A Positive Step for Equal Energy

In a week that was littered with strong stock performance, one of the best stocks in my current ownership lot was Equal Energy. Most of the outperformance came after the company released news that they were disposing of non-core assets.

Equal Energy Ltd. (“Equal” or the “Company”) (TSX: EQU): (NYSE: EQU) announces that it has entered into definitive agreements to sell several non-core properties in Canada for a total cash consideration of $49.35 million (the “Asset Dispositions”). The proceeds from the Asset Dispositions will be used to reduce outstanding debt.

Don Klapko, President and CEO commented, “ Equal will continue to develop its key oil plays in the Alliance Viking and Lochend Cardium in Canada, and its liquids-rich gas play in the Hunton formation of Oklahoma.”

The Asset Dispositions include properties in Alberta, Saskatchewan and British Columbia and compromise total current production of about 2,100 boe/day, of which 51% is natural gas. Upon closure of the transactions, Equal expects to realize lower operating costs and interest expense resulting in improved cash netbacks per unit of production on the remainder of its assets. Equal estimates that its net asset value will be approximately the same after the completion of the Asset Dispositions. The Company anticipates its second half 2011 production to range between 9,200 – 9,700 boe/day, after taking into consideration the Asset Dispositions.

By taking a look at the last Annual Information Form released by the company (March 24th) its pretty clear that Equal sold off all its land outside of the 3 core areas of the Alliance Viking, Lochend Cardium in Canada, and the Hunton formation of Oklahoma. Below is a list of other properties owned by Equal and producing totals for each area. Together these properties add up to about 2,000boe/d.

So what are these properties? Below I’ve copied the description of each from the AIF:

- The Desan property is located 120 kilometres northeast of Fort Nelson, British Columbia in the gas producing greater Sierra area. The primary producing zone is the Jean Marie formation.Daily average production in Desan for December 2010 was 2.6 mmcf/d of natural gas and 16 bbl/d of oil and NGLs.

- The Clair property is located 20 kilometres north of Grande Prairie. The Corporation’s assets include a 100% working interest in 4,380 acres of land (1,340 net undeveloped acres), 15 producing wells, 6 water injection wells, and a profit sharing interest in an oil blending facility. Oil and natural gas production is primarily from the Doe Creek (Dunvegan) formation. The Doe Creek oil pool produces light (41 API) oil along with solution gas and is currently under water flood to maximize oil recovery. There is also natural gas production from one Charlie Lake well. Average working interest production for December 2010 was 227 bbl/d of oil and 379 mcf/d of natural gas.

- The primary production is crude oil (27 API) from the Pekisko formation. Much of the Corporation’s land is covered by 3D seismic with detailed geological and geophysical studies outlining new development drilling opportunities. Additionally, significant potential lies in the Bow Island and Sunburst formations. During 2010, Equal drilled two wells in the Princess area. At year-end, the Corporation had 25 producing wells in the Princess area with average working interest production of 303 bbl/d of crude oil and NGL and 817 mcf/d of natural gas. Net undeveloped acreage totalled 1,237 acres at year-end.

- The Primate heavy oil field is the main producing asset in the Primate area and the Corporation holds a 100% working interest in this property. Oil and natural gas production comes primarily from the McLaren and Mannville formations respectively. Despite the oil’s gravity, 11 API, the gas saturation of the reservoir allows cold production of the oil under a primary recovery scheme.Average December 2010 production from the Primate area was 387 bbls/day of crude oil and 925 mcf/d of natural gas.

- Natural gas production from the Liebenthal area comes from the Viking formation. The Corporation holds a 100% working interest in the pool. Seismic indicates that the pool is structurally controlled. Average December 2010 production from the Liebenthal area was 1,028 mcf/d of natural gas.

None of these properties strikes me as terribly interesting and the undeveloped land appears to be negligable.

Reduction of Debt is a Good Thing

The reason that this is such a good move for Equal is not because they scored a killing on the price. They didn’t. They received about $25,000/boe producing on the transaction. This could be considered a bit low, but given the following facts, its not bad:

- The amount (51%) of natural gas involved

- The oil produced at Primate is 11 API

- the oil produced at Pekisko is 27API and presumably requires a lot of water handling

- There is almost no undeveloped land involved in the deal

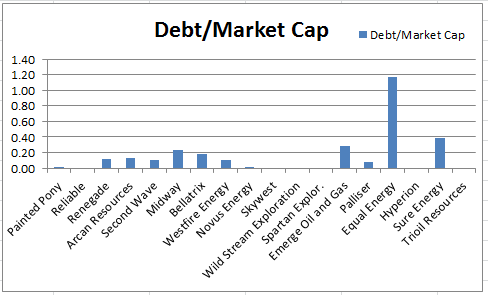

The reason this is such a good move for the company is because it de-leverages them. I think that the amount of leverage that Equal has is the primary reason that the company is trading so cheaply. When you look at Equal’s debt compared to its production level, and compare that to the other juniors I follow in my universe its rather clear that Equal is quite leveraged up.

After this transaction Equal’s ratio drops to 16,300, which puts them more in line with their peers.

Onto the Mississippian!

The second positive that comes out of this transaction is that it should help to speed up the development of the Mississippian. I was clearly too early when I bought Equal in the spring on the expectation they would begin exploiting their Mississippian prospects in Oklahoma soon. But while the company has yet to spud a well or provide a firm development plan for the Mississippian, it is clearly on their radar. Again from the news release:

Equal has amassed a significant acreage position on an exciting new Mississippian light oil play in Oklahoma that exists on acreage held by production from certain of its Hunton fields. The Company plans to continue consolidating acreage prospective for the Mississippian while it considers options to begin development of the play during 2012.

It remains a waiting game. Having held it this long, I will continue to hold Equal until these Mississippian wells begin to be drilled and the company hopefully gets revalued to a more reasonable level in anticipation.

{kind=link}

I just would like to make a correction, the company still owns the Claire oil field and the Liebenthal formation (however this formation is shut in right now).

Regards,

Nawar