Week 236 Mistakes were Made (by me)

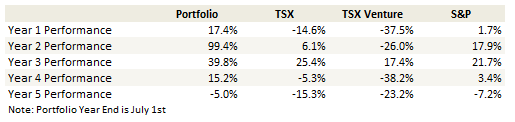

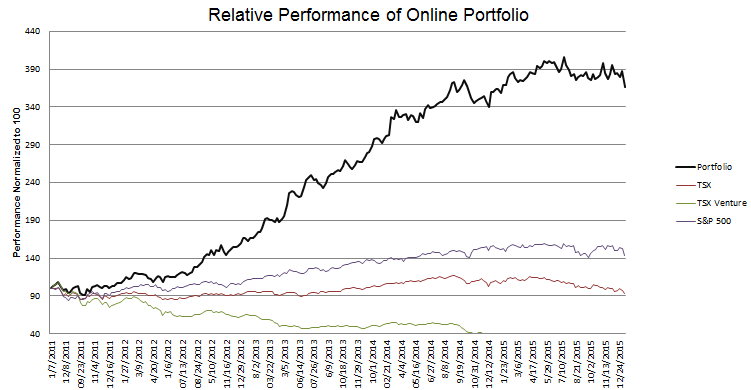

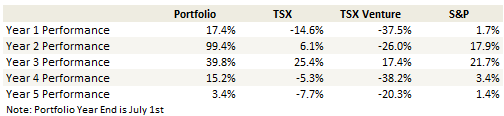

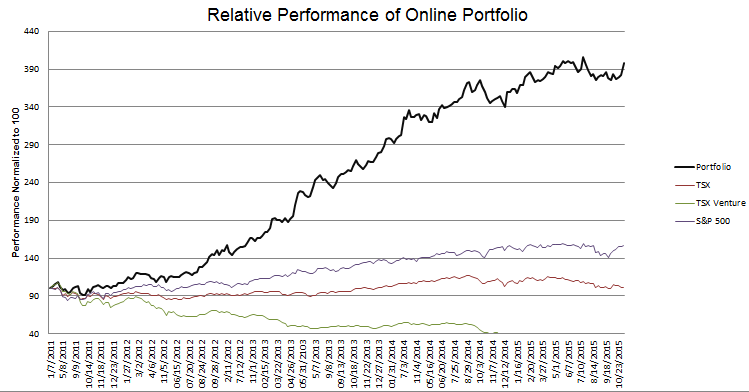

Portfolio Performance

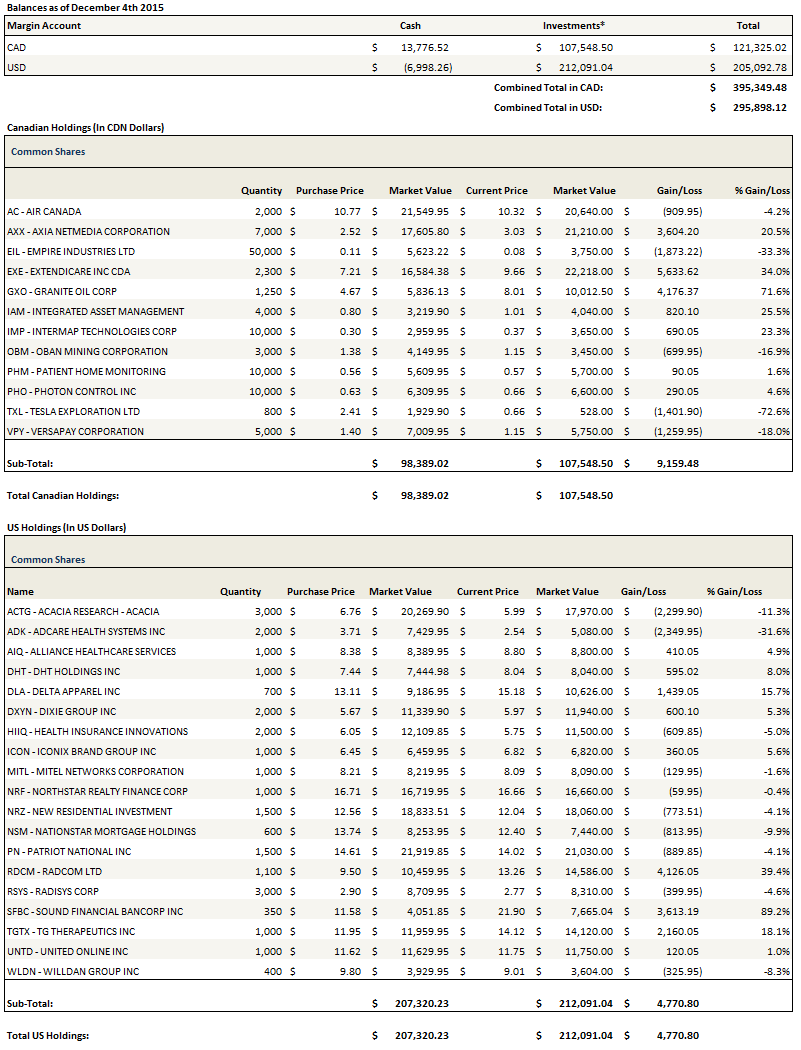

See the end of the post for the current make up of my portfolio and the last four weeks of trades

I am late getting this update out. Last week I found it hard to write about my investments as my portfolio is getting ravaged every day.

I was doing pretty well up until the end of the year. I wasn’t at a high, but I wasn’t too far away and the market was only doing ok so that didn’t seem too bad. I’d taken some one-stock hits in December, on news from Patriot National, Acacia Research and Iconix, but I had managed to make back those losses by working hard to find other names that worked.

Then the new year hit and it all fell apart.

I wrote about 80% of a write-up last weekend. I intended to write the rest Monday, but my portfolio got smacked. Same thing Tuesday. By Wednesday I was selling some positions and adding to others, so my original write-up seemed out of date. On Thursday I had a miserable day as the positions I had added to (Northstar Realty, Brookfield Residential, TG Therapeutics, Relypsa) took further hits. On Friday, after some further losses, I threw in the towel, sold a lot of stock, and went back to a big cash position and (where I can) shorts to hedge the rest.

It is a little depressing. I am literally back to the exact same level I was at during the mid-August bottom which is the same level I was at during the early October bottom (note that I’m pretty sure that intra-day of the crash that occurred in August I was quite a bit lower, though stocks recovered a lot of those losses by the end of the day so we’ll never know how bad it got). No progress.

