Can’t stay away: Arcan Resources and Second Wave Petroleum

If you remember, I sold both Arcan and Second Wave a week ago Friday. That lasted about a day and a half.

Sometimes selling a stock can make you think about it more clearly. Such was the case with both Arcan and Second Wave. In fact I spent last weekend working through their prospects. I hope to post on this soon, but for now, let me just say that the work reiterated to me just how much potential these two companies have.

The main reason for not owning both of these Beaverhill Lake producers is because they are spending a lot more then they are taking in.

They really have been spending a lot more than they take in. The original reason I reduced my position in both companies last fall was because with Europe appearing on the precipice, being invested in companies in need of capital seemed like a poor proposition.

However Europe seems to be back on the back burner. For Arcan and Second Wave, spending a bit more then you make is not such a bad thing anymore. It can actually be perceived as a good thing; growth and potential and all that jive.

The reality is that the prize at Swan Hills continues to prove itself up, and the NAV of both companies will likely continue to rise as they drill more wells.

Perhaps the kicker for me was the news release put out by Second Wave last Monday. In the release SCS announced a number of new boomer wells in and around the existing boomer wells that they (with the JV with Crescent Point) and Coral Hills have been drilling. But more importantly, SCS announced the success of a well drilled far to the south of this existing “sweet spot”:

[Second Wave] completed its 100% working interest 01-17-062-10W5 Beaverhill Lake light oil well in south Judy Creek with an initial two day flow test rate estimated at 800 bbl/d of light oil further delineating the Company’s south Judy Creek land base.

The 01-17 well (big red circle) is well to the south of the existing sweet spot and it opens up a whole mess of land in between. A lot of those southern sections are 100% interest for SCS as well:

While we are somewhat away from proving up the sections in between, the 800boe/d success gives me a lot of confidence that they will be proved up over time.

I ran the cash flow numbers on 2012 based on their expected average production of 3,850 boe/d and $95 oil and I figure they can generate around the $85M mark of cash flow. I will post that cash flow analyis more thoroughly in a later post. For now, suffice to say that my estimate compares favorably to the $85M CAPEX estimate that the company had in their February presentation. Perhaps the days of spending in excess of what you make are soon to be over for Second Wave?

Future Catalysts?

I see a couple of catalysts for Arcan and Second Wave that made me want to stay out of the stocks.

I think that the biggest catalyst to get me back into both stocks in short order was the spector of the upcoming reserve report of both companies. I suspect that the reserves for both Arcan and Second Wave are going to show some excellent numbers, potentially with NPV10 estimates decently above the current share prices.

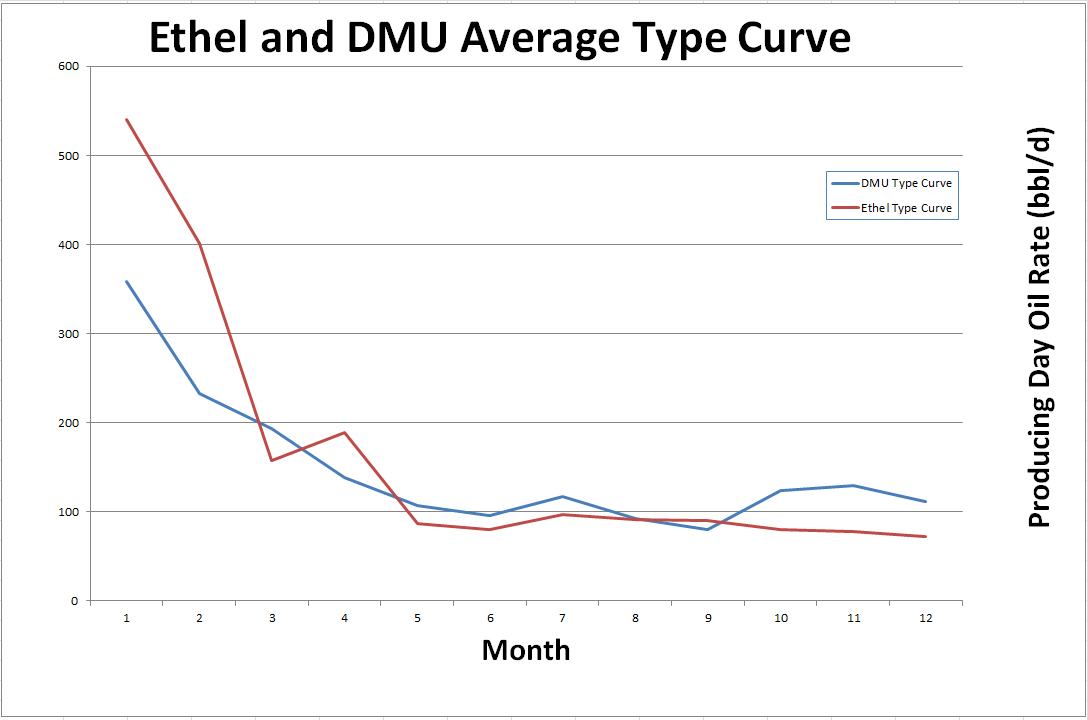

Arcan has the additional catalyst of the waterflood of Ethel. I posted late last year how quickly Ethel production was declining without waterflood. I wrote:

If you look at the average Ethel and DMU production curve, you can see the effect of the waterflood taking place at DMU versus Ethel. Ethel wells do appear to stabilize at a lower level. The following chart looks strictly at horizontal Ethel and DMU wells drilled after Jan 1st 2010 (I didn’t want to confuse things by adding data from old completions) averaging out the monthly production for all wells at that point in their decline. Producing day rates are used.

Now it has to be pointed out that the post 6 month data for Ethel is a single well (the 10-27). So we are not dealing with a large dataset here. Still, I think the conclusion can be made that Ethel wells drop off quicker and stabilieze at a lower rate without the waterflood.

Presumably with waterflood one would expect that Ethel type curve would shift up to where the DMU curve is. One mitigating factor to this improvement might be reservoir quality. The sands at Swan Hills have often been thought to thin to the south. On the other hand, Arcan’s completion techniques have improved quite dramatically lately with the move to the larger acid fracs (another detail that was provided in the Q2 MD&A). This is witnessed by the significantly higher IP30 and IP60 results produced by these presumably thinner sands at Ethel. So this may help the Ethel wells outperform.

Its a bit of a guessing game until you get some data.

So what does it mean to production? Two things. First, with the waterflood implemented you would expect that the existing wells at Ethel would deliver a higher rate. I’m going to speculate that, on average, this would be about 40bbl/d for the post 2009 drills. This would add about 350bbl/d of production to Arcan.

Since that time Arcan has drilled a number of additional wells at Ethel. I would estimate that once in full operation, if the 40 bbl/d per well increase number holds up one could expect around 500 bbl/d extra production from Ethel. But it could be more, and at least in the short run, likely will be more.