Week 227: No pain no gain

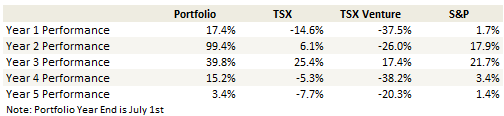

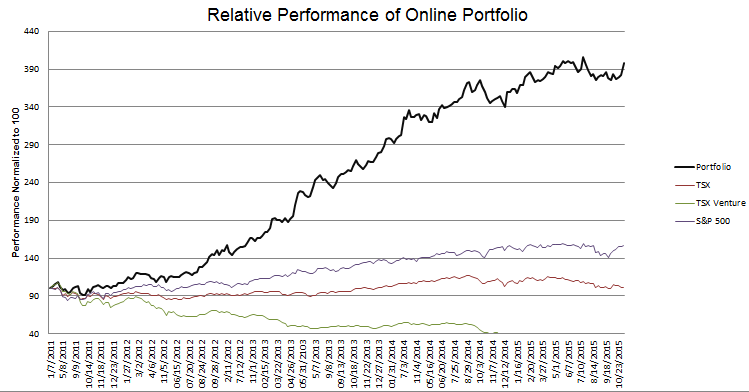

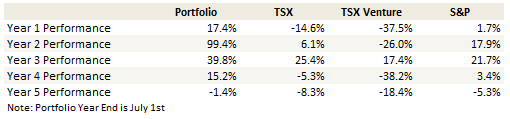

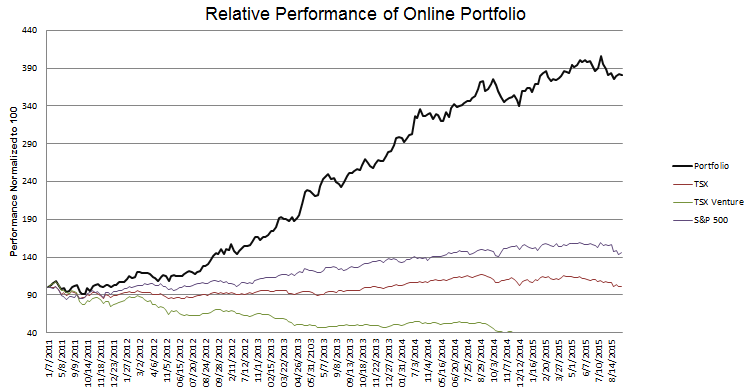

Portfolio Performance

See the end of the post for the current make up of my portfolio and the last four weeks of trades

Monthly Review and Thoughts

Over the last few months I have been focused on minimizing the fluctuations in my portfolio. This has kind of worked. I haven’t had the up’s and down’s that I might have had otherwise, given the volatility. But I also haven’t had the returns.

The reality is that I very rarely do well without experiencing a lot of pain beforehand. Let’s look at a few examples to prove that point (I’m going off of memory here so allow me a little leeway in the exact figures):

- Tembec and Mercer both fell ~30% from my original purchase price before rallying to be triples.

- PHH went from $15 to almost $10 before eventually running into the mid-$20s

- I originally bought MGIC at $2.50, watched it fall to almost 50c, before finally selling the stock over $8.

- YRC Worldwide fell from $8 to $6 before making its run to $30.

- I watched Extendicare go from $7.50 to $6, adding extensively on the way down. Now its at $9

- Every time I buy New Residential it seems to fall incessantly for days or weeks after my first purchase before I finally wind up making a good return on the stock.

Unfortunately, the fall is part of the reason for the gain. These situations turn out to be big winners is because

A. I get to know the story really well (as the name falls, I worry and fret about whether I have screwed up (because I screw up a lot) and in the process I learn a lot more about the position

B. I add to my position.

I know I say I have a rule that I don’t add to losing positions and I cut positions after a 20% loss. And that is mostly true. But its not totally true. What I actually do is dramatically escalate my level of worry at that threshold, which in most cases leads to nausea and good riddance. But sometimes I find the story compelling and I get stubborn, and in these cases I add.

The mental capital that I expend in these situations is enormous. I grump and fight depression as the position falls. I feel elated when it finally rises only to be sent back into gloom as it falls again. Its a gut-wrenching experience and one that I have come to dread. But it is, unfortunately, an absolutely necessary part of the process. I know of no other way to capture returns.

I haven’t been doing this lately. I have been too scared to take risk. The consequence is that I have sold a number of stocks way too soon. I sold Hawaaiian Holdings at $26. I sold Bsquare at $6. I sold Apigee at $8 (I realize its back at $8 but that was before going to $10+). I sold Impact Mortgage at $17. And so on. In no case have I been willing to scale up.

This month I decided to change my tack.

