get my foot in the door.

I think it could be telling us that significant changes are happening.

What changes might those be? Well… let’s use steel as an example.

China produces nearly 60% of the world’s steel. Much of it is dirty.

But the world is changing. Emissions are starting to matter. Plug Power didn’t go up 20x last year on smoke and mirrors. Sure, there were smoke and mirrors, but there was also a recognition that dirty is going away and clean is going to rule.

China recognizes this. Maybe it is because they honestly care about improving the environment. Could be. It could also just be that they don’t want to be left behind.

The EU is already talking about how they may restrict imports from “dirty” producers that have weaker carbon mandates. China sees the writing on the wall. Change or the world will change without you.

For the first time it looks like China is not just paying lip service. They shut-down 7 steel mills in Tangshan in April. I read that in Tangshan they are forcing the shutdown of 30-50% of steel production by year end. If they did that across China it would be over 500 million tonnes of steel.

To put that in perspective, Nucor produced a little over 20 million tonnes of steel last year.

I think this is just the beginning. The “greening” of commodities is one of those themes that just feels right to me. We already know that some commodities (like copper) are going to see big increases in demand from the greening of the world. And now we are beginning to see how others (like steel) are going to be greened themselves.

I mention steel but you can go through the list. Aluminum production (again over 50% coming from China) is very dirty. And what about nickel? Indonesian nickel in pig-iron, which has a horrible environmental footprint, has been the elephant in the room of western nickel producers since 2008. And rare earths – OMG I read an article last year about Chinese rare earth production – it is an environmental disaster. Yet its like 80% of worldwide production.

What if the world starts saying no way. What does that mean for commodity prices?

You can see how this could be a very big deal. And this is the sort of situation where price takes a back seat. It just doesn’t matter. If we have to accept $1,000+ steel or $10+ nickel in order to save the planet, do you really think that any country is going to balk?

So look, I may be buying close to a top. This last week has been a week of correction even as the market roared higher. I am trying to start small to get my foot in the door, and I plan to add if they strengthen to higher highs.

I just remember at the end of 2001, when I was a brand new, newbie investor right out of university reading my Dad’s Donald Coxe Basic Points publications. Coxe was showing all these charts of commodity producers like BHP and Rio Tinto and saying this was just the first movement of the symphony (he talked like that, which is great).

And so I bought Aur Resources. This was a copper stock. This was really my first, ever bet on a stock – like the first time I did the work, made a spreadsheet, and didn’t just act on a tip or something.

I bought Aur at over $3. I remember I was very worried. Because Aur had been like a $1-$2 stock not long before. And here I was buying it after a move to $3.

Sure enough, in the first few months Aur corrected back. I was distressed. But Donald Coxe kept saying, ignore the noise and buy more because we are about to have something big.

So I did. By 2003 Aur Resources was my largest position. The stock was $4. Then $5. Then $8. By 2007 it was bought out at $40.

I may be totally off base on this. It is still so early, it is hard to know if this is truly a tectonic move and not just a blip. But if I am right then we are at 2001 or 2002 in a game that didn’t end last time until 2008, and probably would have went straight up until 2012 if the US hadn’t imploded their housing market.

That’s why I am not staying on the wrong side of the Canadian dollar. And why I’m actually pretty excited even though my portfolio is not.

I can’t get over the move we are seeing in ag prices.

To think that corn is over $7 a bushel right now. Its pretty much a parabolic move.

My first foray into agriculture was in 2006. Donald Coxe, who I followed closely, became a huge agriculture bull. I did extremely well buying fertilizer stocks, seed stocks and machinery stocks. Then 2008 happened and the party ended.

I made a second foray into Ag from 2009 to around 2012. Again, a sustained move that lasted a few years.

I learned from Donald Coxe not underestimate the duration of a bull market in ag. You don’t see this kind of move unless there is something tectonic going on below the surface. Something that will last 2 years, not 2 quarters.

