Week 231: Tax Loss Buying

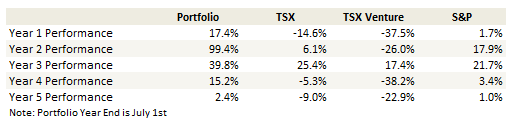

Portfolio Performance

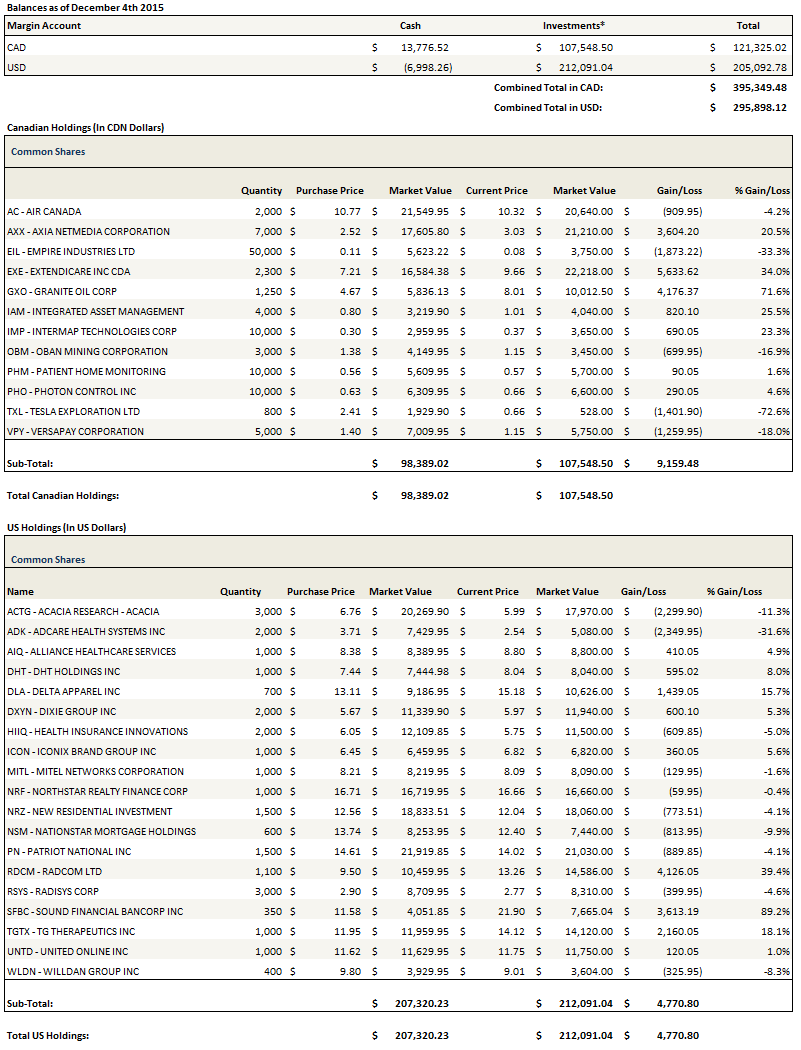

See the end of the post for the current make up of my portfolio and the last four weeks of trades

Monthly Review and Thoughts

I didn’t make a lot of trades this month. I added a couple of beaten down stocks (Dixie Group and Iconix Brands), added to a couple of existing beaten down positions (Acacia Research and Health Insurance Innovations), added to a less than beaten down position (Axia NetMedia) and sold out of a few poorly performing positions in PDI Inc, Nevsun, Independence Realty and Hammond Manufacturing. I also reduced two of the three out-sized positions that I talked about in my last update, New Residential and DHT Holdings on pops. At this point the only really uncomfortably large position I have is in Air Canada, a stock that seems to do nothing but go down.

It is my experience that the last three months of the year can be very quirky. The confluence of redemptions and tax loss selling leads to seemingly endless downward moves. While its easy to describe this as an obvious opportunity when you limit yourself to generalizations or retrospectives, the reality is that it is not so easy to buy that which has collapsed when it goes down every day.

I have plenty of examples of stocks I am following that are examples of this. Most are either yield stocks or energy names of one type or another.

