A couple of weeks ago Gecko Research (which seems to be, oddly enough, a Swedish based, Canadian Gold junior company research firm) put out a report on Atna Resources. The report is available here.

Most of the report is full of your typical fare. These are their properties, this is their management, yada, yada, yada.

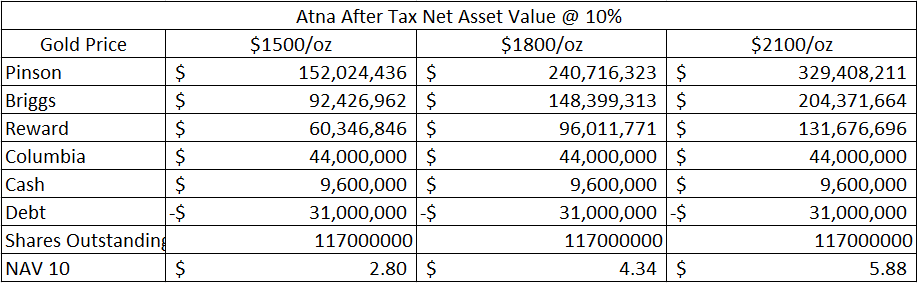

Then I got to this table:

I did a double take when I looked at the 2013-2016 cash flow numbers. $1 per share in 2013? Is that possible? Could Atna really generate that much cash flow that quickly?

The work I have done

When I looked at the table and contemplated the numbers it occured to me that I had never actually looked at the year by year cash flow that the company might generate once Pinson is up and running. What I spent quite a long time looking at was the net asset value of the company. I did that analysis right before Christmas.

What I found out was this:

After I came up with the NAV estimates I basically wrapped up my analysis and put it under the Christmas tree.

See, I don’t have oodles of time to do miscellaneous research. When I get a set of numbers like the one’s in the table above, where the only conclusion that can be drawn is table pounding buy, I don’t tend to spend too much more time splicing out the details. Atna is going to make a lot of money and that is not baked into the price of the stock. End of story. Go buy the stock.

Anyways that was my thinking at the time. So I never really looked at the year by year cash flow in any detail. Until I read the Gecko report and that made me curious. Could it really be that high?

Looking at cash flow

The best way to check the numbers is to run them yourself. I took the inputs Gecko provided and created my own little cash flow spreadsheet.

The first thing that should be pointed out is that Gecko is using, to put it mildly, optimistic gold prices. I don’t think there are any analysts out there using $2600 per ounce gold for 2016.

Second, I had to make some assumptions. For D&A I assumed a constant $200/oz produced which I think is likely going to be on the high side. For G&A I used $8M per year, which was based off of the average of what I saw from some other companies (Argonaut, Aurizon, Allied-Nevada, Alamos), and no I did not intend to only compare the company against other companies that started with the letter A.

Exploration was assumed to $10M per year, which may be on the high side but Atna has a lot of other properties so I wouldn’t be surprised if they start working on them once they have the cash.

Taxes are based on the nominal rate provided by the company.

The results I came up with were not too far off what Gecko did.

And using the BMO price deck…

Since I had the spreadsheet built I started to look at other scenarios. Probably the most illustrative was to look at what Atna might be generating based on the BMO price deck. The BMO price deck could be considered to be a “realistic” price deck, with the term realistic being defined as generally accepted until it is proven to be horribly wrong.

But that is for another rant.

BMO is predicting the following gold price going forward:

You still get some pretty gaudy cash flow numbers:

Financing?

Another point that was brought up in the Gecko report was the chance of a financing. Gecko thinks this is going to happen. I hadn’t really thought about the possibility too much until they brought it up, but I can see the logic.

Even though Atna has the possibility to grow only from internal cash flow, we think that Atna will raise money through an equity financing some time during H1/12, likely during Q1. We believe C$20 million will be sufficient to take Atna through 2012 with the development of Pinson and to fast track the studies of Pinson Open pit. This will also assure that long lead-time equipment for the Reward Mine will be ordered in time. We assume an equity raise will be done at C$1.50 by issuing 13.33 million shares.

It’s a fair point. While they can probably squeeze by without one, they don’t have much cushion. As long as its done at a high enough price, I have no problem with it

Haven’t sold a share

Over the past month Atna has gotten its butt kicked along with the rest of the gold sector. It probably went too high too fast and now its come back to earth.

I don’t love gold right now. With the economy improving I can imagine that selling pressure will remain on the metal. My favorite sector right now, the regional banks, are the antithesis of gold. Its hard to imagine both going up together.

Yet I haven’t sold a single share of Atna. I bought more shares when it dropped into the $1.12-$1.15 range late last week. I don’t really expect much upward pressure on the shares until they begin to announce more news about Pinson. In particular I think the full permitting of the project would be big news.