First, I took a brief but very large position in Concordia Healthcare in the midst of its free fall. It may not have been prudent and it was probably born out of frustration as much as anything, but as Concordia dropped to $25 Canadian on October 21st I just kept adding. At the low, I had a 15% position in Concordia and by 11am, as it hit $25 (I believe that was around $19 US) I had fully reconciled myself with the possible carnage I was risking.

I actually sold half of the position at what turned out to be essentially the low. But seconds later I felt the fear of copping out at a bottom to be more overwhelming than riding the position all the down. Or maybe I had a rational moment where I considered that the CEO had just been on BNN basically dispelling any connection to the troubles with Valeant and thinking to myself that maybe its just taking a few minutes for the market to catch on to what he just said. So I bought the whole thing back and more. I remember my hands were shaking and I was walking around in a daze. I put a fork in the microwave at lunch.

Fortunately what appeared to me to be unwarranted actually turned out to be. The stock moved up slowly then quickly, ending the day at $34 and two days later at $44.

I’d love to say I held the whole stash for the run but I didn’t. Happy with the relief of turning big losses into reasonable gains, I sold stock at $30, at $34 and again at $38 the next day. I let go of the rest a few days later at $42.

The event, which quite honestly was harrowing, was another reminder. I have to be willing to be scared if I am going to make money. This may have been an extreme example, and looking back on it I don’t think it was probably the sensible thing to do, but nevertheless taking a risk on a situation that doesn’t make sense to me is the essence of what I need to be able to do.

Since that time, having woken up again to the necessity of risk, I made a couple of other bets that are more “risky” than what I would have attempted a couple months ago. I took two reasonably large positions over the last two weeks; one in Air Canada and one in New Residential. I took a third on Friday with DHT Holdings.

I actually wrote this part of the write-up earlier last week, on Wednesday, but I had to delete it and write it again over the weekend. When I wrote on Wednesday, my position in New Residential looked to be under never-ending selling pressure and my position in Air Canada felt like it would never move up. So I wrote a couple paragraphs about how I was going to stick with these positions because I really thought I was right here and even as I was tearing my hair out and becoming angry at the world I still believed I would prevail in the end.

Fortunately things started to turn around.

What can I say. I got kicked in the teeth for most of October. I was literally down 9 straight days at one point. Not down big mind you, but nevertheless I was down every freaking day. Keep in mind that this happened as the market roared to new heights. It felt like a never-ending assault.

Things started to turn last Thursday (the 26th) when Radcom put out a pretty so-so quarter but hinted at some excellent Tier 1 opportunities on the conference call last Thursday. This was followed up by a solid quarter from Radisys.

Last week was up and down until Thursday when Air Canada reported a quarterly beat and the stock actually held its gains, Mitel reported a solid quarter and was up a buck, Granite Oil showed that someone can make money at $45 oil, raising its dividend and moving up a dollar and New Residential, while pulling in a modest 10c rise, pulled off an intraday reversal and a glimmer of hope. Friday was even better with big gains from all of the above mentioned names.

I’m hoping its the start of something. I’ve had enough pain.

New Residential

I’ve taken a fairly large position in New Residential. At $12, which is where I was really adding, I think it is just too cheap, with a 15% dividend, positive exposure to higher rates, and below the book value of $12.40 which doesn’t even account for the $5-$10 of value that their call right portfolio could eventually yield (more on that below).

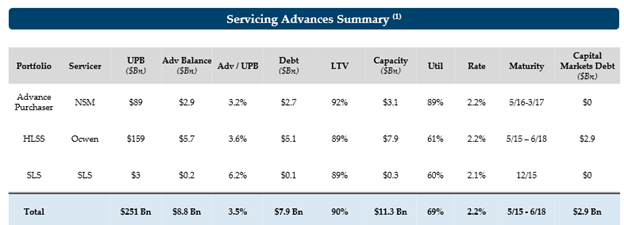

I’ve talked about their mortgage servicing portfolio on numerous occasions so I am going to leave that for now. I’ll focus instead on the two other portfolio segments, servicer advances and call rights.

Servicer Advances

Here’s how it works. New Residential buys a pool of outstanding servicer advances and with it the base fee component of the related mortgage servicing right (MSR). The price of the purchase is a discounted cash flow value of the outstanding and future advances and the base fee.

Typically New Residential already owns the excess MSR in these pools. The base fee they purchase would likely be around 20 basis points depending on the type of mortgage they are servicing. Nationstar or Ocwen would remain the servicer and perform all the servicing duties in return for a servicing fee that New Residential pays them. The fee structure of the servicing fee is described in the 10-Q and appears to be quite different for Nationstar than for Ocwen, but the essence of both is that there is a base fee paid and an incentive or profit sharing fee that is made once a return threshold has been reached.

