Arcan Resources: Thoughts on the Waterflood at Ethel

Arcan’s Q2 MD&A, which was released August 29th, was somewhat short on detail. Unlike the past, the company neglected to provide much detail about their quarterly production. Previous MD&A’s broke out production on a well by well basis, which helped to give some insight into where Arcan’s production has been coming from and what problems, if any, might lie ahead. Nothing of the sort this time. Its been suggested that this was Crescent Point’s influence. Could be, the timing certainly coincides.

Nevertheless the MD&A did provide one nugget that was perhaps overlooked by the market but is nevertheless important. Waterflood approval from the ERCB, which had been expected early in 2012, was given early.

In August Arcan received approval for water injection in the Ethel area. Wells are currently being converted to water injectors and water handling facilities are currently being constructed in order to commence water injection.

This is terrific news for the company. Waterflood should be having an effect by sometime late in Q4 or early in Q1.

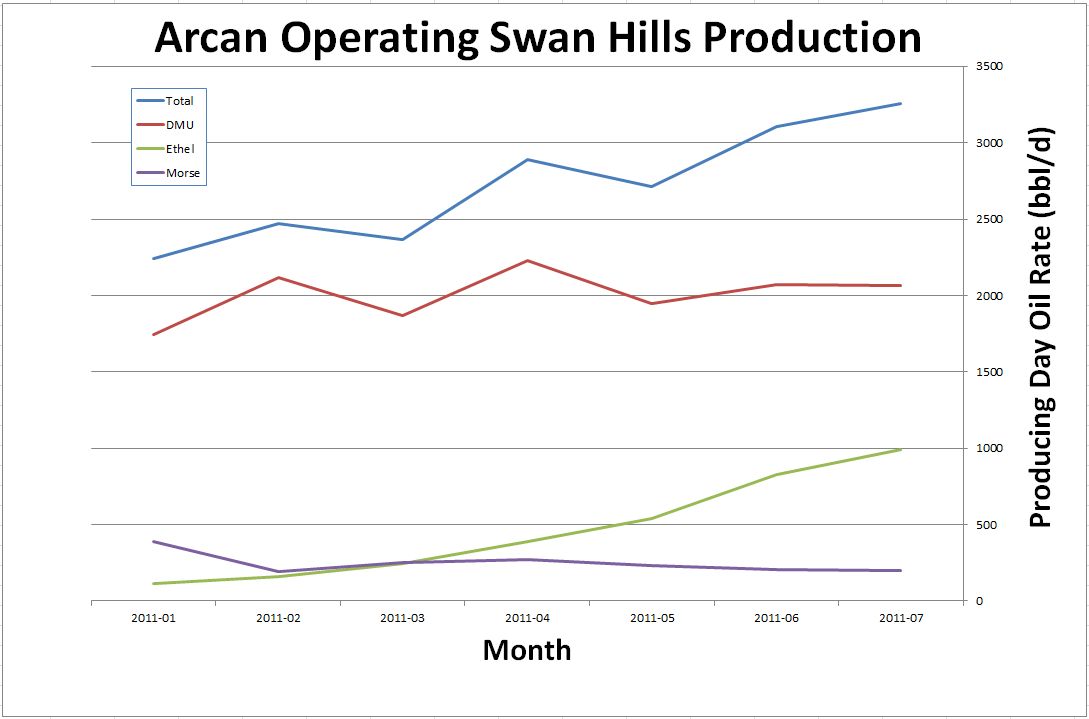

The news of the waterflood at Ethel made me want to dig a bit further into Arcan’s prodution. I decided to investigate how much production was coming from Ethel, and what kinds of declines that unit was currently experiencing.

Below is a graph I made of Arcan production by unit (data available is to and including July 2011). Note that I have not taken into account working interests and so the numbers are gross. There are also a few wells that appear to me to fall outside the units (meaning the extents of waterflood) so I didn’t include those. The production data is in calendar day rates.

Ethel is where Arcan has been focusing their resources of late and that is where the overall production increase is coming from. At Ethel Arcan brought on-stream a well in April, a well in May, two wells in June and there are 2 wells tied in that should have been producing in August (15-08 and 06-10). Meanwhile, DMU (Deer Mountain Unit) has been surprisingly flat given that they’ve only added on-stream a couple wells since the first quarter of this year. Morse River is mostly vertical wells that have been producing for years, so its profile is basically flat.

Next I took a closer look at well performance at Ethel. If you look at the average Ethel and DMU production curve, you can see the effect of the waterflood taking place at DMU versus Ethel. Ethel wells do appear to stabilize at a lower level. The following chart looks strictly at horizontal Ethel and DMU wells drilled after Jan 1st 2010 (I didn’t want to confuse things by adding data from old completions) averaging out the monthly production for all wells at that point in their decline. Producing day rates are used.

Now it has to be pointed out that the post 6 month data for Ethel is a single well (the 10-27). So we are not dealing with a large dataset here. Still, I think the conclusion can be made that Ethel wells drop off quicker and stabilieze at a lower rate without the waterflood.

Presumably with waterflood one would expect that Ethel type curve would shift up to where the DMU curve is. One mitigating factor to this improvement might be reservoir quality. The sands at Swan Hills have often been thought to thin to the south. On the other hand, Arcan’s completion techniques have improved quite dramatically lately with the move to the larger acid fracs (another detail that was provided in the Q2 MD&A). This is witnessed by the significantly higher IP30 and IP60 results produced by these presumably thinner sands at Ethel. So this may help the Ethel wells outperform.

Its a bit of a guessing game until you get some data.

So what does it mean to production? Two things. First, with the waterflood implemented you would expect that the existing wells at Ethel would deliver a higher rate. I’m going to speculate that, on average, this would be about 40bbl/d for the post 2009 drills. This would add about 350bbl/d of production to Arcan.

A bigger effect will occur going forward. Those wells put on-stream in June and July and those wells being drilled right now and through to the end of the year should see a shallower decline and more stable production profile after the first few months.

Arcan Resources was, for a time, my largest holding. Arcan announced a large bought deal yesterday just before market close. As you would expect, the stock did poorly today, trading down to the price of the deal.

After watching the stock fall on account of the bought deal, and doing some thinking about Ethel and the upcoming waterflood, I decided to buy a bit more Arcan yesterday.

When you look at the bought deal, they were able to raise a significant amount of money in what is a difficultenviornment. As well, $85M of the $135M deal was in debentures. This is good from the perspective of dilution; the debentures are convertible at $8.75.

Jennings put out a piece yesterday suggesting Arcan had the cash to be drilling 6 wells a month. I don’t know if that will be the case, but if it is, 6 wells drilled into three areas now under waterflood should produce some impressive production gains. I remain of the opinion this is one stock worth holding through the unfolding European implosion.

{kind=link}