First the REITs. I could pick from a litany of REITs here but I’ll focus on Northstar Realty because I know it fairly well. The stock can’t seem to get out of its own way, having endless down days followed by briefing sharp rallies that are followed by further relentless selling pressure that can’t be overcome by even a 2% up day by the market like we had on Friday. Northstar has a yield 15%. The dividend is backed up by real estate assets, mostly healthcare and hotels. On September 29th the company announced a $500 million buy back. Given the current market capitalization of a little over $3 billion, this is not insignificant. On the negative side, the stock is externally managed, something that seems to be the kiss of death right now, and its hotel properties have underperformed lately. Risks for sure, but at what point are those risks priced in?

Another example is Navios Maritime Partners, a dry bulk/container shipper. Navios cut their dividend in November from $1.77 to 85 cents. They operate in an extremely tough market, but at the time of the dividend cut they made a strong case that the current level was fully supported by existing contracts with almost a 9 year period. This outlook was confirmed in a solid analysis posted in Seeking Alpha. The stock has went down relentlessly both pre and post dividend cut. It’s at $270 as of Friday’s close so its about a 30% yield.

A third example that I just started looking at over the weekend is Suncoke Energy Partners. Suncoke owns three facilities that turn coal into coke for steel making. The company has a market capitalization of $300 million versus a tangible book value of around $500 million. Earnings for the first nine months were $1.16 per share and full year estimates are $1.50 per share. The stock trades at $6.59 at Friday’s close. The steel industry is hurting and Suncoke’s partners are expected to shutdown mills that Suncoke supplies. On the other hand Suncoke has take or pay contracts and their customers are large producers: US Steel, ArcelorMittal USA, and AK Steel. So are they really doomed, as the stock price performance (down from $15 since August) suggests? Or will the partners pay and this a great buying opportunity for assets that are temporarily impaired?

Here is one from the energy sector. Surge Energy. I’ve owned it before, in the late spring/early summer. They are currently producing around 14,000 boe/d with 80% of their production being liquids. In the first half of 2015 they generated $85 million of funds from operations with the oil price (including hedges) averaging a little less than $60. In the third quarter they generated $17 million of funds from operations on an oil price of $41, so about the current price. Capital expenditures in the third quarter were $17 million. The company has about $140 million of debt, so less levered than most. Is oil destined to float around the $40 mark forever, in the process sending basically the entire North American industry into bankruptcy, or will it eventually find a higher equilibrium? If it does what will one of the survivors, as Surge would surely be, trade at? At 5x cash flow on $60 oil Surge would be worth more than 50% more than it is today.

And one last one from energy infrastructure. Willbros Group. Management has been much maligned and struggled to turn a profit in the past. This year, perhaps because of the pushing of activist investors, they’ve sold off a number of their divisions, raising cash and paying down debt. With the recent sale of the Professional Services segment to TRC Solutions for $130 million they have reduced debt to under $100 million and they have cash on hand of $50 million. With 63 million shares outstanding Willbros has a market capitalization of about $170 million. They generated $2 billion of revenue in 2014 and this year, even after the sales of multiple divisions and the devastating downturn in the energy industry their revenue run rate is close to $1 billion. The company will likely not be profitable until oil prices turn, but when they do there is a lot of leverage to margin improvement and incremental contracts.

So there are some names. None are sure things, all can have cases made for and against. My point is simply that at this time of year there tends to be real bargains, but pulling the trigger is a lot harder because there are also always real questions, and the answers are rarely clear.

The stocks I’m going to talk about below, with the exception of Axia NetMedia, all positions that fit into this mold. These are stocks that have been beaten up, that have warts, but that I feel are overdone. I just hope that I am right in more cases than I am wrong.

Dixie Group

Dixie Group is a company I have owned in the past, followed for a long time but held out from buying until it got to a price that I thought presented very little downside.

Dixie Group is a supplier of commercial and residential carpet. They have 16 million shares outstanding at $5.50 for $88 million market capitalization. They have $131 million of debt that consists primarily ($84 million) of a revolving credit facility that comes due in 2019.

Dixie Group has undergone a lot of changes in the last couple of years. They made a number of acquisitions of high end commercial and residential businesses in 2013 and 2014, and have spent the last year digesting the capacity.

The results so far have been lukewarm. Sales have shown some slight growth while the rest of the industry has seen slight declines. But the increased scale has not translated into improved profitability.

Some of this is skewed by continued restructuring and sampling costs, and some of it is because there have been employee and quality issues that have arisen along with the capacity additions.