New Residential makes money via the spread between A. the base fee they receive on the MSR and B. the combination of the fees that they have to pay the servicer (Nationstar or Ocwen) and the interest expense that they have to pay on the advances. They explained it like this on the first quarter conference call:

The way that we get compensated, we receive a portion of the MSR off of the $251 billion UPB of non-agency loans. This compensates us for our advances. Our advances are currently funded with $7.9 billion of debt with an approximate advance rate of 90% and an interest rate of — cost of funds of 2.2%. On our debt, 50% have fixed-rate coupons, which will also help mitigate interest rate risks. And as I pointed out earlier, our life-to-date IRR on our advance portfolio has been 34%.

They also explain the whole process fairly well on slide 10 of their first quarter presentation:

The way to think about the investment is that its just another way to get at the monthly servicing income. Instead of paying for the excess servicing right with only up-front capital, you pay for it with a combination of up-front capital and the on-going servicing fee and the interest on the advances. But the essence is the same; its a perpetual income stream as long as the mortgage is not paid back or delinquent. So it is pretty similar to the excess MSRs that New Residential is better known for. I’m not sure whether the investment community sees it that way though, which may present an opportunity once the steady cash flows become appreciated.

Non-agency Call Rights

A call right is the ability to “call” securities once certain criteria have been met. My understanding, which admittedly isn’t perfect, is that the criteria to call for the non-agency securities in New Residential’s portfolio, triggers when the UPB of the underlying loans pays down to 10% of the original balance.

New Residential has been acquiring call rights as part of the private label servicing that they have acquired. It seems like the call rights have been something of a free-bee thrown in with the mortgage servicing right in many cases.

This means that New Residential’s call right portfolio is not recorded as a significant asset on the balance sheet. Management drove this point home on the first quarter conference call:

Douglas Harter – Crédit Suisse AG, Research DivisionSo just to be clear: there’s no value on the balance sheet today for those call rights?

Michael Nierenberg – Chief Executive Officer, President and DirectorThat’s….

Jonathan R. Brown – Interim Chief Financial Officer, Chief Accounting Officer and TreasurerThere’s essentially no value on the balance sheet. When we acquired them, we put a small number on, but it doesn’t move with the mark-to-market.

So book value calculations for New Residential ignore the value of the call rights.

Now for a little bit about how it works.

First, New Residential is going to look at the bonds underlying the call right and, where possible, purchase these bonds at a discount to par. The call right gives New Residential the ability to call the bond at par plus expenses. When the market is in their favor they do this, and then take the performing loans and repackage these into new securities which they sell at a premium to the par that they called the bonds. The delinquent loans stay on the balance sheet and New Residential takes interest from these loans and liquidates them as opportunity permits.

we buy bonds at a discount that accrete to par when we call them. We call the collateral at par plus expenses, we then securitize or sell the loans at a premium. The delinquent loans that we take back are retained on our balance sheet at fair market value and that those get liquidated or modified over time. Since we’ve begun this strategy, we’ve been averaging approximately two to three points of P&L per deal.

New Residential has about $200 billion of UPB in call rights (they said $240 billion UPB in the first quarter but have since then referred to it only as over $200 billion). Impressively, this amounts to 35% of the outstanding legacy non-agency market. Right now about $30 billion that meets the 10% UPB criteria to be called. Therefore it can be called be if New Residential finds that it is accretive to do so, meaning specifically if the market conditions for the new securitizations are favorable.

That $200 billion will amortize over time, so the actual UPB at the time it is called will be somewhat less. They think the eventual UPB will be in the $100-$125 billion, as they described on the first quarter call:

There is going to be amortization to get to a 10% clean-up call or 10% factor on the underlying deals. So in our best case or our best guess-timate at this point, that $235 billion at the time of call will be between $100 billion and $125 billion.

The economics of the deals were discussed on the first quarter call as such:

Our recent experience when we’ve called deals, the way to think about this, has been we’ve been making approximately 2 to 3 points per deal. Now some of this will be dependent upon rates, but as you think about it, on a $100 billion portfolio of call rights at the time of call, 2 points would be — would correlate to about $2 billion. Thinking about it, with 200 million — 198 million shares outstanding, it should bring in approximately $2 per share.

So I am quite certain Michael Nierenberg, the CEO, misspoke on the $2 per share comment. This has caused me a bit of consternation because he actually said the $2 comment twice. But I’ve read a few brokerage reports and the value they are more inline with what the other numbers imply. Undiscounted the earnings potential here is more like $10 per share. Piper Jaffrey gave a $5 per share value to the call right portfolio here. UBS gives a value of $6 per share to the portfolio.

So that is a crazy big number for a company trading at $13. Its why, even if we get a little run here to $14, I will be reluctant to part with my position. I need to keep reading and making sure that I am not missing anything, but this feels to me like another one of these fat pitches that I see coming along every so often. If there is one thing I’ve learned its that you have to take on some risk when these opportunities present themselves.

Nationstar Mortgage

I would not have bought Nationstar had I not had such a big position in New Residential.

