Week 55 Update: The Insurers

The Insurers

I added to all 3 of my insurers in the last two weeks; Radian Group, MGIC, and MBIA. Regarding Radian and MGIC, while the data this week was mixed, I still am of the mind that the worst of housing is behind us. While I’m not ready to jump into home builders or lumber stocks or anything else that is dependent on a robust recovery in prices or demand, I am willing to make a bet on mortgage insurance companies that need things to just stop getting worse. The insurers need prices to stop falling and defaults to continue to slow. I am inclined (albeit skittishly) to believe that will happen.

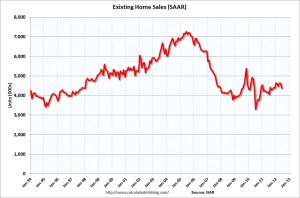

The housing data this week, while not great, supported that thesis. The market focused on the month over month decline in existing home sales (down 5.4%), but year over year the trend is still to higher sales (4.5%). The trend, while not robustly bullish, appears to be of a bottoming nature.

Perhaps more importantly, inventory continues to decline and the year over year number is down a somewhat startling 24.4%.

Total housing inventory at the end June fell another 3.2 percent to 2.39 million existing homes available for sale, which represents a 6.6-month supply4 at the current sales pace, up from a 6.4-month supply in May. Listed inventory is 24.4 percent below a year ago when there was a 9.1-month supply.

Bill Mcbride (of CalculatedRisk) pointed out in a recent post that it is really the inventory number that we should be focusing on:

I can’t emphasize enough – what matters the most in the NAR’s existing home sales report is inventory; what matters the most in the new home sales report next week is sales. It is active inventory that impacts prices (although the “shadow” inventory will keep prices from rising). Those looking at the number of existing home sales for a recovery in housing are looking at the wrong number. For existing home sales, look at inventory first.

Meanwhile the monoline insurers (Radian and MGIC) are writing more new business and this is some of the best business they have every written. I have already written about how strong lending standards are these days. Below is the trend for New Insurance Written (NIW) for the first 7 months of this year.

The returns on the new business should be quite impressive. Mark Devries, the analyst from Barclays that covers the insurers, was quoted in this Bloomberg article on expected returns:

Firms that stay in the business may benefit from a return on equity above 20 percent on new coverage as the exit of some rivals allows remaining insurers to boost prices, and tighter underwriting standards limit claims.

Meanwhile the old book continues to wind down. The delinquency bucket for both insures continue to fall.

The insurers are like those movies you see where there is a big explosion and the movie star starts running and there is this big fire ball behind them and its gaining on them but the movie star keeps running and eventually the big fireball burns itself out. These insurers are trying to outrun their legacy business by printing as much new business as they can to overcome the losses on the legacy. I think when they hit that point that new gains outrun old losses is when they really move.

As for MBIA, the company is less dependent on any specific economic dynamic then they are on the outcome of their court cases with Bank of America. There are signs these cases could be coming to a head, but of course they might not. Its really difficult to say when this will end and whether a settlement will be reached before a verdict. When I tried to analyze the deal between Bank of America and Syncora earlier this week and the conclusion I came to was that you couldn’t extrapolate much of anything to MBIA.

I don’t know how the businesses have changed since 2007, but have you read Ackman’s presentations on the bond insurers?

It strikes me that these are fundamentally unsound business models barring government involvement — “picking up pennies in front of a steamroller” so to speak.

Would be interested in hearing your reaction after reading these.

http://www.confidencegame.net/read-reportspresentations.html

(skip the Farmer Mac docs)

Thanks for pointing me to these slides. They will be a great resource. I bought Ackman’s book confidence game and plan to read it once I finish Fatal Risk, which is a book about AIG.

Whether the insurance business is a great business or a bad business depends on the price the business is written at. i haven’t gone through all the slides yet but I think one of the key ones is slide 14 of the How to Save the Bond Insurers presentation. That slide shows how MBIA and Ambac were writing business with margins of 20 basis points. Compare that to what Radian and MGIC are writing now. Its 60 basis point busines on plain vanilla residential loans. It isn’t an apples to apples comparison because Ackman is highlighting the structured finance wing of MBIA, which was writing business on CDO’s and CMBS and other structured products, whereas like I said pretty much all of what Radian and MGIC are writing now is flow insurance on individual first lien residential loans.

The other point that I will try to make quickly, and what I want to do a write-up on shortly, is how good that residential business is that they are now writing. They are writing business on loans with FICO score above 750, its being written at a time when only the lowest credit risks get loans. And when you look at Radian’s defaults since 2008, so the 2009 and 2010 books, they are way below trend on the loss charts.

The unknown for me with the monolines, so with Radian and MGIC, and what has kept me from writing them up in more detail, is understanding whether they are adequately reserved for the legacy book. They have to be able to get through that book. And its like Ackman is implying, these insurers wrote a lot of crap back in 2005-2007. They have to be able to weather that storm and come out the other end to see the benefit of new business they are writing. I think that Radian can do that, but like I said the real unknown is whether their reserves are going to cover the eventual losses. I struggle with understanding that. If I knew that Radian was adequately reserved I would be absolutely loading up the truck, because the company is going to earn a dollar plus earnings in a couple of years if they can get through the next couple. Its definitely got the potential to be a multi-bagger. MGIC I’m no so sure of, but the same dynamics are at play.

Again, thanks for the link to the slides.

Yeah, based on what you said, it sounds like they’ve been forced to really adjust their business models since 2008 (for obvious reasons).

Take a good read through the 2003 memo especially, because it’s got a lot of good information on assessing the quality of the old book of business.

I haven’t spent a ton of time on these other than reading the memos & Confidence Game, but even taking 60bps (vs. 20) but still being levered 140:1 is a bit scary. Not to say it can’t work… investors buying Fannie / Freddie in 1980 did QUITE well for themselves until 2006.

Anyway, look forward to reading your thoughts.