Week 30: Cognitive Dissonance, Canaco updates, Canadian house prices and the story of Community Bankers Trust

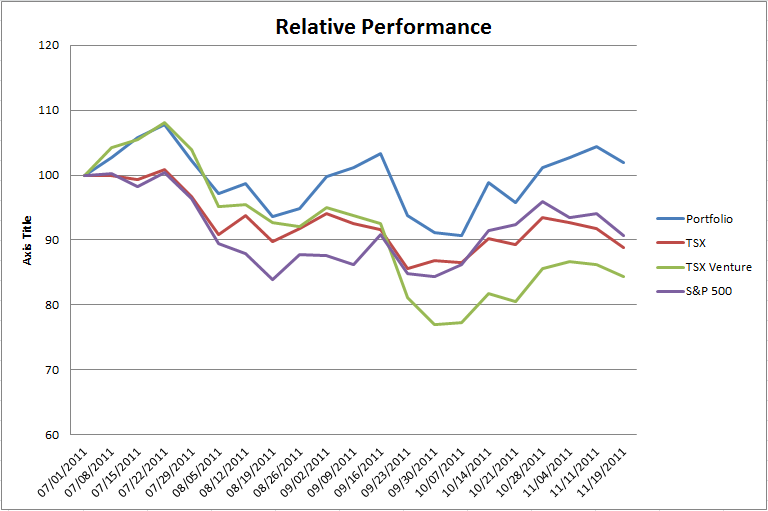

Portfolio Performance

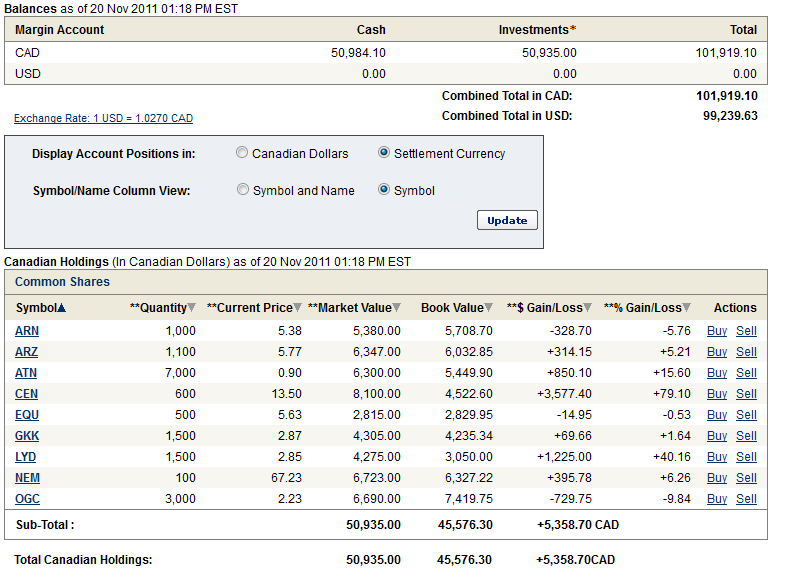

Portfolio Composition

Trying to not be dogmatic

A few years ago I read a book called Mistakes were Made. The book described our ability as human beings to remain convinced that we are right to the point where we ignore all evidence to the contrary.

Our predisposition to fabricate reasons why we are right and ignore reasons why we are wrong is based on a concept called cognitive dissonance. As the book defines it:

Cognitive dissonance is a state of tension that occurs whenever a person holds two cognitions (ideas, attitudes, beliefs, opinions) that are psychologically inconsistent… Dissonance produces mental discomfort ranging from minor pangs to deep anguish; people don’t rest easy until they find ways to reduce it.

All symptoms I am all too well acquainted with.

Along the same lines, I came across an interesting piece on FT this week. The following quote can be attributed to SocGen’s Dylan Grice:

But all is not lost. The bias towards thinking we’re more correct than we are isn’t driven by an inability to fully assimilate undesirable information but an unwillingness to do so. Therefore, the first step in removing the bias is to adopt procedures that foster a more honest acceptance of logical conclusions. Logic has no emotional content per se. There is no such thing as good or bad information; information is only true or false.

But because of our hardwiring, we only want certain information to be true. In particular, we want the information that confirms our prior beliefs and validates our belief systems to be true — about ourselves, about others, about the world. Thus, debiasing ourselves must involve an honest assessment of what we want: do we want to be right about everything, or do we want to know what’s true?

Let’s bring this back to what this blog is about: investing. In my piece last week I stepped through the basic premises on which I am currently invested. The tenants I stated were the conclusion of a somewhat anguished and certainly restless mental reevaluation that I had been running through over the prior few weeks.