You work hard, find some good stocks, manage through some bad one’s, scalp a few trades where you can and make some progress and then in a week you are right back where you started.

Not fun.

I made the following tweets on Friday evening that sum up my sentiment:

sigh…back to same portfolio level as Aug/Oct btm – gave up interim gains again, down 5% from high, sold/stopped out, back to cash, hedged

— LSigurd (@LSigurd) January 9, 2016

I thought I was more cautious this time – 30% cash at top, but wasn’t enuff, too many volatile small caps got smacked hard, added too soon

— LSigurd (@LSigurd) January 9, 2016

I thought I was more cautious this time – 30% cash at top, but wasn’t enuff, too many volatile small caps got smacked hard, added too soon

— LSigurd (@LSigurd) January 9, 2016

I cant help my response to corrections. My defining moment as beginner investor was 08. I know this isnt 08. But I don’t know what this is

— LSigurd (@LSigurd) January 9, 2016

Didnt know what Aug/Oct/ebola panic/debt ceilings were either. No question would’ve been better not to panic/sell/hedge – just stay course

— LSigurd (@LSigurd) January 9, 2016

Problem is I didn’t know what 08 was until too late. It was so painful, so awful. I feel like I have to insure that never happens again

— LSigurd (@LSigurd) January 9, 2016

It makes it hard to buy the ‘dips’, hold stocks thru corrections. Cuz I experienced a time where it just kept getting worse and it haunts me

— LSigurd (@LSigurd) January 9, 2016

Frustrating. No progress for 7 mths. One step fwd, one back. And sick that we may rebound again like Aug/Oct and Im scrambling for pos’ns

