Valuing Tricon Capital’s Asset under Management Biz

As I’ve tweeted about, early in the new year I took a position in Tricon Capital (TCN.to) after being introduced to the company by a friend in early December. It took me until January to become comfortable with the name and until now to write about it. I’m slow.

I have found Tricon complicated to analyze; they have both an asset management business with a number of separate investment vehicles in addition to an on-balance sheet housing portfolio (which is my primary focus). They are also opaque; like most Asset under Management (AUM) companies the details about the investments held within the vehicles is scattered and incomplete.

The part of Tricon that I am most interested in is its home purchase business. Tricon has been buying properties across the US since Q2. Their purchases have been concentrated in Sacramento, Bay Area, Southern California, Phoenix, Charlotte, and SE Florida. They are looking to expand into LA county (where they recently signed a contract with a management company that would look for an purchase homes in the area), and potentially Orlando.

Right now Tricon has 1,500 homes on their balance sheet.

The part of Tricon I am going to focus on here is the asset management business. Before I can begin to value the residential home purchases I need to be able to isolate it, and to do that I have to eliminate the value of their asset management.

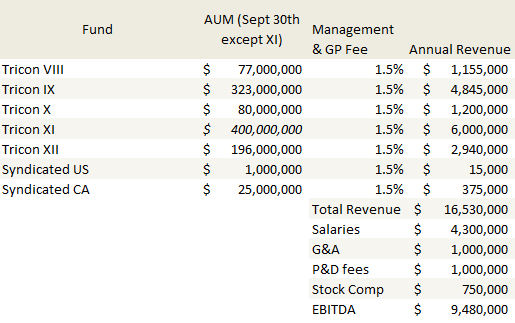

Valuing Base Fees

Tricon gets two base fees that are independent of incentives: a management fee and a general partner fee. Both fees are based on assets under management, together these two fees add up to around 1.5% (they were a little over that in the last quarter). Below I have tabulated all the assets under management that were collecting fees at the end of Q3 and from them calculated an EBITDA estimate based on Q3 salaries, G&A, professional and director and stock based compensation fees. Note that I am using Tricon’s estimate of eventual assets under management when fully subscribed for Tricon XI.

Valuing Incentive Fees

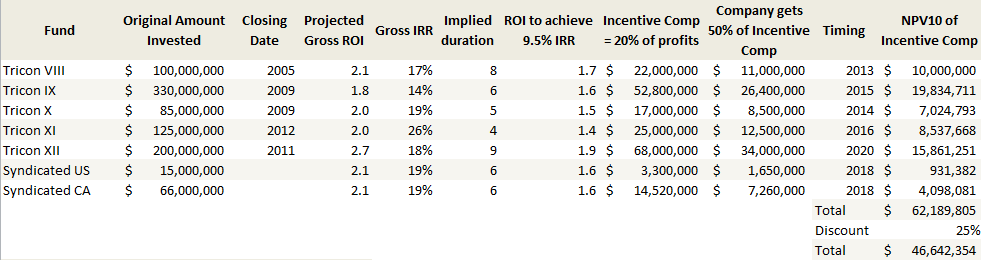

In addition to the base management fee, Tricon receives an incentive fee if their fund is successful . Because of the nature of the funds Tricon manages (they are real estate development private equity funds), the incentive fee is a bit complicated. It goes something like this:

- Tricon pays out the principle to all the limited partners in the fund

- Tricon has to pay out a minimum return to all limited partners, typically a 9-10% return on invested capital

- After that there is a catch up phase where Tricon gets 50% of the profits until they are at an 20/80 profit ratio with the limited partners

- Further profits are split 80/20 between Tricon and the limited partners

- Tricon runs a long-term employee incentive program that give employees 50% of incentive fees earned

Because the investments Tricon is in are real estate developments the return on investment is lumpy and delayed. The incentive structure adds to this lag, as Tricon is the last one paid out. The company said in their Annual Information Form (the Canadian equivalent of a 10-K) that there is typically a 6-8 year lag between closing of the fund and the payout of any incentive to Tricon.

In my attempt to value the incentive fees I created the table below. I used the projected ROI and ROE provided by the company in their Q3 MD&A. I extrapolated a duration of each fund by matching the ROI to the ROE. I checked the ROI against the minimum ROI for that investment (assuming 9.5% minimum return) to make sure that each exceeded the threshold required for Tricon to begin to collect incentive fees. I calculated Tricon’s take and subtracted the percentage of the take that would go toward the long-term employee incentive program. I used a 10% discount rate to calculate the present value of the fees.

Finally, I discounted the final value obtained by a 25% haircut to account for the uncertainty in the outcome. I think this is pretty reasonable. If you look at the historical performance of Tricon funds (available in the AIF), they have done as well or better as the company estimates for the future.

Finally, I discounted the final value obtained by a 25% haircut to account for the uncertainty in the outcome. I think this is pretty reasonable. If you look at the historical performance of Tricon funds (available in the AIF), they have done as well or better as the company estimates for the future.

