The Canadian House Price Plateau (or cliff?)

I live in Calgary, Alberta. The house prices here are high by most global standards. The average sales price of a single family home in Calgary was $453,000 in December.

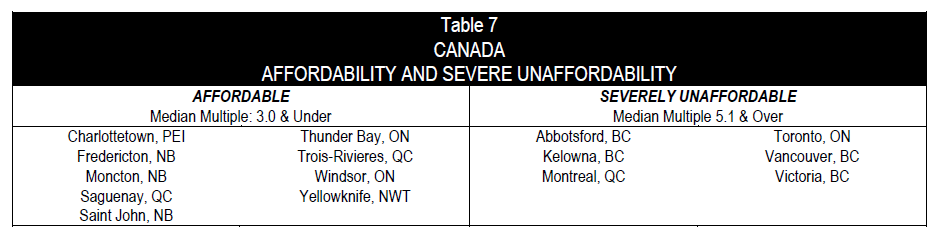

In Canada, Calgary is nothing special. House prices in Canada are high. I stumbled upon the following interesting research by the Demographia International Housing (DIH) that compared house prices across the globe. Here is what they determined as being the unaffordable locales in Canada.

For those of you unfamiliar with Canada, Fredricton, Thunder Bay and Yellowknife do not represent a “hub” of Canadian population. Vancouver, Victoria, Toronto and Montreal do.

The above was taken from the DIH’s Affordability Survey (2012). The methodology they use is to rank cities based on affordability is to use a ratio of the median home price in the city divided by the household disposable income. The number gives a ratio, and a ratio of greater than 3 has traditionally been seen as creeping into the unaffordable category.

Whne I read through the report, my first question was, what exactly is household disposable income (HDI)? From wikivest:

The amount of money that households have available for spending and saving after income taxes have been accounted for. Disposable personal income is often monitored as one of the many key economic indicators used to gauge the overall state of the economy.

In Canada, HDI is somewhere around $55-$65K depending on the source you use to calculate it:

While the DIH provided some interesting city by city numbers, I was able to dig up a Canada-wide number from a recent speech given by Mark Carney. You have probably read sound bites from this speech before. In particular the following shocking, over the top, end of the world type pronouncement about the Canadian housing market has been quoted widely:

Some excesses may exist in certain areas and market segments.

These central bankers are fear mongerers!

But not to worry, Carney also pointed out that overall the Canadian housing market is healthy:

Canada’s housing supply is relatively flexible, compared with other countries, and it appears to have grown at rates broadly consistent with underlying demand forces, the most important of which is the rate of household formation.

Of course, in the United States, in the time leading up to their housing collapse, Alan Greenspan and then Ben Bernanke said much the same thing. One thing I have learned from reading all these books about the 2008 housing debacle in the US is that what a central banker says has more to do with the central bankers ideology is than the on the ground reality.

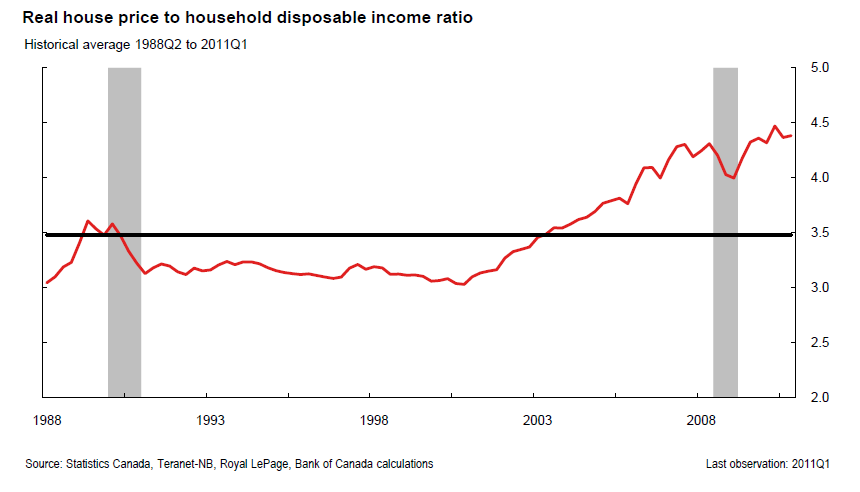

If you look at the data, you get a somewhat more worrying picture. Below is canadian house prices to disposable income:

Overall the country is quickly approaching 4.5. Using the DIH methodology, this would put the country as a whole in the “seriously unaffordable” category.