I haven’t followed Nationstar closely for a while. Last year I owned the stock for a short period but exited for a loss after giving up trying to determine how much of their net income would be absconded via a more watchful regulator, and a closing of loop holes like force-placed-insurance.

Fast forward a year. The company’s earnings have taken a hit, in large part due to the aforementioned scrutiny. I’ve found at least one lawsuit that they settled regarding force-placed insurance (here). They paid another $16 million in borrower restitution for in-flight mods, which is where a borrower gets a modification from one servicer even as the loan is being transferred to another. It looks like some of the executives at Nationstar were even sued on allegations that they did not properly disclose just how large the impact of the regulator crackdown to earnings would be. The company paid out $13.9 million in the third quarter and $37.3 million in the 9 month period for legal fees and settlements. Its worth noting that Nationstar still ranks as a below average servicer among customers.

So there are problems. Nevertheless I bought the stock, primarily because, after listening to the third quarter conference call, I felt there were enough signs of a turnaround in place to warrant at least a bump in the stock price. Witness the following:

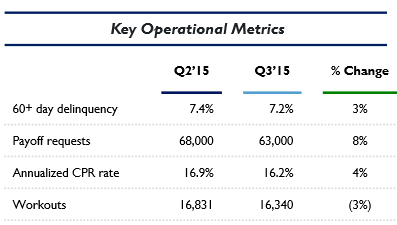

The servicing business had a better quarter, servicing margins were up to 3.6 basis points, which was a 1.3 basis point improvement over Q2.

Nationstar thinks that by the fourth quarter they can get servicing margins up to 5 basis points. 1 basis point of that increase is expected come from improved amortization (which I essentially think means that rates are higher and so they can assume a longer amortization trend) with the rest coming from operational improvements.

For 2016 they are targeting 5-7 basis points of margins. The average servicing unpaid principle balance (UPB) was $400 billion in the third quarter and they ended the quarter with $408 billion UPB. A move back to 5 basis points would be $14 million more in pre-tax profits (or 13c). 7 basis points would be $36 million incrementally (33c).

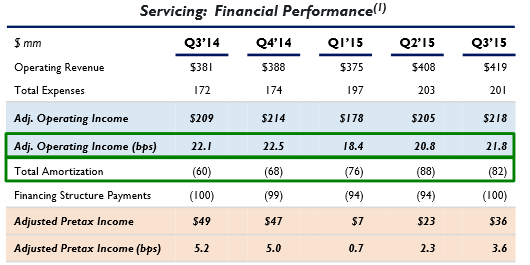

Here is how servicing has trended over the past number of quarters. Note how much of an impact the increased amortization has had. Amortization is going to look a lot better at higher rates.

While Nationstar may not be a leading edge servicer, they are starting to see improvement on prepayments (CPR), which dropped 4% in the third quarter. Delinquency rates have improved from 10.6% to 7.2% over the past year

Net of recapture CPR was down to 13.3% from 14.1% in the second quarter. The overall recapture rate was 28%

In October Nationstar signed a $50 billion sub-servicing agreement with “a major financial institution”. That is 15% growth to their existing UPB. The company said in response to questions that this new UPB will add $30-$40 million of income once fully boarded in 2016.

Also interesting were the comments made around their online home selling platform, Xome. Xome’s results were somewhat underwhelming, revenue was down from $122 million in the second quarter to $109 million as they sold less units than in the second quarter:

But if you parse through the data the decline was generated entirely by REO units sold. So Xome actually saw year over year growth in third party transactions. Third party revenue was up 34% year over year an makes up 37% of revenue now. And its third party transactions that will ultimately determine the value of Xome.

In response to a question regarding the strategic process to find a partner for Xome, Nationstar said that the valuations they were getting from prospective buyers were in the $1 billion range

Overall, earnings right now are in the $1.20 range adjusted for mark to market adjustments of the MSRs. You get a possible upside when value is realized on Xome and you get potentially improved servicing margins as rates rise. Its not a sure thing but there is upside potential.

Patient Home Monitoring

Patient Home Monitoring (PHM) has been beaten up over the past few months. When I bought it in the mid-50 cent range I thought I was getting into the stock as it moved off the bottom. This unfortunately proved to be premature, and it has since slumped back down to the lows.

PHM owns a variety of healthcare businesses that revolve around home based services for patients with chronic conditions. They provide home sleep testing to patients that sleep apnea, home medical equipment such as oxygen nebulizers, and mobility devices, they have a complex rehab business, a pharmacy business – special programs to Medicare Part B programs, and a post acute respiratory care business.

They brought these businesses together via acquisitions, so they are a roll-up strategy, which has become a four-letter word over the past few months and which is partially responsible for the poor stock price performance.