As the market moved against me I started to look at why I might be wrong. In my spare time I tried to “assimilate the undesirable information” and paint the most contrary picture I could.

I especially went through the exercise with gold and with my rather significant precious metal stock positions (Aurizon Mines, Atna Resources, OceanaGold, Canaco Resources, Geologix, Esperenza Resources, Lydian International and Golden Minerals). Gold is always easy to question (what does gold really do anyways?). I attempted to soberly evaluate both the prospects of the metal and the companys. I looked for reasons to basically cut them loose.

I hemmed and hawed a lot, and at times began to convince myself that I was indeed wrong. But in the end I was led back to the basic points of valuation and underlying conditions, which seemed to me to remain firmly in gold’s favor.

This is how I make decisions. At times it undoubtably appears that I am flip-flopping. I am sure that my weekly writings must have an aire of contradiction when read one after another. A reader might wonder how it is that my point of view can go from one extreme to another in the matter of weeks (see Argonaut Gold). Or at times even flip 180 degrees only to flip back a few weeks later (see Argonaut Gold).

In truth, this is the only process I know of that allows me to really question whether I am right. If I can push myself to the edge, almost convince myself of the diametrically opposed point of view, and still in the end come back to my original conclusions, then well, that’s really getting somewhere. At times I push myself so far that I actually begin to believe it myself (ah yes, see Argonaut Gold), but that is just a occasionally necessary casualty. Far more often I leave the exercise with more clarity, and with that clarity comes the likelihood that I will act properly when the situation arises.

In the end I came away from my “anguished” analysis of gold more confident in my positions than I was when I started. And this week, on Wednesday, when the Fed news hit the wire that interest rates would be low for time eternity, that gave me the clarity to act.

The moment I read the news I bought a position in Barrick Gold, and I added to my positions in Esperanza Resources and Golden Minerals (though I neglected to make the AUM trade in my practice account). The next day I added to OceanaGold, and thta was followed by additions to Atna and Canaco the day after that.

In my practice account:

And in my actual account:

You do the work so that you have the confidence to act. You put in the time learning and working through why so that when an opportunity makes its brief appearance, when Bernanke comes out and says “yeah we aren’t going to raise rates for a long time” you can recognize it for what it is and say “all right, I’m in” and you know what you have to do.

Had I not been stepping through the thesis of why gold and gold stocks remain a solid investment, I likely would not have had the conviction to buy into the rally. At worst, I would have sold into the rally, because if you really don’t know why you are investing in something you tend to take the first blip after a long period of blah as a “finally I can get out” moment. As it is, with the Fed putting interest rates on hold for another couple years, and with their actions maybe even foreshadowing a true QE event in Europe, I feel quite confident that I am positioned well for that fall out.

Speaking of Canaco Resources…

I bought Canaco Resources at the end of the year at about $1.10 as part of my “tax loss buying binge”. A couple of things happened with Canaco this week.

First, the stock went up.

Second, the company updated us on its activities in Tanzania:

- Expect a resource estimate by the end of March

- Expect a preliminary economic assessment by the end of the third quarter

- Expect further metallurgical testing results at some point

Third, Canaccord Capital came up with an updated price target, and more importantly helped give us a glimpse at what to expect from the upcoming resource estimate (hat tip to howestreetbull who posted this on Investors Hub).

- Canaco has approved a US$35-40 million 2012 exploration budget, and is currently drilling 10,000 metres per month at Handeni with nine diamond drill rigs and one RC rig.

- Six of the drill rigs are focused on delineating the Magambazi resource in preparation for the initial resources estimate. Two diamond drill rigs are focused on the Kuta and the Magambazi North Extension targets. The remaining diamond drill rig is operating on the Majiri target, where previous surface sampling and RC drilling indicate a gold anomaly. The RC drill rig iscurrently operating on the Bahati target to test preliminary regional targets.

- We are expecting an initial resource and metallurgical test results in Q1/12, and a PEA in Q3/12. We are expecting an initial resource of 2.3 million ounces of gold at a grade of 3+ g/t gold. Previous metallurgical testing indicates recoveries of 90+% using a conventional CIL process.

Valuation: with US$110 million in cash, we believe the company is in a strong position to continue to derisk and advance the Handeni project. Our peak gold price estimate of NAVPS (10%, US$1,750/oz) remains unchanged at $7.50. We continue to value Canaco based on a 0.65x multiple to our peakgold price estimate of NAVPS.

At the current price of $1.50 Canaco trades at a market capitalization of $300M. Subtracting the current cash balance of $115M, the enterprise value of the company is a little less than $200M. If the deposit does indeed contain 2.3M oz of gold, the valuation being given for those ounces is about $80 per.