Corn acres in the United States came in well below early expectations while soybean acres beat only modestly. I see estimates from January that there would be 95-97 million acres of corn and 87-89 million acres of soy beans. The latest estimate right now are showing corn coming in at under 93 million acres and soy beans just over 90 million acres.

In Brazil there are drought conditions that are not looking good for their corn crop. And in Canada, I can attest to the fact that moisture this year has seemed low.

What could go wrong? Well for one, a lot of buying is coming from China. They are restocking and dealing with rebuilding their swine herds after the last bout of African swine flu and that demand might be transitory. China loves to blindside the market by stepping away if it’s in their best interest.

Never underestimate the ability of the North American farmer to squeeze more yield out of the same acre.

And is this (and every other inflationary force) a one-time global restocking after the pandemic that will end in a couple quarters?

Picking Ag stocks is tricky. There is interplay among Ag commodities – what is good for corn is bad for chickens, bad for soybeans but often good for wheat. Ag stocks often have a finger in many pies so you really have to be careful with what you are buying.

The two things I felt most sure of, at this early stage of my research, are that A. there is going to be more demand for fertilizer and B. farmers are going to do very well.

So I took a couple mid-cap positions.

I bought Mosaic and Nutrien, which are fertilizer plays (though Nutrien is diversified beyond fertilizer). Mosaic has the best leverage to potash (other than Intrepid Potash, which I looked at and based on the earnings reaction today maybe I should have bought instead). And I bought Ag Growth International, which should benefit from increased farm income. I’ll talk about Mosaic and Ag Growth for now.

Mosaic

I have always loved potash stocks. I know the nutrient has its limitations – it is not as necessary as N and K and so farmers (and countries) can balk and walk away if prices rise too quickly.

But from what I’ve read the potash producers have some cards in their favor. India just signed a surprise contract at $280 per tonne, $50 per tonne higher than the previous agreement. Port inventories in China are low. And of course grain prices are high.

Spot potash prices in Brazil are already $330 per tonne.

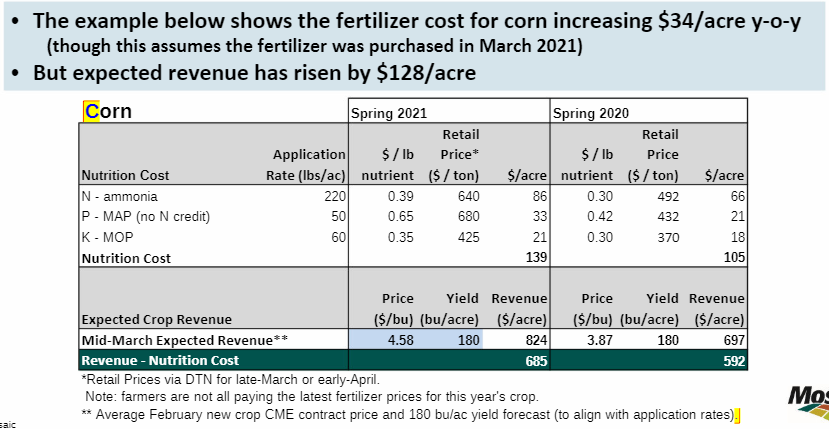

Mosaic put together the classical “bull case for fertilizer” slide in their March presentation.

Simply put, the bull case is – yes fertilizer prices are up but grain prices are up even more! And you presumably should get a better yield per acre with better fertilizer application.

Mosaic will benefit. They own two potash mines in Saskatchewan and another small one in Texas. Mine capacity a little under 10 million tonnes. They produced 8.4 million tonnes last year.

I calculated that every $50 per tonne increase is another ~$400 million of revenue. Most of that, ex-taxes, should drop to the bottom line. That is close to a buck a share of EPS.

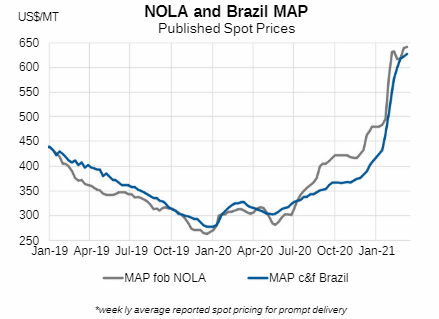

Mosaic’s other major business is phosphate. Midwest phosphate prices are $600 per ton FOB right now. This is up substantially year-over-year.