— LSigurd (@LSigurd) January 9, 2016

So I don’t know, maybe this is going to turn out to be a whole lot of nothing again, but you never know. What kind of worries me about last week is how many stocks I own and follow made 52-week lows on basically no news. Stocks that fell like a knife through support on absolutely no reason. The overall move in stocks was supposedly caused by China but that disagrees with what I saw because what I watched were positions in Northstar, Brookfield, Delta Apparel, Vicor, TG Therapeutics, Relypsa, get obliterated and none of them have anything to do with China (to make no mention of others like Patriot and Iconix, where yes they have their own issues but still the collapsed on no news was somewhat stunning). In fact much of my losses were the result of buying stocks that I felt were isolated from China but which fell extremely hard anyways.

The last time this sort of move happened was when Bellatrix, RMP Energy and Swift Energy went into free fall in October 2014. It all seemed terribly overdone at the time but was fully justified in retrospect given what happened to the oil markets. Looking back on that time, the only thing I wish is that I would have sold out sooner.

I sold sooner this time. Never soon enough, but sooner.

One of my favorite books over the last few years has been Mistakes were Made (but not by me) by Carol Tavris and Elliot Aronson. In the book the authors investigate how the brain is wired for self-justification. When we make mistakes we experience cognitive dissonance that is uncomfortable, maybe even unbearable. If we allow ourselves to rely on our natural fallback mechanisms our response is to disengage ourselves from responsibility, make up a story in our head to justify what we did or change the narrative entirely to a more pleasing one. The intent of which is to restore our belief that we are right. The consequence is that we do not learn, we do not change, and we are more likely to make the same mistake again.

I am not going to allow myself to justify why I am right and the market is wrong. Not when I get bombarded with evidence like I got last week. I don’t know the reason. Maybe (like with oil in October 2014) there is something out there that I just haven’t figured out yet. Maybe I’m just picking the wrong stocks in the wrong market. Maybe everything bounces back next week and I am left scrambling (and I will scramble back into some of these positions if it looks like the coast is clear). Nevertheless if I was doing things right, this week should not have happened. I should not be losing 5% in a week. Something is wrong and the only prudent thing I can do is take a step back until I figure out what that is.

What is written below is what I wrote before the carnage of last week. Not all of it is relevant. I sold out Iconix. I sold out of Relypsa. I cut Patriot back substantially. I still hold my golds, and added to a few in the last week. Note that I also started one new position that I kept, Vicor, but I am in no mood to write it up right now.

Gold stocks: Lake Shore Gold

These gold stocks get no respect. If I told you that I had a company with a $500 million market cap, zero net debt, generating 50% gross margins and with free cash flow of $42 million in the first nine months what would you say? Sounds pretty good doesn’t it? Except its Lake Shore Gold.

I am returning to the gold sector because I see it as a potentially misunderstood investment. The gold stocks all move inline with the price of gold. Its painful to watch. The price of gold goes up $5 and they all get a bid. It drops $5 and that bid disappears.

Yet for non-US based gold producers it is not the price of gold in US dollars that determines their margins. Its the price of gold in local currency, or to look at it the other way the cost of production in US dollars. For Canadian, Mexican and many South American producers, the cost of producing gold has fallen dramatically. Add to that the reduction in energy costs and many producers are experiencing margins that are actually better than they were when gold was a few hundred dollars higher.

Lake Shore Gold has 439 million shares outstanding. It has long-term debt of $91 million, cash on hand of $80 million and another $20 million in gold inventory. In the first nine months of the year the company generated $77 million in cash flow before working capital changes, spent $37 million in capital expenditures and another $7.5 million in finance equipment leases. Free cash flow was $42 million.

