Week 309: One Step Back

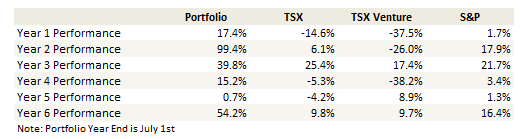

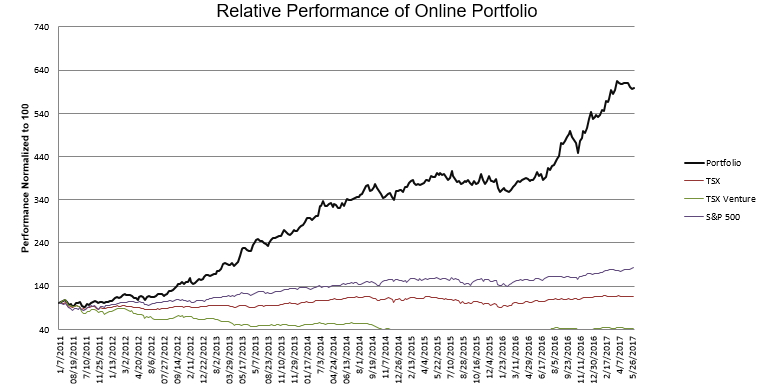

Portfolio Performance

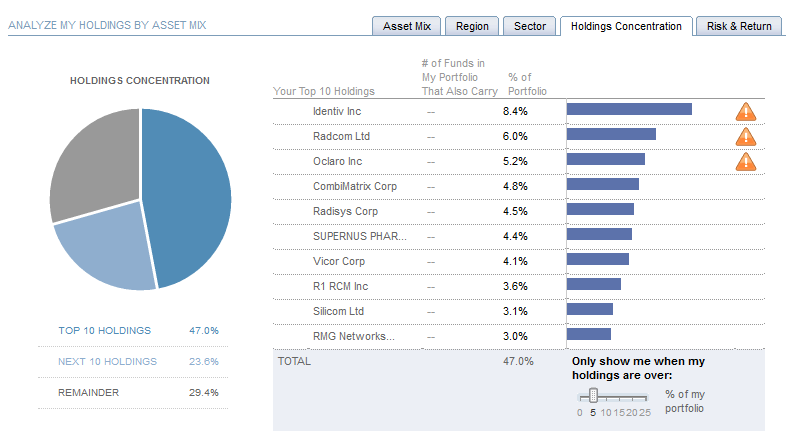

Top 10 Holdings

See the end of the post for my full portfolio breakdown and the last four weeks of trades

Thoughts and Review

April and May have been frustrating months. My portfolio has been down about 2.5%, which isn’t terrible, but as the market has kept moving to new highs it has felt quite a bit worse.

Looking at the performance of my individual positions, I would attribute my under-performance to the following themes:

- Investments in sectors that are doing poorly

- Companies that have exciting potential but its still not showing up on the income statement

- Upside exhaustion

On the first point, I’ve had positions in oil and gas and biotech, and these sectors have been somewhere between lackluster and dismal. Regarding oil, its been a tough time to own Journey Energy, Zargon Oil and Gas, and Vaalco Energy. Each has performed about as poorly as every other oil and gas name. I’m reluctant to cut these stocks loose though, I think each is cheap based on current prices and I’m not really in the camp that thinks we are heading back to $30 oil for any significant time. And as I’ve said before, if we do, the Canadian dollar is going to collapse, which will more than “hedge” any oil exposure that I have.

My biotech positions have been similarly crummy. Eiger Pharmaceuticals is the poster boy for this, having declined from $11 to under $7 in the last few months. I’ve held off adding to Eiger up until last week, when I put in some bids in the high $6 range that got filled. I am looking at a few other biotech names that I am looking to add on weakness.

Likewise, the performance of Novabay and Bovie Medical has been dismal. I sold Bovie Medical after their first quarter results and a conference call that I just didn’t find inspiring. Novabay, on the other hand, I feel more constructive about. The stock is down to an enterprise value of a little over $25 million (or was as of the weekend when I originally wrote this). The company is guiding to sales of $18 million for 2017, which is 50% growth over the $12 million in revenue for 2016. It seems like the stock is being crushed off of a notice of deficiency from the New York Stock Exchange. It’s a very low volume pull-back, which suggests it a couple of folks getting spooked out. It doesn’t seem like a big deal to me? I’m sure they will resolve it.

On the exciting potential but still not revenue bucket we have CUI Global, RMG Networks and Radisys. Radisys hasn’t done terribly, its about the same level it was in April (which is not really a positive thing to say), but RMG Networks and CUI Global have both been crushed. RMG Networks needs to get some of these trials and engagements contributing to revenue and until they do I’m not going to be buying the stock. I’m still wary of this name; it could pan out in a big way but it seems like there is a lot of hand waving about what’s to come that has been going on for a number of quarters now. I’m waiting, but not as patiently as I once was.

I added a position too soon with CUI Global. I bought the stock after some very weak results in the low-$4’s but that hasn’t proved to be even close to the bottom. Fortunately I only bought a little, and have subsequently added at $3.70 and again at $3.40.

I have some conviction that CUI Global has the technology to generate significant revenues over time and that its just a matter of time before we see those materialize. In particular, one day they are going to see the regulatory issue that their customer Snam Rete is having that is preventing installations get resolved, and when it does the stock is going to pop big-time. I noticed there were some small insider buys at the $3.40 level so I’m not the only one who thinks this is a decent value here.

As for the third theme, I had great runs from Combimatrix and Identiv and they simply ran out of legs. I continue to hold both, believing their momentum will resume after this breather.

I took new positions in Sito Mobile and Psychemedics this month and have already written about both. There are a couple of others that I will try to write about shortly. I also reduced my position in Medicure, which I talked about here, and exited my positions in BSquare and Versapay.

Neither Versapay or BSquare have shown me that they can convert their leads into sales. Versapay announced another quarter of decent growth on a year over year basis but still very low revenue on an absolute basis. They are not cheap on a multiple of revenue. BSquare isn’t gaining traction fast enough for my liking with its DataV product. The company recorded no new bookings in the first quarter and their DataV backlog declined from $5.7 million to $3.2 million. I’m actually a little surprised both stocks have held up as well as they have after what in my opinion were somewhat lethargic quarters.

Portfolio Composition

Click here for the last four weeks of trades.

{kind=link}