This is a 3 g/t open pittable deposit that looks to be 90% recoverable with a straightforward metallurgical process sheet. In my opinion (and apparently Canaccord’s as well) those ounces should be worth more than $60/oz.

To throw out a comparison point from a recent PEA, Prodigy Gold had a PEA done for its Magino gold property last March. The PEA assumed a CIL recovery process, a 9 year mine life, producing gold from an open pit at a grade of 1.2g/t for 9 years to give a total mine of life production of 1,585,000 oz of gold. The after tax NPV5 of the project was estimated at $259M at $1000/oz gold. That works out to a value of $160/oz.

Albeit there may be better comparisons out there, but this one surely suggests that Canaco is undervalued. Canaco’s Magambazi project is much higher grade than Prodigy’s (3g/t versus 1g/t). The location is Africa, versus Canada for Prodigy, which probably suggests a bit of a discount against Canaco but not enough to make me change my opinion. And while the Magambazi strip is as yest unknown, the Magambazi deposit appears to be around a hill top, which should lead to a reasonable number (the strip for Prodigy’s Magino is 3.3).

Finally, the last bit of news was that Brent Cook came out with the following plug about Canaco:

“The funds were just jumping in on this thing – and they all bailed out as well – the stock got down to $1.20. During this time period they’ve been drilling and drilling and drilling, and the results continue to show me that they’ve got what I think is going to be a legitimate, decent size, decent grade, open-pittable deposit in Tanzania,” Cook says. “So we’re buying this stock at $1.30 with $115 million in the bank, and a $41-million exploration program. That, to me, seems like a good buy.”

Yup.

When the gold price broke out on Wednesday, Canaco was the first stock I added to.

and speaking of gold…

I came across this interesting piece of information regarding the appetite of the Chinese for gold. This may be old news to some but I think it is still worth reporting.

The People’s Bank of China research director Zhang Jianhua was cited as saying Monday in the central bank publication Financial News that gold purchases should be ramped up when prices drop, although he gave no indication of what proportion of the nation’s $3.2 trillion forex reserve should be allocated to investments in gold.

Apparently, Jianhua called gold the only safe haven left and said that:

“the Chinese government needs to further optimize China’s foreign exchange asset portfolio and seek relatively low entry points to buy gold assets…no asset is safe now. The only choice to hedge risks is to hold hard currency – gold”.

High House Prices

I’ve been doing some research on house prices in Canada and in particular in my city, Calgary. I plan to do a separate post on my findings shortly, but for the moment I just want to throw up a couple teaser graphs that gave me pause for thought.

The chart is taken from a speech given by Mark Carney to a Vancouver audience last June. The methodology used is the ratio of the nationwide median home price to the median household disposable income. A ratio of greater than 3 has traditionally been seen as unaffordable.

It makes you think.

One other chart from the same report. Below is the average house price in Vancouver:

Its either a heck of a bull market or a bubble. To say it another way, I don’t know about house prices, but when a stock goes parabolic you typically know how it is going to end.

Anyways, more on this later.

Community Bankers Trust

It was a good week for Community Bankers Trust (BTC).

Earnings will come out for the company on Tuesday. Hopefully the company will put together another profitable quarter.

The BTC story

I bought BTC as a turnaround story. Community Bankers Trust is a bank that has been trying to reincarnate itself after the first incarnation came close to an early death. My observation is that they have been successfully navigating this resurrection, and with the recent turn in profitability (and a helpful turn in the economy) the bank is on its way to realizing its earnings potential.

The bank was hit hard by the recession in 2009. The company saw nonperforming loans skyrocket from 2% of total loans in the first quarter of 2009 to 10% of total loans in the second quarter of 2011. Yet there have been signs that the efforts the company has been making to turn itself around are working, culminating with a profitable quarter in Q3.

Let’s hope they can keep that momentum.

How did they get to here?

The original strategy of the bank was, as far as I can tell at least, to simply buy other banks and get bigger. Witness, the name of the original company was called Community Bankers Acquisition Corporation (CBAC), so they weren’t exactly being subtle. Along with the acquisition strategy, the bank seemed to have a “worry about the profitability later” strategy, which may have worked ok when the economy was growing but that fell flat when the economy didn’t in 2008.

As best as I can discern the acquisition effort was spearheaded by Gary Simanson. He headed up the original company CBAC, and then moved into a position of Strategic Vice President, a position I don’t think I’ve ever heard of with any other company. According to this article, Simanson was responsible for subsequent acquisitions.