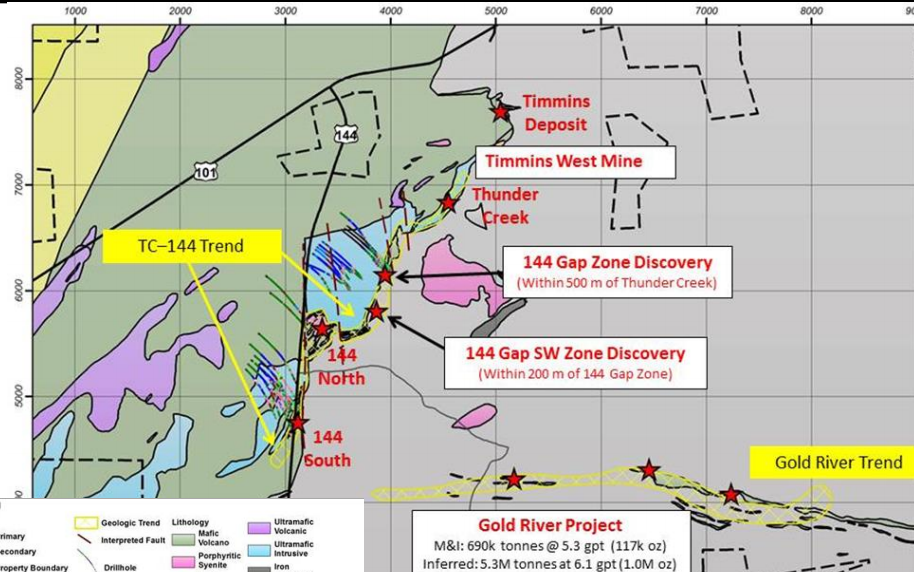

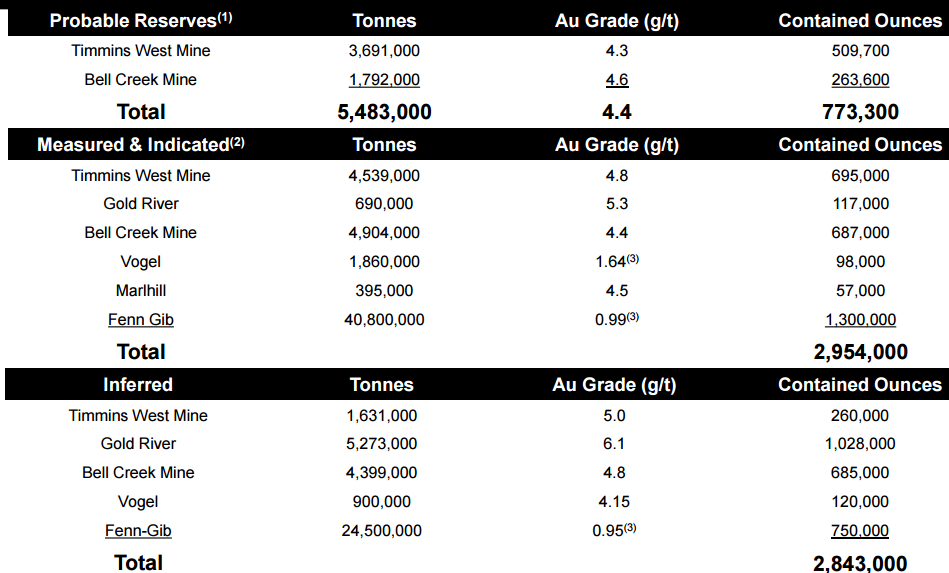

Lake Shore operates two gold mines in Ontario. The Timmins West Mine is 18km west of Timmins. Lake Shore produces from two deposits: Timmins and Thunder Creek. The trend is ripe for new discoveries and there have been a couple with the 144 Gap Zone and 144 West Gap Zone. Below is a schematic of the four deposits.

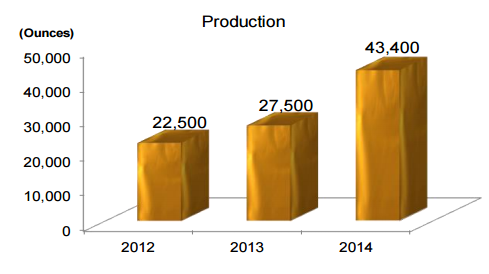

Production from Timmins West has increased over the last three years:

The 144 Gap resource is expected in the first quarter. By the looks of their underground schematic the 144 Gap can be accessed via existing Thunder Creek infrastructure – Lake Shore said in Q3 MD&A that exploration drift from Thunder Creek to 144 Gap was completed in the third quarter, which should simplify the road to production.