The strategy is that you buy these smallish, single shop operations at an accretive price and then take advantage of their patient database to cross-sell the other products in your portfolio. The former CEO, Michael Dalsin, described it as such in an interview last year:

a lot of these new devices and new technologies and new reimbursement codes are not immediately adopted by the large multi-billion dollar companies in our space. They are adopted by the entrepreneurs who are usually the sales reps of the device company, sometimes doctors themselves think they can make more money doing this care coordination than being a physician. So it’s small little companies all around the country – $10-20 million in sales, usually highly focused on one disease space. So they might only service pulmonology disease. And the reason they do that, ultimately, is because they know that market. They know the sales reps, they know the doctors, they can get prescriptions, they know pulmonology. And as they start developing their market, they become a little bit profitable – they make a couple of million dollars a year – but for us, the most important part of that acquisition is the patient database

Lets take a look at some of the acquisitions. In September they closed their acquisition of Patient Aids for $23 million. They expect Patient Aids to generate $17 million of revenue and $6 million of EBITDA annualized. Patient Aids is a supplier of home health products and services in Ohio, Indiana and Kentucky. Product lines include things like power mobility equipment, vehicle lifts, nebulizers, oxygen concentrators, and CPAP and BiPAP units.

Before Patient Aids PHM made its largest acquisition, Sleep Management. Sleep Management provides ventilators to patients with Chronic Pulmonary obstruction. The management of Sleep Management took on senior positions at PHM after the acquisition was complete. Note that this transition has been partially responsible for the decline in the stock price, as investors were surprised by the CEO shuffle and the fact that the former CEO, Michael Dalsin, sold his stock upon his departure. But according to an interview with Bruce Campbell I listened to on BNN, Sleep Management has grown by 100% over the past three years. This was a $100 million acquisition that they expect will generate $18 million EBITDA annually.

Prior to Sleep Management there were a number of smaller acquisitions.

There was Legacy Oxegyn, which they paid a little over $4 million for and of which they are expected to generate $750,000 of EBITDA. They have a business similar to Sleep Management, offering home-based medical equipment and services for patients with chronic pulmonary conditions in addition to wheel chairs, hospital beds, and other mobility aids. They operate in Kentucky and Louisiana.

Before that was Blackbear Medical, which operates in Maine and provides home medical equipment like canes, crutches and walkers. West Home Healthcare provides a similar set of products in Virginia.

All of these acquisitions are expected to cross-sell the array of PHM products over time. I cobbled together the following table of pre and post-acquisition revenues. They have a reasonably good track record of increasing sales from the businesses they acquire.

I don’t think there is any magic to these businesses. They are basic product and services businesses that generate fairly low (10-15%) operating margins. Those margins can potentially increase after they are brought into the fold and higher margin products, like COPD, are added to the product/services mix. Meanwhile the stock seems pretty reasonable at around 4.5x EBITDA. At this point its basically a show-me story where the operating performance over the next few quarters will determine how well the stock does.

Concordia Healthcare

Last month when I wrote up my reasons behind Concordia Healthcare I kind of rushed through it at the last minute and didn’t do a very good job. The problem with these write-ups is they take time, and trying to write consistently every fourth week doesn’t always line up well with life schedules. For example the weekend of my last write-up was Canadian Thanksgiving.

So I don’t own Concordia right now. I think, however, that there is a good chance I will own Concordia in the future. Given that Concordia is complicated and given the absolute roller-coaster ride the stock has been on it seems that a more thoughtful write-up is appropriate.

As I tried to make clear in my original write-up, Concordia is not a perfect stock. It has the following problems:

- They have taken on a lot of debt with recent acquisitions. Currently at a 6x Debt/EBITDA multiple

- They are labeled baby-Valeant by the financial press which means that every bit of bad news for Valeant is conferred to them

- They have relied at least partially on price increases in the past to boost revenues and lever returns from acquisitions

With those three negatives understood, Concordia also has a number of positives.

- They generate a tremendous amount of free cash from their portfolio of pharmaceuticals

- The product portfolio consists mostly of older drugs that have stable to slightly declining revenues but with predictable future revenue profiles

- At the current stock price the stock trades at a very attractive free cash flow multiple of around 5x

- They are less than 1/10th the size of Valeant, so the potential to continue to grow by acquisitions remains, even if one of the models of that growth, acquisition + price increases, is no longer viable

Concordia’s Acquisition History

Concordia hasn’t been around that long. Their acquisitions started small and grew larger, with the biggest being the recent acquisition of AMCo. Below is a table of all of Concordia’s acquisitions pre-AMCo.

Let’s go through each of these acquisitions in chronological order.

Let’s go through each of these acquisitions in chronological order.

Kapvay, Orapred and Ulesfia

These three drugs were acquired May 2013 from Shionogi. Concordia paid $28.7 million including a $2.3 million inventory adjustment. There was also a pay-out clause that if revenue of Kapvay exceeds $1.5 million per year in the first 18 months Concordia would have to pay 30% of incremental revenue. It looks like they had to pay at least some of that amount.