Revenues in the third quarter was $109 million which is flat year over year and up somewhat from the first half. Ignoring working capital changes cash flow was in the third quarter was $8.4 million.

Even though the headline showed a big miss on both revenue and earnings, I didn’t think it was a terrible quarter in a lot of ways.

Gross margins were up to 26% which is a little above the 25% I had been hoping for two years ago when I was looking at the stock. G&A is rising more than it should and this appears to be due to restructuring costs, increased medical expenses, consolidation of offices. They introduced a number of new brands over the last few quarters and those new brands are requiring higher sampling costs. So there are lots of one time things.

But I think that it is the quality problems that are holding back the stock the most. They said the impact to quality in the third quarter was 1% to their gross margins. While they suggested this would decline in the fourth quarter, they weren’t very specific about how quickly that decline would occur and implied it could persist into the first quarter of 2016.

I don’t think the market likes the uncertainty. Heading into earnings the stock wasn’t that cheap if it was producing no earnings and EBITDA on a $20 million run rate. But after the collapse from $9 to $5 much less is priced in. The stock trades at a little under book value.

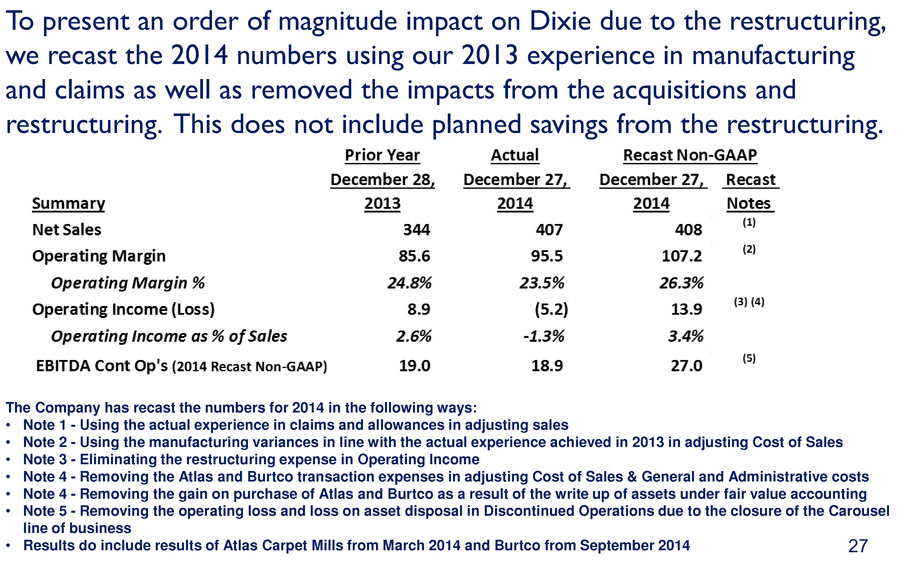

In their third quarter earnings presentation Dixie presented the following pro-forma to restructuring 2014 earnings.

So if the dust settles you are looking at a $27 million EBITDA company with a $219 million enterprise value. So about 8x EV/EBITDA. Its not incredibly cheap but with some growth the equity portion of that enterprise value could quickly grow back to the $9 level.

So if the dust settles you are looking at a $27 million EBITDA company with a $219 million enterprise value. So about 8x EV/EBITDA. Its not incredibly cheap but with some growth the equity portion of that enterprise value could quickly grow back to the $9 level.

Now of course this is the carrot not a forecast. I don’t know if Dixie will regain operating momentum, get past their integration issues, and begin to grow the business. They have the capacity now to produce $550-$600 million of carpet. They just need to find the customers. What I do know is that at the current price their is not much expectation priced into the stock. I think its worth a position, one of those stocks where if anything good happens its bound to go significantly higher.

Acacia Research Third Quarter

Acacia had a really bad third quarter. Revenue was $13 million down from $37 million in the third quarter last year and a $44 million average revenue over the prior two quarters.

So the stock got clobbered. For four weeks it went down almost every day, from the $9 level to almost $5. Was it deserved? Well, the thing about Acacia is that revenue is always going to be lumpy and one quarter does not suggest any particular trend. The company generates revenues primarily through the settlement of patent litigation. The nature of the business is that the counter-party in the litigation is unlikely to settle until the very last moment, usually right before the trial starts. So Acacia’s revenue recognition is always at the mercy of court dates and negotiations.