I ran a quick and dirty resource estimate on 144 Gap and think it could post an impressive number. In their MD&A Lake Shore says that the 144 Gap is 300m x (50-125)m x (75-125)m. I grabbed a specific gravity estimate of 2.92 from the technical report created for Thunder Creek and West Timmins. The volume of deposit is between 1.125mmm3 and 4.6875mmm3. I eyeballed the grade of the deposit from slides 13-15 from this presentation. The results are as follows:

– 2.92 x 1,125,000 = 3,285,000t

– 2.92 x 4,687,500 = 13,687,500t

– 3,285,000 x 4.5 / 31.1 = 475,000oz

– 13,687,500 x 4.5 / 31.1 = 1.98moz

Lake Shore’s second mine is Bell Creek, which is 20km east of Timmins. The mine also has the milling facility in addition to the Bell Creek Mine where ore from both Timmins West and Bell Creek are processed. Bell Creek produced 43,400oz in 2014.

Lake Shore recently bought Temex Gold (September 18th) and their interest in the Whitney project for $23 million. They acquired 708,000 M&I oz and 171,000 inferred oz at Whitney. The M&I resource is quite high grade at 6.85 g/t. Whitney is strategically located; its right next door to the Bell Creek Complex. Whitney was 60% owned by Temex and 40% owned by Goldcorp.

Below are the company’s reserve and resource. Because so much of the company’s operation is underground, the resource is less robust than many of their open pit competitors. I wouldn’t read too much into this. Underground operations are by their nature going to have smaller resources because its simply not economic to drill extensively at depth until mining has commenced nearby. As we see with the recent 144 Gap zone discoveries there is plenty of potential for additional ounces to be added.

The only unfortunate thing is that Lake Shore remains a bet on the price of gold. And I’m not really sure how constructive I want to be on the gold price just yet. I’m feeling better about gold; I look back to the years between 2004-2007 where the Federal Reserve was raising rates and gold was rising. I’m hopeful that the beginning of the rate hie cycle will mark the bottom in the gold price. But I’m not convinced. If I was I would be plowing money into a profitable and well managed miner like Lake Shore and building a big position. As it is, I’m keeping my position modest, and we’ll wait and see what the next move is.

I also added positions in Claude Resources and Argonaut Gold. I already have a position in Oban Mining and Carlisle Goldfields.

Taking Hits and Bouncing Back Part I – Patriot National

I had an abnormal number of negative events hit my portfolio in the last month. Had it not been for these events, my portfolio would have broken out to new highs. As it was I instead spent the month paddling upstream against the current.

But this is the nature of my investing strategy, which to some degree is bottom feeding in stocks of questionable merit but with the potential for outsized returns if events fall into place. Unfortunately in each of these cases events fell outside of expectations.

When I invested in Patriot National it was with the understanding that the company had some questionable behavior in its past. A perusal of the related party acquisitions over the last 18 months leads to some questions and while I am not going to get into the details here, I would direct those interested to read through the proxy for Global HR Research for an example.

Nevertheless I felt comfortable enough investing in the stock because the business was (and is) growing and the CEO Steven Mariano, owned over 60% of the outstanding shares. This seemed like a good put to me, that nothing too shareholder negative would be done as his own net worth would suffer.

Unfortunately that turned out to be naive.

My mistake here was that I read the news release, thought that the attached warrant was unfortunate, but did not dig any further. That is until about two hours into trading that morning with the stock down $4 when I realized something must be wrong. In the proxy document for the offering was a description of the nature of one of the two warrants being offered along with shares, in particular the exercise price associated with the warrant:

“Variable Exercise Price” means, as of any Exercise Date, 85% of the Market Price on such Exercise Date (subject to adjustment for stock splits, stock dividends, stock combinations, recapitalizations or similar events occurring on such Exercise Date).