Kapvay is used to treat ADHD. Ulesfia used as topical treatment for head lice. Orapred is an anti-inflammatory used in the treatment of certain pulmonary diseases such as asthma.

Kapvay and Oraped face generic competition. Both only became generics after Concordia acquired them. Kapvay started to have generic competition in fourth quarter 2013 while Oraped first faced generic competition in fourth quarter 2014. Ulesfia does not face generics yet.

Two of the three drugs experienced price increases by Concordia after they were acquired. From the 2014 AIF: “since acquiring Kapvay, Ulesfia and Orapred, the Corporation has increased such product prices by 52%, 43% and 10%, respectively, without any adverse prescription volume effect.” All of these drugs appear to have prices inline with competition:

Here are sales of each drug:

Its worth noting that Kapvay sales did plummet once the drug was exposed to generic competition in the fourth quarter of 2013.

Its worth noting that Kapvay sales did plummet once the drug was exposed to generic competition in the fourth quarter of 2013.

Photofrin

Photofrin was acquired in December 2013 for $58 million that consisted of $32.7 million of cash and 5 million shares at $5.63 per share. Photofrin is used to treat Esophageal Cancer, Barrett’s Esophagus and non-small cell lung cancer (NSCLC).

Photofrin is kind of an interesting treatment. The drug itself, which is called Photofrin, is administered intravenously. This is followed up by a laser treatment focused on the tumor. The laser reacts with the drug, oxidizing it and the tumor in the process.

I believe that pre the Covis transaction Photofrin was the only drug in Concordia’s “orphan drug division”. Because of the unique combination of drug and device, they do not expect Photofrin to face generic competition.

Prior to being acquired Photofrin had $11 million of revenue in 2011 and $13 million of revenue in 2012. The orphan drug division as a whole had $10.7 million of revenue in 2014, presumably all attributable to Photofrin. In the first half of 2015 orphan drug division had $5.9 million of revenue. Overall Photofrin appears to provide a steady revenue stream. I don’t see any evidence of price increases on Photofrin.

Zonegran

Concordia acquired Zonegran for $91.4 million in cash including approximately $1.4 million for purchased inventory. I believe that what was purchased was specifically the agreement to market the drug in the US and Puerto Rico.

Zonegran is an epilepsy treatment. According to pre-acquisition financials Zonegran has $12.4 million of revenue in the first half of 2014 and $22 million of revenue in 2013:

According to spring presentation in 2014 Zonegran revenue was 8% of Concordia’s $309 million of total revenue or about $25 million.

According to spring presentation in 2014 Zonegran revenue was 8% of Concordia’s $309 million of total revenue or about $25 million.

The essentially flat revenue suggests hasn’t been much in the way of price increases for Zonegran. It looks like Zonegran is inline with the costs of other Epileptic treatments.

The essentially flat revenue suggests hasn’t been much in the way of price increases for Zonegran. It looks like Zonegran is inline with the costs of other Epileptic treatments.

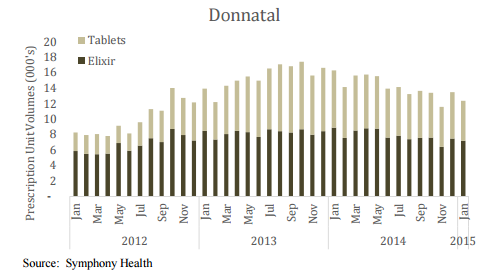

Donnatal

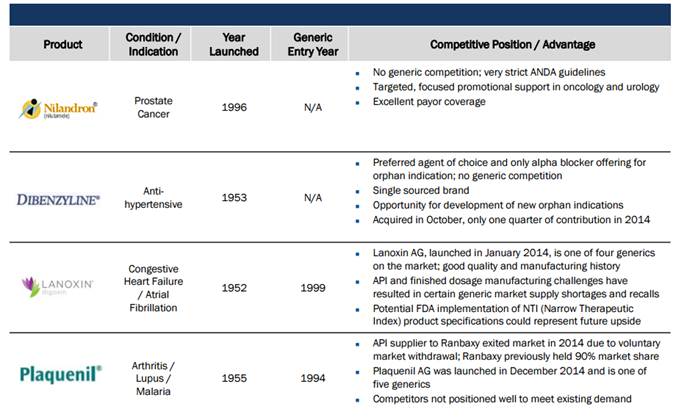

Donnatal was purchased in May of 2014. This was the biggest acquisition Concordia had made at the time Before the Covis acquisition Donnatal made up 41% of Concordia’s revenue, or about $150 million.

Donnatal treats irritable bowel syndrome and has been around for more than 50 years. Therefore it predates the current FDA approval process, it is not a reference listed drug, and, according to the 2014 AIF: “at this time there is no defined pathway for approval of a generic competitor to Donnatal”. Though to qualify this, there are a number of other irritable bowel drugs on the market that compete directly with Donnatal.