The poor third quarter was due to delays on litigation on a number of their patent portfolios. This quote, from the third quarter conference call kind of summarizes their thoughts on the quarter:

The third quarter developments created paradoxical outcomes. On one hand, our marquee portfolios were strengthened through Markman inter-parties review and new patent issuance wins, and now have even greater future value. But on the other hand, we experienced a delay in collecting on that value.

In particular, their Adaptix portfolio is going to trial against Alcatel-Lucent and Ericsson but that was postponed by a quarter. This is because of the introduction of evidence that actually strengthened Acacia’s case but required delays for all parties to review. They also announced that they had won two infringement cases on their Voiceage portfolio (HTC and LG), but that it would take time for a formal opinion from the German court that would lead to a settlement. Subsequently, Acacia announced a settlement with HTC on November 17th.

Acacia’s business model is to partner with patent holders, applying their legal expertise in patent litigation to help the patent holder maximize the value of their asset. On that note Acacia said that in the current environment they expected to be able to partner with other patent holders without putting up their own capital going forward. The environment was a “buyers market”.

At a little over $5, where I was buying, the company was getting close to its cash level of $3 per share. Even here at $6 it still doesn’t attribute a lot of value to the patent portfolio. There are a couple of good SeekingAlpha articles that discuss the stock here and here.

Health Insurance Innovations Third Quarter

Health Insurance Innovations (HII) had a so-so third quarter. The revenue number was a little lower than I expected at $25.8 million versus the $28 million I had been hoping for.

But there are a number of changes going on at HII that make the story interesting enough for me to add to my position. First is the development of an online insurance portal, AgileHealthInsurance.com. They have had Agile up and running for a few months now, and reported that it had accounted for 1,300 policies in July and 5,800 policies in Q3 (suggesting it averaged 2,250 policies in August and September). Second, through the addition of a number of former sales personnel from Assurant, HII has expanded their broker channel significantly.

Overall the business is progressing. Total policies in force increased in the third quarter to a record 137,000, up 31.7% year-over-year and 21.2% sequentially.

The revenue recognition associated with policies procured online is part of the reason for lower revenue. Unlike broker or call center procured policies, those come from Agile have revenue recognized over the full term of the policy while the customer acquisition cost is taken up front which in the short run will depress margins.

Going forward HII expects to gain from a shorter ACA enrollment period and the reality that premiums on ACA plans are “rising rapidly”.

On the third quarter conference call management seemed quite upbeat about how well they are doing through open-enrollment:

Our short-term medical, our hospital indemnity plans, they really fit the need and we’re seeing, unlike last open enrollment period, a dramatic increase in our sales. We can’t wait to share with you the fourth quarter results when we get to that point. This is for the first time, we’re really playing offense during open enrollment versus last year, we were playing a bit of defense.

The fourth quarter will be interrupted by the ACA period, which began in November. Still, I think that if the company can put up a decent showing during this period the market will take notice. Perhaps we are already seeing the start of that with the recent $1 move up.

Iconix Brands

It’s been a while since I have been drawn into a company with a recent accounting scandal. And while I am wary that these sort of situations often go down far further than I expect, I also know that in many cases the eventual profit can be quite significant if you can get through the rough waters.

Iconix is a company that essentially rents out the usage of their brands. They buy the rights of well known clothing and entertainment brands and then for a price licenses the usage of the brand by department stores and manufacturers. Their portfolio of brands encompasses a wide variety of low to high end men’s and women’s fashions as well as well known entertainment brands like Peanuts and StrawBerry Shortcake.

Its a pretty good business that has consistently generate 30% margins and significant free cash flow.

The company ran into problems earlier this year. In March the CFO resigned. Two weeks later the COO resigned. And then the biggie in August, the CEO resigned. At the same time they announced their second quarter results and said that they would be reviewing the accuracy of past financial statements.

This was followed up on November 5th by a mea culpa by the new leadership team that past financials were not accurate and would have to be restated. Shares which had already fallen from the $30’s to the mid-teens, got halved again to around $7.

What’s interesting though is that the accounting irregularities revolve entirely around the income statement. Here is what the interim CEO, Peter Cuneo said on the third quarter conference call.