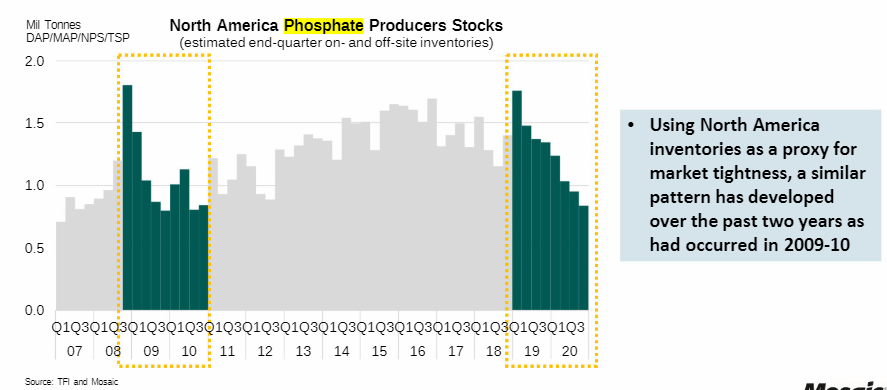

Inventories for phosphate look an awful lot like they did in 2009-10.

Mosaic’s phosphate operations are in the United States and Brazil. In the US they have capacity for just under 10 million tonnes of processed phosphate while in Brazil they have capacity for another 4 million tonnes (that is equal to 70% of Brazil’s annual production). They produced about 8,500kt of finishes product last year at a selling price of $360 per tonne.

Mosaic’s revenue from phosphate this year is, so far, significantly above last year. February revenue was $297 million vs $172 million in 2020. January revenue was $337 million versus $198 million. This does not include the Brazil operations, where sales were roughly flat yoy.

The Phosphate segment did about $2 billion in sales and $400 million in gross margin in 2020. This year I think they’ll do well over $3 billion of revenue. Probably over $3.5 billion. That extra $1.5 billion of revenue is going to almost all fall to operating income.

If you look at analyst estimates, they are pegged for ~$2.6 billion of EBITDA this year. That is after $1.5 billion of EBITDA last year. When you look at where potash and phosphate prices are, I think Mosaic is going to beat those estimates by a lot.

What’s more, the stock is anything but expensive. On analyst estimates the stock trades at a little over 6x this year’s EBITDA. In the 2009-2011 cycle, Mosaic’s EV/EBITDA got to over 11x. Once they show they are beating estimates, the multiple goes up.

Ag Growth International

AFN provides grain handling equipment to farmers and grain buyers. Augers, belt conveyors, bins, aeration equipment.

The bet here is that a reopening and rising grains prices has got to boost demand. It appears to be so far. On the fourth quarter call the company said backlog entered the year up 20% yoy and was up 40% yoy in March – and that March comp had not been impacted by COVID yet.

There are a couple of negatives that are going to hit their business this year. First, the bins are steel, which is going up in price (though that actually might pull forward demand in the short run).

Second, they sell into the US but costs are in Canadian, so this rising Canadian dollar (the bane of my existence) is going to be a headwind.

And third, they had a bin collapse last year, and that creates some uncertainty. I will get to that later.

But the stock is not super expensive. I bought it at $40. That is under 13x trailing (adjusted) EPS. The company had a dividend of $2.40 per share in 2019, which would be a 6% yield if reinstated.

While just a general improvement in business conditions is the main story, the kicker comes from their AGI SureTrack product. SureTrack is a connected farm type of product. It is directed at both farmers and grain buyers.

SureTrack is made up of a number of tools to monitor the farm. There is a grain bin monitor that tracks your grain level, quality and bin conditions. A field monitor keeps track of conditions in the field. There is tank manager for monitoring fuel and liquids. a dryer manager for monitoring grain drying. There is a marketplace for monitoring prices and connecting buyers and sellers. And there is an economics module that helps you maximize your margin based on growing, hauling, labor and fuel costs.