Overall the country is quickly approaching 4.5. Using the DIH methodology, this would put the country as a whole in the “seriously unaffordable” category.

As for Calgary, with a ratio of 3.9, it is only “moderately unaffordable” (phew), though we are on the cusp of being “seriously unaffordable” (uh-oh). There is a really excellent analysis of how both house prices and household income have grown on the economic analyst website. They posted the following comparison for Calgary in particular:

One more point about Calgary. If you look at the median house price that is being used for Calgary by the DIH and others, you would be struck by the fact that it is $353,700 and not $393,000, which is median price reported by the CREB. The reason for the discrepancy is that the $353,700 number includes the “surrounding district” which means it includes Cochrane, Airdrie and some of the farming communities surrounding the city (Acme?). If you include the metro Calgary area only, which is what the local real estate board does when they are reporting statistics (because they like to print higher numbers), it would put Calgary into the “seriously unaffordable” category. I cannot find data on the area used to calculate the average household disposable income of the city, but I imagine it would be based on tax receipts and thus be restricted to the metro area.

Back to Canada as a whole, price to rents tells the same basic story.

Its either a heck of a bull market or a bubble.

As an aside I was amazed to learn that the price to disposable income in Vancouver is a rather bizarre 10.6. And that is using a $678,000 median. If you start using the average home price in Vancouver, the ratio is closer to 15.

Of course none of this has to end until interest rates show some sign of rising. Right now our househols pays prime -0.9% on our mortgage. That works out to about a 2% interest rate. Its rather insane. Even if we had a $500K mortgage (we don’t) it still be affordable. Of course if that rate went to 6%, it would be a different story. Some day that might happen.

Opportunities?

So why am I writing about this? Well for one, I think its an interesting study. The Canadian housing market has defied all other housing markets that have crashed and burned in the last few years. It has also defied most all metrics of affordability. For all the bears out there that say that the US housing collapse was inevitable it seems a reasonable question to ask: “then why not Canada too?”

I am of the mind that these forever rising prices, particularly Vancouver and Victoria and the inner city area of Toronto, are going to end badly some day. Everywhere else in the world the 3:1 ratio holds but Canada is different? The different argument is a big circular one. Because the different argument inevitably comes down to the fact that Canadians are inherently prudent and would not expose themselves to large risks. Which apparently means that this attitude allows Canadians to take on large risks. Anyways…

I also bring the topic up as a potential area for short candidates. Who would be hurt by a price fall? Particularly Vancouver.

Well first and most obvious is the Canadian banks. Mortgage debt makes up around 42% of the loans on the balance sheets of Canadian banks. This number has increased from 31% in 2002.

Another name that comes to mind is Home Capital Group. The company is always being praised on BNN by some expert making a top pick. The stock appears to trade relatively cheaply, at less than 10x earnings. But the business of the company is to make loans to people that can’t qualify for CMHC loans. I don’t know if the loans they make are “subprime loans” persay, they probably aren’t, but the company fills the exact same niche that the subprime borrowers in the US did.

I don’t know enough about the company to make any more observations than that right now. But it intrigues me. The company is worth a closer inspection.

And I’m open to ideas. What other companies could potentially be left with their pants down in the event of a material decline in Canadian house prices? I think there is plenty of time to gather more information about this trade. There probably is not much to worry about until interest rates begin to rise. And that might not happen for another couple of years. Please contact me with any suggestions, either by email or in the comments.

I have not investigated Home Capital Group recently and last time I did was close to ten years ago and their stock did phenomenally. I forget the price but it was something like $8 to $25 in a relatively short time frame. Anyways, at that time they did not make “subprime loans” but loans to “qualified” people whose income might not qualify at a traditional bank. Primarily, this group consists of small business owners or self-employed incomes and did not reflect on poor credit history or anything like that. Also at that time they began to initiate a new segment involving securitization of mortgages and was their fastest growing segment. I have no idea what occurred post 2008. But they deal with Canadian real estate and it has simply not tanked like USA. If the Canadian real estate market collapsed with a 50+% decline then I assume their business would also suffer like Canadian banks too.

I think the logical target sectors that would get hit hard from a Canadian real estate melt down would be sectors such as lumber companies, home improvement stores like Rona, new home building companies, and realtor agencies.