This review has identified errors regarding the classification of certain expenses as well as inadequate support and estimation of certain revenues, and of retail support for certain licenses. As such, we will restate our historical financial statements for the fourth quarter of 2013 through the second quarter of 2015.

A table detailing these adjustments was included in last Thursday’s press release. What should be emphasized is that the amounts of the restatements have no impact to 2013 net income. They do result in a small reduction of approximately $3.9 million or 2.5% to 2014 net income, and they are slightly positive for 2015 net income.

Further, these changes do not impact cash, do not impact historical free cash flow and do not impact debt covenants or securitized net cash flow as defined in our securitized financing facility. In fact, gross collections for our securitized brands are up 3% for the first ten months of the year, which reflects the strength and stability of the assets in the securitization.

Now that its down almost 80% Inconix, with 48.5 million shares outstanding has a market cap of about $325 million. Iconix also has a lot of debt, $1.47 billion. Included in that debt is a $300 million 2.5% convertible that comes due in June of 2016. Normally this convertible would not be an issue. Given the company’s problems they may have to fund its repayment out of cash. When I look at the cash on hand and cash flow they can generate from operations, they should be able to do that without too much problem.

The bullish story here is simply that once the accounting issues are behind them, what will be left is a company that generates significant free cash and trades at an extraordinarily low free cash multiple. Iconix issued the following guidance for 2016:

We expect organic growth to be flat to up low single-digits driven by double-digit growth in our international business and U.S. revenue down slightly. We’re including no other revenue in our 2016 forecast.

Reflecting these expectations, our 2016 guidance is as follows: We expect revenue to be in the range of $370 million to $390 million. We expect non-GAAP diluted earnings per share to be in the range of $1.35 to $1.50 and we expect free cash flow to be in the range of $170 million to $185 million.

Free cash of $170 million is $3.50 per share.

There are hurdles to reaching that guidance to be sure. On the third quarter call they said their mens apparal segment was performing poorly because of poor performance by Rocawear and Ecko, both mature brands that may be reaching end of life.

Also one of their biggest brands is Peanuts which is experiencing some headwinds. Peanuts accounts for somewhere in the neighbourhood of $100 million of licensing revenue, so 25%. While the recently released Peanuts movie has done fairly well in the box office and in ratings, it is suffering on the merchandising side because it has to compete with Star Wars for shelf space over the Christmas season.

Nevertheless, even with the debt, even with the accounting issues, it seems too cheap to me. Unless there is something further that comes out on the accounting front I think the stock has to move higher at some point next year. It could go down more over the next few weeks with tax loss selling, but I can’t see it staying here for good. The fundamentals, un-obscured by fraudulent accounting, just aren’t bad enough to justify it.

Axia NetMedia

I’ve owned Axia for years now and recently added to my position. The company has 63.4 million shares outstanding, and at its current price of $3 they sport a $190 million market capitalization.

Axia owns and operates fiber networks in Alberta, France and Massachusetts. Each of these networks supplies high speed connections to smaller cities and towns throughout the area.

Axia has already built fiber trunk lines that provide high speed connections to the major centers in each of their networks. Now they are in the process of signing up homes and offices and building out fiber to individual customers (called FTTH and FTTO respectively). The addressable market is over 1 million homes only counting the 20 largest of the 400 communities that the fiber reaches.

In Alberta they have completed at pilot FTTH in one community (Vulcan) and are in the process of ramping up in Drayton Valley and Lloydminster. The package they offer (which I believe is via third party providers) is $59 per month for 25Mbps rates. In Massachusetts they offer 100Mbps rates for $49 per month.

This doesn’t seem to me to be a bad package for small town households that previously were limited to slower cable or satellite connections that was intermittent or experienced outages. Having lived in a small town and having had first and second hand experience of the existing internet options I can say that the following commitment would be a major step up:

We are confident that Axia provides the most reliable Internet possible. In fact, for business we commit to 99.9% availability and a maximum 4-hour mean time to repair in the rare event of a fibre cut.

You can view the Canadian and US plans here and here.

