New Position in MYnd Analytics

Well we are less than a month into the new year and I am already breaking a rule. Rule #2, stay away from illiquid stocks. So what do I do? Two days later I buy a stock that trades 20,000 shares most days.

That said the stock has had a lot of volume the last few days. So it’s not illiquid at the moment. And I am keeping my promise to write more. So there’s that.

Here’s the scoop.

Mynd Analytics (MYND) has a not-so-interesting legacy business of providing psychiatric help via video conference to patients in remote areas. They have a second not-so-interesting business of offering a platform (called PEER) that helps doctors prescribe for psychiatric conditions.

Two not-so-interesting businesses are not a good reason to buy a stock. What is interesting here is a merger that was announced a few weeks ago. Mynd Analytics is merging with a private biotech firm called Emmaus.

Emmaus has a much more interesting business than anything Mynd has, so this is more of a reverse takeover kind of merger where the new company is going to be Emmaus, not Mynd. In fact, exiting Mynd shareholders are going to get about 5.9% of Emmaus. They are also going to get a spin-out of the two not-so-interesting businesseses into a separate company.

So while those businesses are not very interesting to me, the market was still saying they were worth up to $1.50 a few months ago. So basically as a shareholder I get what I already had, plus now I get a piece of Emmaus.

Getting a piece of Emmaus is interesting. Emmaus is in the early stages of marketing a drug called Endari. Endari is approved to treat sickle cell disease.

Sickle cell disease (SCD) is an awful sounding inherited disease where your blood hardens, which can cause stroke. There are 100,000 patients in the U.S, another 80,000 in Europe, and over 400,000 in Africa and the Mideast.

There is only one treatment on the market for SCD. It’s called hydroxyurea and its been on the market for over 20 years. It helps in most cases but it’s not a cure and it produces a lot of adverse side effects in patients.

Endari has went through FDA approval trials and its efficacy has been demonstrated. It provides improvement in adverse events over the placebo, both on its own and when used with hydroxurea. Importantly it is well tolerated by patients.

That last clause in the sentence is important, because physicians can prescribe hydroxurea and Endari together.

While it’s expensive to prescribe, insurance companies have been very willing to add Endari to their list. Why? Because adverse events for sickle cell patients are severe. They require ambulances, hospital stays and are extremely expensive. Endari comes at an ASP of $30,000 ($20,000 net to Emmaus after rebates and coupons). All it takes is a couple less hospital visits and Endari pays for itself.

Okay, so the drug is effective. What’s the stock worth?

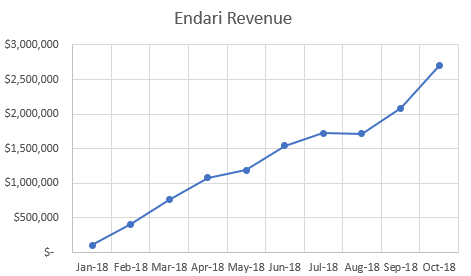

Well Emmaus just started their ramp with Endari in January. The CEO, Dr. Niihara, who is also the founder and inventor of the drug, gave us an indication of the sales ramp in a PiperJaffrey presentation they gave in November. This is gross revenue.

They also said there was about 1,200 patients on Endari at the time (so November). That roughly lines up with the gross ASP of $30,000/year.

Niihara also forecasted 10,000 patients on Endari by the end of 2019.

So the math on that is 10,000 patients at $20,000 net ASP is $200 million of annual revenue.

The math on the post merger valuation is that there will be about 160 million shares of Mynd Analytics outstanding. I bought the stock at $1.40 so that gave it a market cap of about $225 million. Now the market cap is around $280 million. I actually added a little at the open this morning after I wrote this up because it made more sense to me once I put it down on paper. Sometimes writing clarifies the mind.

Somehow under 2x revenue for a biotech with a new drug ramping and an orphan drug designation seems too low to me.

Endari is on patent in the US for another 6 years. There is a 10+2 patent in Europe that doesn’t begin until its approved. There is another patent in Japan.

The $200 million should be just a start. It’s basically a 10% market share in the US, but market share isn’t really the right term here because it can be used at the same time as its competition. Europe has a TAM of another $1.2 billion (the ASP is Europe is expected to be a bit lower). ROW TAM is another $3.4 billion.

So the TAM is reasonably big. It’s not like Endari is going to top out in a few months and stop growing its market.

Given that I think the stock isn’t pricing this in.

On the risk side, I have lot’s of questions. First, why is Emmaus doing this? They said they don’t need capital and its cheaper to merge than an IPO, which is fair. They also get the $60 million or so of net operating losses, so that’s a reason. But I have to think that after the lock-up (120 days) some of these early investors will want out.

Second is the risk that Endari falls flat. I have no reason to think that from what I’ve read, but the drug is an improvement, not a cure. I am also no biotech expert. There are also a bunch of drugs in the pipeline that are a few years from approval and will be competition.

Third, I’m not sure how far off that competition is. Both Global Blood Therapeutics and Novartis have recently received fast track designation for their drugs. It’s not completely clear to me what that means for approval.

Fourth, the spin-off of the psychiatric business is likely to get sold hard when it happens. Everyone now is buying for the interesting business and the not-so-interesting business is an afterthought.

Fifth, I don’t know much about Emmaus beyond what is on their website and what is in the disclosure documents.

Sixth, if the government shuts down again god knows when this will close. I’ve been waiting on Eclipse and Blue Ridge to close for like 8 months now.

Seventh, prior to the merger it seems like there was quite a bit of management deals on shares and related party transactions from the not-so-interesting businesses they operated.

There are others, but that’s a few to ponder.

Nevertheless it seem like a decent speculation at this price. And it let’s me write something up quickly and keep new years resolution #4.