When I read this I honestly couldn’t believe it. I thought I must be missing something. Who offers shares that it is questionable the company even needs and tacks on a warrant that lets you buy more shares at essentially any price. What stops the warrant holders from shorting the shit out of the stock, driving down the price and then redeeming their warrants at the depressed level? And even if that is explicitly prohibited by the proxy (which it was) what stops investors like me from worrying that they will figure out a way to do it anyways, and selling their position before it happens?

It was essentially a “no bottom” situation where the more the stock fell the more worried you’d get that there were nefarious forces at work and that it would fall further. So I sold. About 30% lower than the stock closed at the previous evening. But over 30% higher than its eventual bottom.

Amazingly, a week later, on Christmas Eve no less, Patriot announced that they had come to an agreement with the subscribers and cancelled the company offering. Mariano, who was offering some of his own shares as part of the deal, would still sell his.

This brings us to the current state, which is interesting. As far as the company, its basically status quo. Guidance has been reaffirmed, no dilution has occurred, its the same company it was a month ago. Ironically my original thesis, which was that Mariano owned too much stock to do anything too stupid, played itself out as one would expect. I doubt that the decision go back on the offering was out of concern for the shareholder base so much as the shock that some $80 million of his net worth had evaporated in a few days.

The problem is that credibility has been lost and as a result the stock is trading at about half the level it was at prior to the debacle. While I totally understand the perspective that you just have to walk away from any management team that would attempt something like this, I am compelled by just how cheap the stock is. So I added my position back. We will see if time and maybe a few good moves can heal some wounds.

Taking Hits Part II and II – Acacia Research and Iconix

Acacia Research was the second negative event to befall me. This one was relatively simpler than Patriot. The company lost a patent infringement suit that I didn’t think they were going to lose. It was for their Adaptix portfolio, which is one of their marquee portfolios, and so it calls into question the valuation of that portfolio. With the stock down at $4 its trading extremely close to cash and you can certainly make the argument that the current price exaggerates the impact of the legal loss.

I sold because I saw the stock falling, knew that the lawsuit was pending and that therefore it had likely went against Acacia, and suspected that there would be more selling than buying over the following weeks so it was better to get out sooner than later. I plan to revisit after my 30 day tax loss selling period has expired.

When I entered into a position with Iconix it was with the knowledge that there may be more shoes to drop. So when the SEC announced a formal investigation into the accounting treatment of the company’s joint ventures, I was disappointed but not surprised. As in the case of Patriot and Acacia I thought it better to sell first and ask questions later, which turned out to be the prudent move as the stock fell further (20+%) than I would have expected.

Iconix feels binary to me at under $6. Even after the move last Thursday which jumped it to $7 the stock still seems to reflect quite a bit of pessimism about the investigation.

The company isn’t perfect, to be sure. To reiterate some of what I wrote last post, debt lies at $1.5 billion which is simply too high. A few of their menswear brands are experiencing headwinds which may or may not be permanent. The new management conceded that not enough dollars have been spent on advertising and that a “refresh” of a number of their brands is necessary.

Nevertheless, the company owns strong brands prominent in a variety of retail (Walmart, Target, Kohls, Sears/Target) as well as entertainment brands like Peanuts and Strawberry Shortcake that have long term appeal. They should be able to continue to deliver consistent licensing revenue. At $6 the stock reflects 4x free cash flow even using somewhat depressed 2016 numbers. That’s a cheap number for any business that doesn’t have questions about being a going concern.

On further reflection though I decided that the market was probably punishing the stock on uncertainty and passed transgressions than it was on any new revelation. I think what happened is that the company is suspect because of the already announced accounting issues, and the press release announced was admittedly vague and light on details, so it was an excellent opportunity to imagine the worst.

Relypsa

I got the idea for Relypsa from @exMBB on twitter. Relypsa has 41.7 million shares outstanding so at the current price it has about a $1.1 billion market capitalization. the company has $285 million of cash.