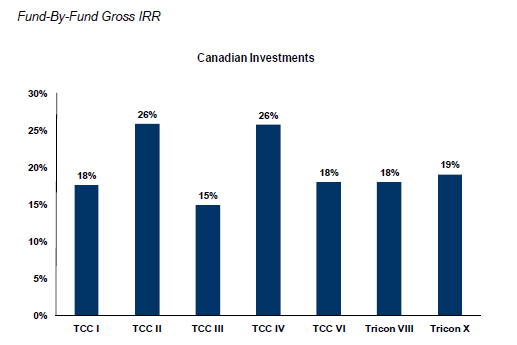

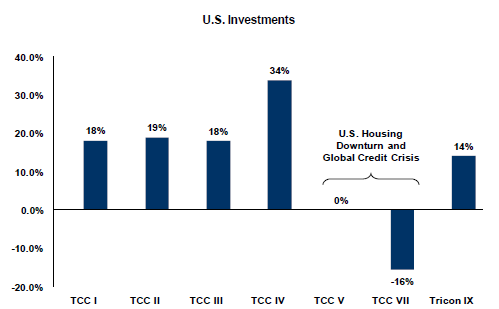

I’ve also done a bunch of work investigating the properties that Tricon is developing. One of them is right here in Calgary, and I am impressed with their choice of location and am satisfied that it will succeed even if the economy here slows. The others, in Toronto, Vancouver and Edmonton, certainly hold some risk due to the housing correction occurring, but appear to be in equally good locations and in most cases well along the development path.

Co-investment

The company has begun to invest as a limited partner in their own funds. They have committed to providing $50.4 million of capital to Tricon XI and XII, of which they have committed $13 million so far.

In addition, they have taken a $14.4 million stake in a residential housing development called Cross Creek Ranch, a planned community in Houston, Texas. The company describes Cross Creek as follows:

Cross Creek Ranch (“Cross Creek”) is an active 3,200-acre master-planned community in Houston, Texas with 4,775 residential lots which will be sold to builders as well as 238.4 acres of commercial land which will also be marketed for sale to commercial developers. Although still in the very early stages, the project appears to be meeting or exceeding the expectations of both the investor and the Company. The project was underwritten to produce a net IRR to the Company of 21.7% plus estimated future asset management fees of approximately $6.5 million.

I followed the same methodology as above to value Cross Creek. Taking the company’s estimated IRR estimate at face value, discounting the returns and management fees (assuming the project has a 4 year duration), and then applying a 25% haircut to account for the uncertainty of the outcome, and I arrive at a net present value of Cross Creek of $17.25 million.

The co-investment in Tricon XI and XII gives a value of $14.5 million.

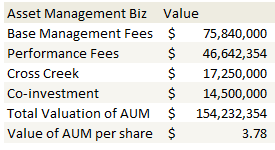

Adding it up

If I add up the sum of the parts, I get the following per share valuation of the asset under management business.

If you look at the asset under management business on a purely historic basis, the company had about 30 million shares outstanding before they began to purchases houses and the stock price fluctuated between $3.50 and $4. Therefore the market was valuing the business at about the level I am estimating here.

Therefore the market is valuing the rest of Tricon, which consists of cash, convertible debt and the residential housing business, at between $3.25 and $3.50. It is the housing business that I am most interested in. Next up will be for me to evaluate just how fair that value is.

Good Analysis and I will be interested to read the rest.

I had bought TCN back when they came public at $5.00 based on their reputation and dividend, but always found it hard to value. Their move into US housing seems to be going well and their stated rates of return are good, with the potential for higher capital returns down the road.

I did, however, sell recently in the $6.90 range. My first concern were their frequent financings in the market – I know this money was being raised to drive new businesses, but I felt that I was being overly diluted just as the value was surfacing in the company. My second issue was trying to figure out what the value of the company really was. They are trading at well over 2 times book value which is high for a traditional real estate company and they are also already at high multiples on earnings and EBITDA valuations.

The story is good (undervalued US housing), so it could be a good stock to ride the real estate rebound for the next while, but I personally have a tough time holding stocks where I do not see underlying value as they tend to correct quickly as well (in my experiences).

But, having said all that, I am interested in the rest of your analysis and could re-enter if it makes sense.

While i haven’t worked through the details of a complete valuation I suspect that when I do I won’t find it to be significantly higher than the current share price. It will probably be in the $6-$7 range. But I think that focusing on the current value is probably a mistake. Tricon is going to be more of an event driven story. Value will continue to be added as they purchase more properties. And each time there is a purchase, assuming the purchases continue to be on favorable terms, the stock price will adjust. So I’m not sure this will ever be a story where you see a big discount to intrinsic value. More likely that the stock price will continue to follow additions to NAV upward. Reminds me of Newcastle. I mean you could have hesitated on NCT all the way up, but every few months they would add another MSR deal or the retirement REIT business or the MBS portfolio and with each addition the stock price rose.

Hi – just wanted to say I’m a new reader of your blog and I’ve really enjoyed all of the postings I’ve read so far. Thanks so much for sharing your insights.

A quick question for you with regard to your second chart – could you explain to me how you’re extrapolating duration as well as how you get to your target 9.5% ROI figures? This is probably a simple question but for some reason I’m not able to figure it out. Thanks for the help.

Check out SBY, it has everything you like about Tricon’s direcrt housing ownership play, but without the AUM angle to complicate it’s analysis. It’s a pure play SFH rental REIT with a portfolio of homes bought at the bottom with I am long SBY.

Thanks, I’ve looked at SBY and have been considering buying it. I took a position in TCN because they appear cheaper to me once you ex-out the AUM business. But both SBY and RESI could be good plays. I think RESI is interesting because their method is to buy the bonds that have foreclosed properties packaged into them and then take over the properties that way. I can imagine this would be a way to take over blocks of houses more cheaply.

Thanks, I’ve looked at RESI very briefly too. I got hung up on them physically relocating their executives and offices from Europe to the US Virgin Islands at significant expense and didn’t explore further. I saw that move as a looting extravagant corporate culture red flag. The homes that they buy and their business counter-parties are located on the mainland USA. I can’t see how being in the USVI instead of on the mainland helps them conduct business. Going public should be a time to up the ante on hard work, not sit on the beach with a tiny umbrella rum drink. What’s next, a corporate jet to make hops to Florida or Charlotte to actually do some work?

Do you happen to know if they had a valid business reason for relocating HQ and execs to USVI?