There is a very good discussion on the fourth quarter call where a lot of detail on SureTrack is provided.

They put together the platform through acquisitions of IntelliFarms, Affinity Compass, CMC as well as our investment in Farmobile.

AFN describes what SureTrack provides as follows:

They sell SureTrack through 3 principal channels: direct to farm, direct to commercial users, including grain buyers and food processors and through their dealer network.

AFN already has a large dealer network – they can sell SureTrack through 1,000 existing dealers in the United States.

There is a comp here with the recent IPO FarmersEdge.

SureTrack and FarmersEdge have one big similarity – they are both SaaS solutions for managing farm operations.

But Suretrack is not really in competition with FarmersEdge. There is a bit of overlap, but not much.

FarmersEdge is really a monitoring and predictive tool for managing the crop in the field. Seed selection; precision planting; precision application; machine automation; soil probes, satellite imaging and telematics data used to determine plant health and problem areas.

SureTrack provides a platform to manage the farm itself. FarmersEdge is upstream, SureTrack downstream.

FarmersEdge did about $46 million of revenue this year, up about 100% yoy. They lost $8 per share and had $44 million of negative free cash flow. SureTrack did $23 million, with less growth – 16% yoy or 33% on a retail equivalent sales basis (more on that shortly). While SureTrack is not yet cash flow positive, they said on the Q3 call they expected to reach that shortly.

The FarmersEdge solution is definitely the sexier of the two products but the fact remain that they both manage operations on the farm. With that in mind, FarmersEdge has a market cap of $740 million. AFN is going for about $1.5 billion, including debt.

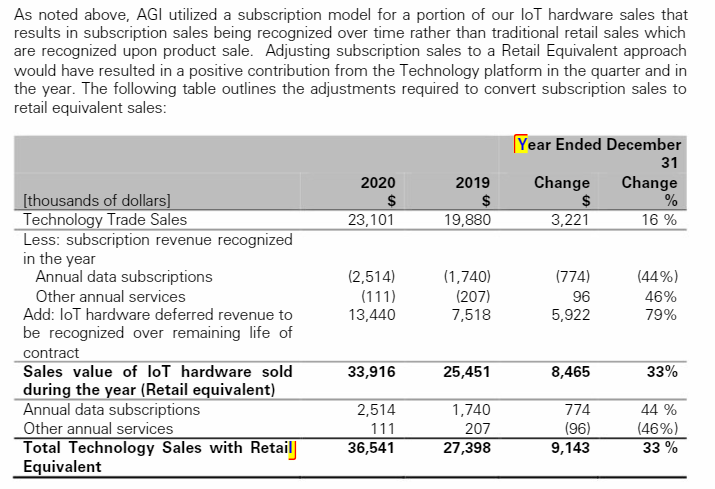

Now there is a question of how much SureTrack is really a SaaS business. AFN sells the IoT hardware and the subscription. The hardware currently makes up most of AFN’s revenue. The company breaks down the revenue buckets in their MD&A where they reconcile their “Retail Equivalent” revenue with the actual revenue that they are allowed to book.

There are positive and negative takeaways here. The negative is that the actual data subscription revenue is small. The positive is that the real apples-to-apples sales number should be the “Retail Equivalent”, which means the business is growing at a 33% clip.

It sounds like AFN is changing the way they sell SureTrack this year. They will be selling more of the IoT hardware upfront rather than packaging it with the subscription. This is actually going to make revenue look better than it should this year.

While the subscription revenue is, so far, small, that also means the market left to tackle is large. On the fourth quarter call they pegged the North American addressable SaaS market for SureTrack at $2 billion. The IoT side is another $10 billion.

CIBC is targeting 50% growth for SureTrack this year. That seems a little aggressive to me, but I do note that the data subscriptions grew at 44% last year, and that was with COVID. When one analyst asked about margins Tim Close, the CEO, seemed to agree with the assessment that 60-70% gross margins and 20% EBITDA margins would be in the ballpark. Close has talked about 50% growth in the past.