Relypsa specializes in polymeric drugs. In particular they are targeting a condition called hyperkalemia with a drug called Veltassa. Here is what hyperkalemia is:

Hyperkalaemia (higher-than-normal potassium levels) follows the kidney’s inability to excrete potassium, mechanism impairment of potassium transport into cells or a combination of both, according to ZS’ website. It can cause cardiac arrhythmia and sudden cardiac death.

Veltassa is a polymer that will exchange calcium for potassium. The existing treatments work on exchanging sodium for potassium, which is not well tolerated in patients.

Our bodies relatively narrow range for which we can tolerate potassium in our kidney. Most of us take in more potassium than we can handle but we just excrete the extra. However if you have chronic kidney disease you can’t and you end up with dangerously high potassium levels.

If you have a potassium level of 5.5-6 or greater, there is need to treat the patients, but treatment is intermittent because of the poor tolerance of the available options. With Veltassa you can take patients that are hyperkalemia, pull down their potassium to the normal range and keep it there.

The patient population is 2.5-3 million patients, with these patients all being parts of the CKD3 and CKD4 (CKD is Chronic Kidney Disease) populations that have high potassium levels. On one of the conference calls Relypsa said that Veltassa would be sold for $600 per month.

Veltassa has been approved for treatment of hyperkalemia, broad application. The approval occured on October 21st. The problem with the approval was that it included a limitation of use that it is not be used in emergency situations. The stock dumped initially but recovered much of the losses through November and December.

The warning label was required because there was some indication of interaction of Veltassa with other drugs – in particular in vitro studies showed interaction with 9/18 drugs tested against.

Listening to some of the recent conference presentations, Relypsa argues that the in vitro test is conservative. In vitro studies are very good at showing where there is no interaction but give false positives for interactions that need to be verified.

Relypsa is going to perform human drug interaction studies to find out if the in vitro studies are correct. The human studies they are done with healthy volunteers, there may need to be additional studies with some other patient groups such as type 2 diabetes patients who have stomachs that empty much slower and where a 3hr separation wouldn’t be enough. But the first results are expected in early 2016.

The concern is that the warning label, if it stays, will put Veltassa at a disadvantage against competition, in particular ZS-9, which was developed by a company named ZS Pharma. ZS-9 is further behind than Veltassa, an FDA approval decision isn’t expected until the spring and it carries some concerns of its own.

Glassock maintained ZS005’s high hypertension threshold will impact approval or prompt a black-box warning. Lipicky agreed a black box could be issued. Veltassa’s boxed warning states it binds other orally administered medications, potentially decreasing their absorption and reducing effectiveness.

ZS Pharma was recently taken over by AstraZeneca. They paid $2.7 billion for the company. ZS Pharma is essentially a one drug company. The implication is that apart from the warning label concerns about Veltassa, Relypsa should reasonably expect a takeover value in the same range.

Some of the takeover talk has ramped up through December, first with rumors about Merck and then with rumors of a bidding process in the works. Here is what is said about the takeover possibility on IBD:

Shortly before noon, Street Insider quoted an anonymous source saying that Merck (NYSE:MRK) was about to make an offer for Relypsa for an unknown price. About an hour and a half later, the Financial Times reported that its own anonymous source said that Relypsa was merely starting the process without a particular buyer, though GlaxoSmithKline (NYSE:GSK) and Sanofi (NYSE:SNY) are both potential bidders.

Speculation that Relypsa could be bought has been buzzing since AstraZeneca (NYSE:AZN) agreed to buy ZS Pharma (NASDAQ:ZSPH) last month for 2.7 billion. Relypsa and ZS Pharma both make drugs treating high levels of potassium in the blood; ZS Pharma’s hasn’t been approved, while Relypsa’s drug Veltassa was approved in October but with a stiff warning label about dangerous interactions with other drugs.

Its an interesting situation, one that is speculative to be sure. There is a short interest that doesn’t buy the story, and plenty of action in both puts and calls. There is also the question as to why AstraZeneca bought ZS Pharma and not Relypsa in the first place. Still, I think its worth a speculation.

Portfolio Composition

Click here for the last four weeks of trades.

{kind=link}