Donnatal is probably the most notable example of price increases. The CEO of Concordia admitted as much last week during a BNN interview (segments one and two here and here). What’s interesting is that while Concordia did raise the price of Donnatal significantly after acquiring the drug, similar cost increases appear to have been made even before the acquisition. Also worth noting is that Donnatal is well within the price range of its competition:

Here is Donnatal prescription volumes over past few years:

Covis

Covis

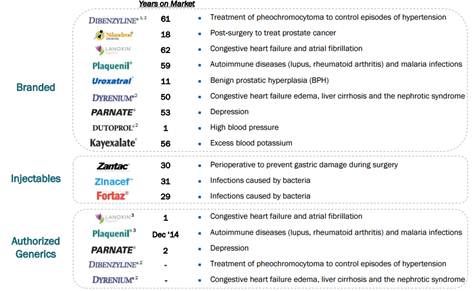

Covis was acquired for $1.2 billion on April 21 2015. Things begin to get more complicated here, because Covis is a big acquisition with many drugs. Covis added 18 branded or generic products. Here is a list of what they got:

Of these products Concordia focuses on the following four as being the most important:

Of these products Concordia focuses on the following four as being the most important: What’s key about most (but not all) of these products is that they are old, they have generic competition, and they have stable or falling demand profiles.

What’s key about most (but not all) of these products is that they are old, they have generic competition, and they have stable or falling demand profiles.

I haven’t been able/had time to dig up information on the individual drugs. As a whole, Covis had revenue of $47 million to $52 million in the fourth quarter of 2014, so just before acquisition. 2014 revenue as a whole was was estimated by Concordia to be between $140 million to $145 million at the time of acquisition.

Post-acquisition, Covis had revenue of $38.7 million in the second quarter. Given that the acquisition closed on April 21st, that revenue accounts for 68 of the 91 days in the quarter, so pro-forma over the full quarter revenue would have been $52 million, which inline with the fourth quarter results.

Amdipharm Mercury

Concordia sells the Amdipharm Mercury acquisition as a way to increase the diversity of their revenue and expand the overall platform, which sets them up to more easily compete in future acquisitions. The acquisition is a departure from past acquisitions, which targeted either a drug or portfolio of drugs, as Amdipharm is a complete company purchase.

This wasn’t a cheap acquisition. The total price at the time of the stock offering was $3.5 billion. Concordia paid around 12x EV/EBITDA based on a little less than $300mm EBITDA for Amdipharm. This included the assumption of $1.4 billion of Amdipharm debt. They also issued 8 million shares at $65 USD. The acquisition is closer to 10x EBITDA for those of us looking at the stock now with the shares having depreciated significantly. But that is no consolation for the folks that bought at $65.

The company describes the acquisition as accretive to earnings, and I believe that’s true based on my own number crunching, but you have to realize that its accretive because they are taking on so much debt. The debt is roughly $3 billion of the $3.5 billion acquisition price. The accretion is because this is a very profitable drug portfolio, so even after subtracting interest costs there is significant earnings remaining on the bottom line. The downside is that it made Concordia very levered up.

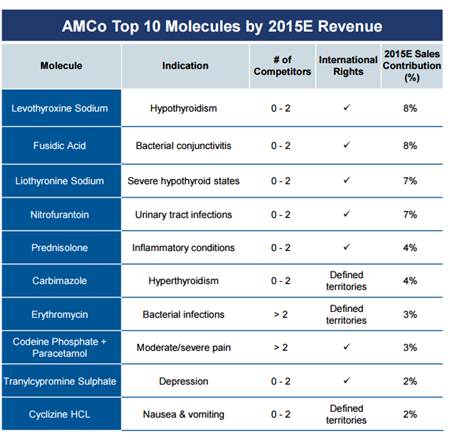

The benefits are diversification, as Amdipharm was primarly in the UK and Europe. Concordia is now only 40% exposed to the US and 10% exposed to state funded plans, a global footprint, which Concordia suggests will make it easier for them to cross-sell their existing pharmaceuticals and expand with further acquisitions. AMCo also appears to have a fairly stable product base, most of them have been off-patent for a long time, many of them are difficult to manufacture, and 88% of the portfolio have two or fewer competitors. Of course cynically you could look at these points and say what a great portfolio to implement price increases on…

Amdipharm has 190 products, which makes it a lot more difficult for me to analyze. Here are the top ten by revenue:

Valuation

What continues to make Concordia tempting is that on a free cash basis they trade extremely cheaply. The company’s guidance for cash earnings is $6.29 to $6.77 per share. It looks to me like cash earnings has followed closely to free cash flow.

