Community Bankers Trust: Gives a Little Bit of Green in the Sea of Red

In a week where most stocks I own (and most stocks period) went down, there were a few bright spots in my portfolio. Almost all of those bright spots were regional banks. The best of the bunch, by far, was Community Bankers Trust (BTC). Community bankers trust reported its second quarter earnings last week. Evidence of a nascent turnaround in their operations are likely responsible for the interest in the stock.

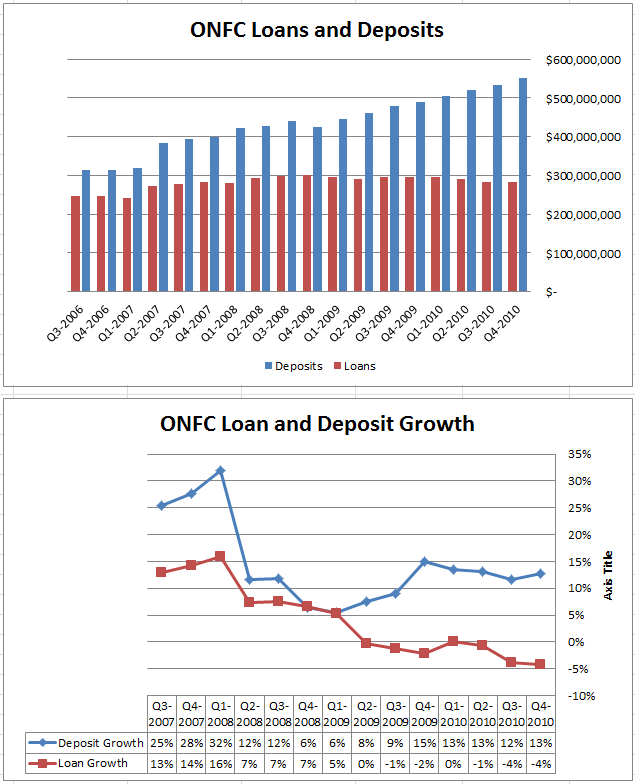

I only have a small position in BTC because, to be honest, they are a bit of a flyer. Unlike my other bank holdings (ONFC, HFBL, and recently XBKS) has some nonperforming loan issues.

Still there are some signs that the bank is turning things around. First of all, there has been a lot of insider buying going on in the last couple of months.

Second, delinquent loans have been coming down, as have charge-offs. On the Q2 conference call management talked of definitively turning the corner on their nonperforming loan issues. They also suggested that new loan growth would begin to kick in soon.

(note that the 30-89 day number for Q2 won’t come out until the 10-Q is filed. This is an important number and something to watch for when the 10-Q comes out).

Finally, the company is trading at a severe discount to book value. Tangible Book value is $3.57, meaning that the stock is trading at about 39% of tangible book. Moreover, unlike some banks, tangible book hasn’t proven to be a continuously shrinking metric. Book value has remained relatively constant for over a year now.

BTC is one to keep an eye on. If there is continued progress on their non-performing loans, and charge-offs continue to fall, I think this is the sort of stock that could easily triple from here. I will watching closely for their 10-Q. Confirmation that loans past due fell further in Q2 would likely lead me to buy more.

{kind=link}