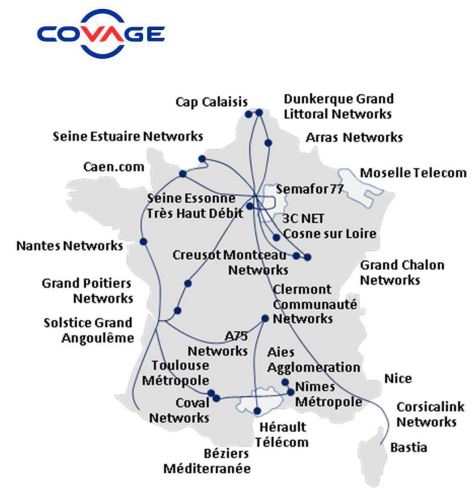

In France the opportunity for growth is even better than in North America. Covage, of which Axia has a 50% ownership, has 10,600 km of fiber including 3,400 km of fibre backbone.

In the third quarter Covage’s customer connections were up year over year 36% for FTTO and 61% for FTTH. On the third quarter conference call Art Price (the CEO of Axia) said that “Covage has sustained growth on its existing networks and has tangible FTTO and FTTP opportunities that could more than triple Covage’s size.”

In the third quarter Covage’s customer connections were up year over year 36% for FTTO and 61% for FTTH. On the third quarter conference call Art Price (the CEO of Axia) said that “Covage has sustained growth on its existing networks and has tangible FTTO and FTTP opportunities that could more than triple Covage’s size.”

Subsequent to quarter end Covage won a large FTTO contract that encompasses an additional 22,000 businesses. Covage currently has a little over 7,000 FTTO connections. Bringing on 10-20% of these additional sites would mean a large uptick.

Earlier this year Axia won a contract to provide Fiber to Seine et Marne that will pass through 319,000 homes. Right Covage has around 7,000 FTTH connections. So think about that for a second.

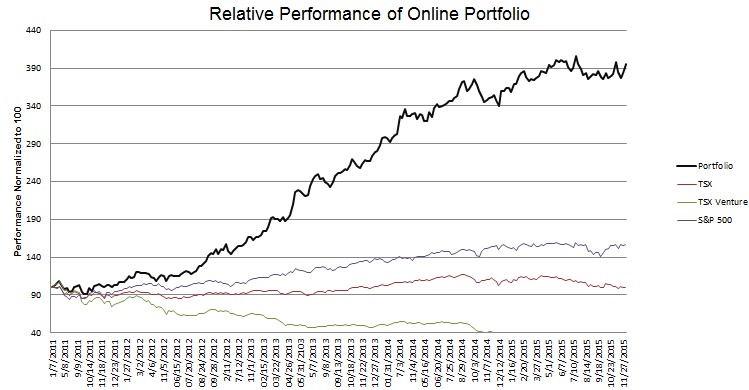

Right now they are growing steadily (see chart below) but the profitability of this growth is masked by the continued build outs of networks and connections.

On the third quarter conference call they had a long discussion talking about the need for capital in the business they are in and what this means the eventual end game has to be. I think its worthwhile reproducing the response in full:

Well, we’re looking at different options, and the way the company is harnessing the capital markets. I would say in the broad, we’ve been a company that is incrementally growing from a small size to a €200 million market cap size. But now we’re a company that has opportunities in front of us that are multiples of our current market capitalization.

And if we were just going to make the comment that where is this fiber infrastructure ultimately destined in the capital markets, well, clearly this fiber infrastructure is going to end up in billion dollar equity market cap, with capital structure that can issue its own bonds for debt. I mean that’s where this kind of investment ultimately ends up and we all recognize that.

So the question is what’s the path to get to that point? Is that path an incremental path similar to the one we have been on, but moving to a different shareholder class in a different size or is it some other path? And the Board is actively looking at that set of issues and looking at it in the context of the current market and looking at in the context of our investment opportunities having this sort of North American and France character, which some of the capital markets looks together at and other parts of the capital market look at that as segmented.

So we’re in that process, because besides the opportunity in front of us, in order to make those available or actually take those opportunities on, of course there is quite a bit more capital involved and our path is either we line up the company for that capital to rate shareholders’ evolution or we aren’t able to take advantage of the number of opportunities in front of us.

That’s a pretty interesting comment. It basically says that they see the bottleneck and they are going to figure out what is the best way to address it. It means they either are going to get the market to buy into the Axia story (and produce much larger share price) or try to find an acquirer with the financial clout to build out the infrastructure that they require to grow.

Either way it seems like a likely win for shareholders. I think Axia is in the right place at the right time. I’ve been adding.

Portfolio Composition

Click here for the last four weeks of trades.

{kind=link}