But I’m nervous about the debt and the short-selling. Total debt is around $3.5 billion. Given the company’s EBITDA estimate of $610-$640 million for 2016, Concordia trades at about 8x EV/EBITDA. On a pure enterprise value basis that leaves them somewhat undervalued compared to other pharmaceutical companies (which seem to go for around a 10-11x EBITDA multiple).

Clearly there was short-selling involved that caused the precipitous drop to the teens a few weeks ago. That they have their sights on Concordia is cause for concern for owning the stock. As long as Valeant is in the headlines Concordia is at risk whether its warranted or not.

Other Adds: Alliance Healthcare, Nevsun Resources, Northstar Realty, Acacia Research

I bought Alliance Healthcare because I thought that at $8 it was getting just a little to cheap. At $8 the market capitalization was only a little more than $80 million. While the company’s debt remains enormous ($507 million) they continue to generate a lot of free cash ($40 million in the first nine months of the year, though this is before minority interests so the actual number attributable to the company is somewhat less than this). The stock has been under pressure since their major shareholder, Oaktree Capital Management, sold their shares at $18.50 to Fujian Thai Hot Investment Company. Thai Hot now has a majority interest in the company but as part of the deal has agreed to make no further purchases of shares, which essentially prohibit it from supporting their position. The whole thing is weird, but at $8 I have to think most of the damage is done.

I bought Northstar Realty and Nevsun for similar reasons. Northstar is a hated property REIT mostly operating in the healthcare and hotel sectors that has been beaten down to a 15% yield. I don’t see anything particularly wrong with their property portfolio, and I suspect that the incessant selling has more to do with year-end and being a former hedge fund darling.

Nevsun is an $800 million market capitalization (Canadian dollars) copper miner with almost $600 million of cash on the books. While the low copper price has hurt them, they are still generating free cash. They operate one mine, called Bishna, in Euritania. While I admittedly haven’t had time to go through the third quarter data, I bought the position off of the second quarter numbers where they showed $97 million of cash flow from operations and $53 million of capital expenditures, meaning decent free cash generation. I also like that they are transitioning from being a primarily copper miner to a copper and zinc miner in 2017. The supply/demand outlook for zinc looks pretty interesting and so they may benefit from higher zinc prices right around the timeI’ll try to talk about these positions in another post, as this one is already way, way too long.

Acacia Research partners, a patent litigation firm that partners with patent owners to realize the value of their patents, got creamed on a pretty terrible headline quarter. I bought after the carnage had appeared to run its course. So we’ll see if that’s the case. At the current price the company has a $330 million market cap and $168 million of cash on the balance sheet. The thing here is that a bad quarter doesn’t necessarily mean anything about future performance. Acacia has a portfolio of patents that they are moving towards litigation. The companies that they are litigating against generally hold-out against settlement until the very last minute. The poor revenue number this quarter (it was $14 million, versus $37 million last year in the third quarter and an average of $37 million the last two quarters) simply reflects delays in a few of their cases, some of which were actually brought about by evidence that strengthened Acacia’s case. From the third quarter conference call:

The third quarter developments created paradoxical outcomes. On one hand, our marquee portfolios were strengthened through Markman inter-parties review and new patent issuance wins, and now have even greater future value. But on the other hand, we experienced a delay in collecting on that value.

This is a stock that is going to whipsaw up and down on what will always be very lumpy results. I think you have to buy it when the whipsaw down is extreme. There is a very good writer on SeekingAlpha (he also has his own blog) who follows the stock closely and wrote a good piece on the company here.

What I sold

I reduced my position in the few gold stocks I bought after the latest Federal Reserve view on the economy came out. I still hold a couple small positions here because for the miners outside of the US, even as the price of gold falls their costs are falling just as fast and in some cases faster. The market doesn’t care about margins yet though, so there is no point fighting the headwind too hard.

I bought and sold Digirad within the month for a gain. I bought Digirad on the morning of their takeover of DMS Health for $35 million. The acquisition was accretive and after doing some quick math, on the morning of the acquisition the combined entity had a $77 million enterprise value and a 4.5x EBITDA multiple. I thought this was likely too low so I bought, but the stock has risen since to a more respectable level and so I have since sold my shares.

I bought and sold Enernoc for a loss. I played the swings from $7 to $9 on Enernoc successfully a couple of time an then got burnt when they released quarterly earnings. Fortunately while it was pretty clear that the earnings were awful, the market gave a small window first thing in the morning to get out in the $6’s. I took that opportunity.

I sold Gilead for a loss when I clearly shouldn’t have. I did this before I made the decision to hold to my convictions a bit more firmly and I got spooked out on a dip below $100 that was clearly more of a buying opportunity in retrospect.

And of course I sold Valeant, for a loss, but thankfully well before things really got out of hand with the stock. Better to walk away when things begin to smell bad.

Portfolio Composition

Click here for the last four weeks of trades.

{kind=link}

{kind=link}