In truth, the timing was what killed the acquisition strategy. To quickly step through the timeline, in May 2008 the company began its journey by acquiring two local Virginia banks, TransCommunity Financial Corporation, , and BOE Financial Services of Virginia, Inc. In November the bank moved ahead and acquired The Community Bank, which was a little bank in Georgia. Finally in January 2009 they acquired Suburban Federal Savings Bank, Crofton, Maryland.

So you had 4 bank acquisitions in less than a year happening at the time of a 100 year financial tsunami. How do you think things turned out?

Change in Direction

By 2010 Simanson had left the company and the direction of the company was changed to the more pragmatic “we need to get profitable before we go belly up” strategy.

This was described pretty bluntly in the 2010 second quarter report. CEO Gary Longest said at the time:

Our strategy has shifted from that of an aggressive acquisition platform, to one that meets the banking needs of the communities we serve, while providing sustainable returns to our stockholders. To this end, we are taking the necessary steps to return immediately to profitability. We are actively analyzing our market base to assess the contributions of all branches to our franchise value and will take the appropriate actions in the third quarter of this year. Additionally, we will make aggressive expense reductions, and will look to restructure and strengthen the balance sheet. We are confident that the analysis of these potential critical paths and the resulting execution of these initiatives will lead us back to profitability quickly.” “Our goal is an immediate return to consistent quarterly profits. To accomplish this, we have no alternative as a Company but to make clear and intelligent decisions in the next 60 days, no matter how difficult, to accomplish that goal as soon as possible. That is our full focus.”

In a somewhat odd twist to which I’m sure there is a good story, Longest himself was gone only a couple months later. Nevertheless the interim CEO and soon to be permanent CEO Rex L. Smith took up the reins and has carried out the strategy quite well given the circumstances.

Where are they now?

I already mentioned that the company had its first profitable quarter in a long time last quarter. I don’t believe this was a one time fluke. It looks to me like its the culmination of a number of initiatives put forward by the bank that have been geared towards making the bank more profitable.

The company has made an effort to lower the cost of its deposit base. Time deposits, which are expensive high interest bearing deposits, have decreased from 73% to 67% of total deposits since the end of 2009. As well, the cost of the time deposits has come down from 2.9% in 2009 to 1.6% in the third quarter.

The effect has been a steadily rising net interest margin (NIM) since the strategic direction change in 2010.

(note that this graph is a simplified version of NIM calculated as a percentage of all assets rather than the more common formulation of interest bearing assets)

(note that this graph is a simplified version of NIM calculated as a percentage of all assets rather than the more common formulation of interest bearing assets)

The company also undertook efforts to reduce expenses. The most common way of illustrating the day to day expenses of a bank is through something called the Efficiency ratio. The Efficiency ratio is simply the ratio of the total non-interest expenses at the bank (so the salaries, building costs, lawyer fees, pretty much everything except the actual cost of borrowing money) to the net interest margin (so the amount of interest made minus the amount of interest paid). The reason that you look at the Efficiency ratio is because it ex’s out growth, since growth should occur for both NIM and expenses in concert with one another.

The Effiency ratio of BTC has been falling consistently.

What’s it worth?

To get an idea of what the bank might be worth if it continues to pull itself together, I put together a proforma earnings estimate. I stripped out all the provision for loan losses, the FDIC intangibles (from their earlier acquisitions) that the bank is required to amortize, as well as losses on real estate and gains of the sale of securities. So basically I looked at the banking skeleton that is BTC. Here is what I found:

What this clearly demonstrates is that if get rid of all the scabs, there is quite a profitable little enterprise here.

Meanwhile, the bank sports a tangible book value that is much greater than the current share price ($1.40 after last weeks run up):

What is left to be done?

The story that still needs to play itself out is the healing process. The really big negative for the bank is that it still has an extremely elevated portfolio of non-performing loans. There are signs that this is abating, and in truth part of the bet here is the same one that you make on any regional bank: the US economy is turning the corner, the Fed is not going to allow it to fall into another recession, and so the worst of the loan defaults are behind us.

But just to get an idea of the risk here, typically you wouldn’t want a bank to have non-performing loans in excess of a couple of percent. Many of the best banks I’ve looked at have nonperforming loans of well less than 1%. BTC, onthe other hand…

There are tentative signs that the peak has passed, but it will take a few quarters before we know for sure that further write-downs are not coming.

Earnings on Tuesday will give us a lot of insight into the direction of the trends. I’ll be looking closely at nonperforming assets and the 30-89 day deliquents (which are an early warning of the soon-to-be not performing. I also will be hoping to see some decent earnings.