Whether this is a true SaaS business or not, I could see analysts getting onboard with comps to FarmersEdge and viewing AFN as a technology play. If SureTrack can pull off some eye-popping growth numbers this year, I think that could generate excitement and boost the stock quite a bit.

The rest of the business is not that exciting, but it is steady. They did $1 billion in revenue last year and generated $149 million in EBITDA. The year before that they did the same $1 billion in revenue and generated $144 million in EBITDA.

The company does have an albatross around its neck because of a pretty large mishap they announced in September. One of their bins collapsed at a commercial installation in Vancouver. This SA article goes over it quite well. There are two sites, with the same customer, that were affected. They have allocated $70 million as their cost of remediation of the two sites (they said they would be replacing the entire structures, including the hopper base). They said in the original press release that the original cost was $19.1 million so I’m not sure why its so high, unless maybe they are expecting legal costs too?

Anyway, what’s done is done and this does appear to be done. I mean its not great, it raises some questions about their ability to execute (assuming they are at fault, which has not been determined yet). But the biggest concern would be if this incident caused them to lose customers.

That doesn’t seem to be the case. As I mentioned at the start, the backlog is strong.

My last comment is there is quite a bit of debt here. There is $409 million of long-term debt and another $307 million of debentures. So the overall enterprise value is about $1.5 billion.

On an EV/EBITDA basis that puts the stock at 10x. On an adjusted EPS basis its cheaper – at 13x trailing earnings where I bought it.

On a free cash flow basis RBC puts 2020 at $2.44 per share – or 17x trailing FCF. RBC forecasts free cash flow at $3.16 per share this year and $4.67 per share in 2022. That seems pretty aggressive to me but if they hit it, the stock should be higher. I saw that CIBC is also forecasting $4+ of free cash flow in 2022.

So those are my two main farm plays. I havee a couple micro-cap bets as well that I will maybe talk about in detail another time. Imaflex and Flexible Solutions. Both provide solutions that reduce crop input costs.

Imaflex does it by producing crop protection films that cut down on pests and weeds in the soil around the plant. I’ve owned this stock for a long time and they finally seem to be putting together the results I’ve long hoped for. They did 12c EPS last year which means this is not an expensive stock.

Flexible Solutions markets a chemical call thermal polyaspartate that prevents fertilizer from crystallizing and therefore reduces the amount of fertilizer that needs to be applied. The company announced a disappointing number for Q1 revenue due to shipping constraints and the stock tanked on that. I decided to buy that dip to $3.

With respect to the rest of my portfolio, the mega-cap drug stock trade did not really work out as well on earnings as I had hoped. I screwed up on COVID. First Lilly, then Bristol Myers both took hits on earnings due to COVID. The problem (or not problem, depending on how you want to look at it) is that with vaccines here (none of which are supplied by BMY or LLY), the treatments these companies were supplying for COVID patients are no longer required.

I originally sold my BMY but decided to buy it back yesterday. I am keeping LLY because the pipeline is better and the Alzheimer drug could still surprise, which I believe would send the stock through the roof.

I forgot to mention retail in my last post. I was listening to a podcast of Mad Money a couple of weeks ago. Cramer had on Matt Boss, Retail Analyst from Morgan Stanley. Boss described retail as being in the second inning. I found it compelling.

So I looked at some of these retail stocks and yes, they have moved a lot, but they are not that expensive. Foot Locker trades at 15x this years earnings and 12x next years. Big Five Sports, I’ve talked about a lot in the past and it remains under 10x earnings if you believe they can do $2 EPS this year (they guided to 50c in the first quarter). The Gap

I bought Foot Locker and Big Five Sports early last week.

Finally, I bought Chemtrade International last Monday. I timed that one well (for once). The stock is up 8% since I added it. It has a great dividend, is cheap and its products should be levered to both recovery and to price pressure. Another one to talk about more another time.